Public Storage 2000 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2000 Public Storage annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

19

P

UBLIC

S

TORAGE

, I

NC

. 2000 A

NNUAL

R

EPORT

During 2000 and 1999, our investment in real estate entities reflected decreases as a result of business combinations whereby the

Company eliminated approximately $14,393,000 and $66,690,000, respectively, of pre-existing investments in real estate entity

investments. Offsetting these decreases are additional investments made by the Company in other unconsolidated entities totaling

$75,146,000 and $77,656,000 in 2000 and 1999, respectively.

In April 1997, the Company and an institutional investor formed a joint venture partnership for the purpose of developing up to

$220 million of storage facilities. As of December 31, 2000, the joint venture partnership had completed construction on 47 storage

facilities with a total cost of approximately $231.5 million. The partnership is funded solely with equity capital consisting of 30% from

the Company and 70% from the institutional investor.

Note 6 —

Revolving Line of Credit

The credit agreement (the “Credit Facility”) has a borrowing limit of $150 million and an expiration date of July 1, 2002. The

expiration date may be extended by one year on each anniversary of the credit agreement. Interest on outstanding borrowings

is payable monthly. At our option, the rate of interest charged is equal to (i) the prime rate or (ii) a rate ranging from the London

Interbank Offered Rate (“LIBOR”) plus 0.40% to LIBOR plus 1.10% depending on the Company’s credit ratings and coverage ratios,

as defined. In addition, the Company is required to pay a quarterly commitment fee of 0.250% (per annum). The Credit Facility allows

us, at our option, to request the group of banks to propose the interest rate they would charge on specific borrowings not to exceed

$50 million; however, in no case may the interest rate proposal be greater than the amount provided by the Credit Facility.

Under covenants of the Credit Facility, we are required to (i) maintain a balance sheet leverage ratio of less than 0.40 to 1.00,

(ii) maintain net income of not less than $1.00 for each fiscal quarter, (iii) maintain certain cash flow and interest coverage ratios (as

defined) of not less than 1.0 to 1.0 and 5.0 to 1.0, respectively, and (iv) maintain a minimum total shareholders’ equity (as defined).

In addition, we are limited in its ability to incur additional borrowings (we are required to maintain unencumbered assets with an

aggregate book value equal to or greater than three times our unsecured recourse debt) or sell assets. We were in compliance with

the covenants of the Credit Facility at December 31, 2000.

Note 7 —

Notes Payable

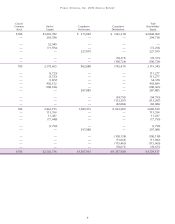

Notes payable at December 31, 2000 and 1999 consist of the following:

2000 1999

Carrying Carrying

(Amounts in thousands) amount Fair value amount Fair value

7.08% to 7.66% unsecured senior notes, due at varying

dates between November 2003 and January 2007 $129,250 $129,250 $138,000 $138,000

Mortgage notes payable:

10.55% mortgage notes secured by real estate facilities,

principal and interest payable monthly, due August 2004 23,820 25,105 26,231 27,438

7.134% to 10.5% mortgage notes secured by real estate

facilities, principal and interest payable monthly, due at

varying dates between May 2004 and September 2028 2,933 2,933 3,107 3,107

$156,003 $157,288 $167,338 $168,545

All of our notes payable are fixed rate. The senior notes require interest and principal payments to be paid semi-annually and have

various restrictive covenants, all of which have been met at December 31, 2000.

The 10.55% mortgage notes consist of five notes, which are cross-collateralized by 19 properties and are due to a life insurance

company. Although there is a negative spread between the carrying value and the estimated fair value of the notes, the notes provide

for the prepayment of principal subject to the payment of penalties, which exceed this negative spread. Accordingly, prepayment of

the notes at this time would not be economically practicable.