United Healthcare 2001 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2001 United Healthcare annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

|

|

PAGE 45 UnitedHealth Group

NET EARNINGS PER COMMON SHARE

We compute basic net earnings per common share by dividing net earnings by the weighted-average

number of common shares outstanding during the period. We determine diluted net earnings per

common share using the weighted-average number of common shares outstanding during the period,

adjusted for the dilutive effect of common stock equivalents, consisting of shares that might be issued

upon exercise of common stock options.

DERIVATIVE FINANCIAL INSTRUMENTS

As part of our risk management strategy, we may enter into interest rate swap agreements to manage our

exposure to interest rate risk. The differential between fixed and variable rates to be paid or received is

accrued and recognized over the life of the agreements as an adjustment to interest expense in the

Consolidated Statements of Operations.

RECENTLY ISSUED ACCOUNTING STANDARDS

In June 2001, the Financial Accounting Standards Board (FASB) issued Statement of Financial Accounting

Standards (SFAS) No. 141, “Business Combinations,” and SFAS No. 142, “Goodwill and Other Intangible

Assets.” Under SFAS No. 141, business combinations initiated after June 30, 2001, must be accounted for

using the purchase method of accounting. Under SFAS No. 142, amortization of goodwill and indefinite-

lived intangible assets will cease, and the carrying value of these assets will instead be evaluated for

impairment using a fair-value-based test, applied at least annually. We adopted SFAS No. 142 on January 1,

2002, completed the initial impairment tests of goodwill as required by SFAS No. 142, and determined that

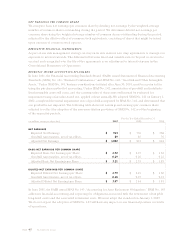

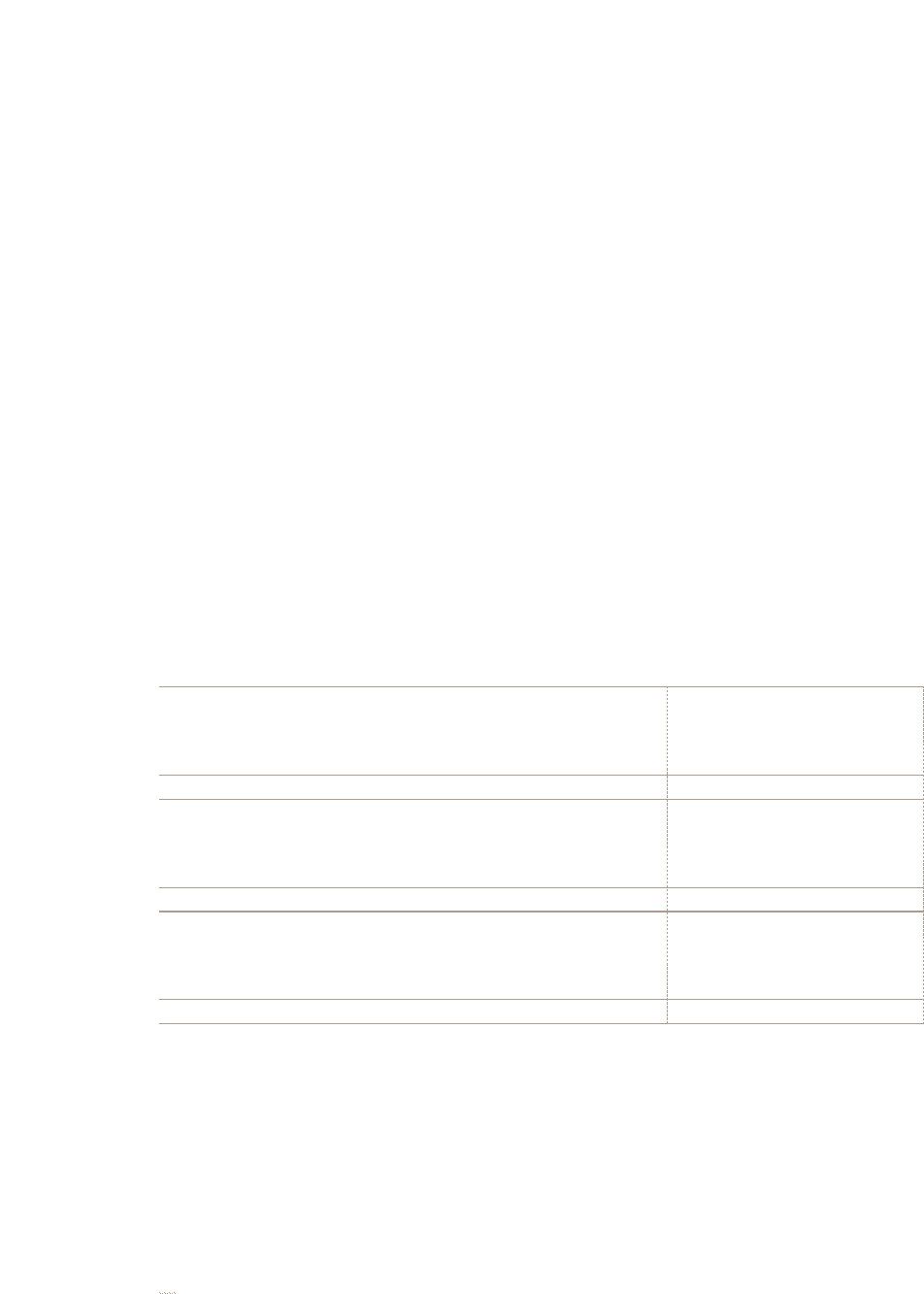

our goodwill is not impaired. The following table shows net earnings and earnings per common share

adjusted to reflect the adoption of the non-amortization provisions of SFAS No. 142 as of the beginning

of the respective periods:

For the Year Ended December 31,

(in millions, except per share data) 2 0 0 1 2000 1999

NET EARNINGS

Reported Net Earnings $ 913 $736 $568

Goodwill Amortization, net of tax effects 89 85 76

Adjusted Net Earnings $ 1,002 $821 $644

BASIC NET EARNINGS PER COMMON SHARE

Reported Basic Net Earnings per Share $ 2.92 $2.27 $1.63

Goodwill Amortization, net of tax effects 0.29 0.26 0.22

Adjusted Basic Net Earnings per Share $ 3.21 $2.53 $1.85

DILUTED NET EARNINGS PER COMMON SHARE

Reported Diluted Net Earnings per Share $ 2.79 $2.19 $1.60

Goodwill Amortization, net of tax effects 0.28 0.25 0.21

Adjusted Diluted Net Earnings per Share $ 3.07 $2.44 $1.81

In June 2001, the FASB issued SFAS No. 143, “Accounting for Asset Retirement Obligations.” SFAS No. 143

addresses financial accounting and reporting for obligations associated with the retirement of tangible

long-lived assets and the associated retirement costs. We must adopt the standard on January 1, 2003.

We do not expect the adoption of SFAS No. 143 will have any impact on our financial position or results

of operations.