TomTom 2012 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2012 TomTom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

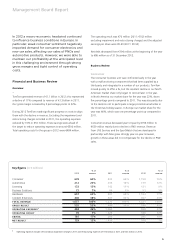

13

Group risk profi le

—

Below is an overview of the business risks that we believe are

most relevant to the achievement of our long-term goals and

strategy. This overview is not exhaustive and should be considered

in connection with forward-looking statements. There may be

risks not yet known to us or which are currently not deemed to be

material, which could later turn out to have a signifi cant impact

on our business or have a material adverse effect on TomTom’s

fi nancial condition, results of operations and liquidity.

Strategic risks

—

Changing competitive landscape

We operate in a highly dynamic and competitive industry. Failure

to adapt our organisation to industry trends or otherwise remain

competitive could have a material adverse effect on our business

and TomTom’s fi nancial condition, results of operations and

liquidity.

Many of our current competitors are large, well-known

organisations with greater fi nancial, technical and human

resources than our group. They may have greater ability to fund

product research and development and capitalise on potential

market opportunities. New competitors interested in the same

markets and products may also emerge.

We have entered into a number of strategic partnerships and joint

ventures to bring competitive product and service offerings to

market. If any of our strategic partners fail to perform as planned

or if we fail to fi nd suitable partners for our business activities,

we may be unable to bring our products and services to the

market and maintain a competitive market position.

Global economics

The majority of our sales are generated in Europe which makes us

vulnerable to the economic challenges and fi scal austerity currently

being experienced across the European Union in the wake of the

global fi nancial crisis. The US is also an important market for us

and any further deterioration in consumer demand as a result of

the global economic climate would also have a negative impact

on our fi nancial results.

The majority of our purchases are made in USD. Any devaluation

of the euro against the USD would therefore have a negative

impact on our profi tability. Although we use foreign exchange

contracts to hedge activities, these are short term in nature.

The impact of global economic conditions on consumer

demand could impair our ability to generate suffi cient cash fl ow

to support our investment plans. These or other unforeseen

macro-economic conditions may render us unable to implement

our strategic agenda as planned and consequently could have

a material adverse effect on TomTom’s fi nancial condition, results

of operations and liquidity.

Geographical sustainability

Currently the North American market offers substantial business

opportunities to us, especially as regards sales of navigation

solutions. We view maintaining and preferably growing market

share as a vital element of being successful in the US market.

However, macro-economic conditions and competitive effects

may render us unable to maintain sales volume and profi ts in

North America and retailer support for our products and services

could decline, impacting our ability to maintain market share

and average selling prices in the region.

Our aspiration to grow in high growth markets such as India,

China and Brazil will expose us to additional political, social and

economic risks. We cannot be certain that our products and

services will meet consumer acceptance in these markets and we

may be unable to realise our growth objectives in these emerging

markets. If we are unable to maintain our market share in North

America or realise our growth plans in emerging markets our

anticipated revenues and profi ts could be adversely affected.

Automotive

The automotive market is continuously evolving with respect to

navigation. Although the navigation experience for our end-users

is similar, whether the navigation system is built in the dash or

provided on a PND, the dynamics of supplying to the automotive

industry are very different from those for delivering mass-market

consumer electronics.

There are additional operational and technical challenges in

growing our automotive business and maintaining profi tability

over the longer term in such a rapidly evolving environment.

Furthermore, new map providers may choose to enter the

automotive market which could signifi cantly increase the level

of competition we face. If we are unsuccessful in maintaining

and growing a profi table automotive business, our fi nancial

condition, results of operations and liquidity may be materially

adversely affected.

Brand

All our products and services are brought to market under one

brand. This leads to brand concentration risk. Brand value can

be severely damaged even by isolated incidents affecting the

reputation of our business or our products and services.

Some of these incidents may be beyond our ability to control

and can erode consumer confi dence in our products or services.

Factors that negatively affect our reputation or brand image,

such as adverse consumer publicity, inferior product quality or

poor service, could have a material adverse effect on our fi nancial

condition and results of operations.