Freddie Mac 2009 Annual Report Download - page 9

Download and view the complete annual report

Please find page 9 of the 2009 Freddie Mac annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

|

|

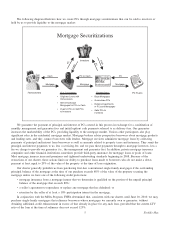

Our charter requirement for credit protection on mortgages with LTV ratios greater than 80% does not apply to

multifamily mortgages or to mortgages that have the benefit of any guarantee, insurance or other obligation by the U.S. or

any of its agencies or instrumentalities (e.g., the FHA, the VA or the USDA, Rural Development).

Under our charter, our mortgage purchase operations are confined, so far as practicable, to mortgages which we deem to

be of such quality, type and class as to meet generally the purchase standards of other private institutional mortgage

investors. This is a general marketability standard.

Government Support for our Business

We are dependent upon the continued support of Treasury and FHFA in order to continue operating our business. We

also receive substantial support from the Federal Reserve. Our ability to access funds from Treasury under the Purchase

Agreement is critical to keeping us solvent and avoiding the appointment of a receiver by FHFA under statutory mandatory

receivership provisions. This support includes the following:

• under the Purchase Agreement, Treasury made a commitment to provide funding, under certain conditions, to

eliminate deficits in our net worth. The Purchase Agreement provides that the $200 billion cap on Treasury’s funding

commitment will increase as necessary to accommodate any cumulative reduction in our net worth during 2010, 2011

and 2012. To date, we received an aggregate of $50.7 billion in funding under the Purchase Agreement. We expect to

make additional draws in future periods;

• in November 2008, the Federal Reserve established a program to purchase (i) our direct obligations and those of

Fannie Mae and the FHLBs and (ii) mortgage-related securities issued by us, Fannie Mae and Ginnie Mae. According

to information provided by the Federal Reserve, it held $64.1 billion of our direct obligations and had net purchases

of $400.9 billion of our mortgage-related securities under this program as of February 10, 2010. In September 2009,

the Federal Reserve announced that it would gradually slow the pace of purchases under the program in order to

promote a smooth transition in markets and anticipates that its purchases under this program will be completed by the

end of the first quarter of 2010;

• in September 2008, Treasury established a program to purchase mortgage-related securities issued by us and Fannie

Mae. This program expired on December 31, 2009. According to information provided by Treasury, it held

$197.6 billion of mortgage-related securities issued by us and Fannie Mae as of December 31, 2009 previously

purchased under this program; and

• in September 2008, we entered into the Lending Agreement with Treasury, pursuant to which Treasury established a

secured lending credit facility that was available to us as a liquidity back-stop. The Lending Agreement expired on

December 31, 2009. We did not make any borrowings under the Lending Agreement.

For information on the potential impact of the completion of the Federal Reserve’s mortgage-related securities and debt

purchase programs on our business, see “MD&A — LIQUIDITY AND CAPITAL RESOURCES — Liquidity.” We do not

believe we have experienced any adverse effects on our business from the expiration of the Lending Agreement (which

occurred after the December 2009 amendment to the Purchase Agreement) or the expiration of Treasury’s mortgage-related

securities purchase program.

For more information on the programs and agreements described above, see “Conservatorship and Related

Developments.”

Our Customers

Our customers are predominantly lenders in the primary mortgage market that originate mortgages for homeowners and

owners of rental apartment properties. These lenders include mortgage banking companies, commercial banks, savings banks,

community banks, insurance companies, credit unions, state and local housing finance agencies and savings and loan

associations.

We acquire a significant portion of our mortgages from several large lenders. These lenders are among the largest

mortgage loan originators in the U.S. Due to the mortgage and financial market crisis during 2008 and 2009, a number of

larger mortgage originators consolidated and, as a result, mortgage origination volume during 2009 was concentrated in a

smaller number of institutions. See “RISK FACTORS — Competitive and Market Risks” for further information. In addition,

many of our customers experienced financial and liquidity problems that may affect the volume of business they are able to

generate. During 2009, two mortgage lenders (Wells Fargo Bank, N.A. and Bank of America, N.A.) each accounted for more

than 10% of our single-family mortgage purchase volume. These two lenders collectively accounted for approximately 38%

of our single-family mortgage purchase volume for 2009 and our top ten lenders represented approximately 74% of our

single-family mortgage purchase volume for the same period. Our top three multifamily lenders (CBRE Melody & Company,

Deutsche Bank Berkshire Mortgage and Berkadia Commercial Mortgage LLC, which acquired Capmark Finance Inc. in

6Freddie Mac