Freddie Mac 2009 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2009 Freddie Mac annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

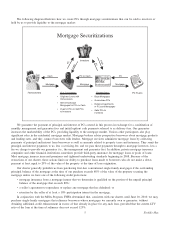

|

|

SIFMA publishes guidelines pertaining to the types of mortgages that are eligible for TBA trades. Mortgages eligible

for purchase by us due to the temporary increase to the conforming loan limits established by the Economic Stimulus Act of

2008 are not eligible for inclusion in TBA pools. However, SIFMA has permitted mortgages that are eligible for purchase by

us due to the increase to loan limits for certain high-cost areas under the Reform Act, which we refer to as “super-

conforming” mortgages, to constitute up to 10% of the original principal balance of TBA pools.

Credit Risk

Our Single-family Guarantee segment is responsible for pricing and managing credit risk related to single-family loans,

including single-family loans underlying our PCs. For more information regarding credit risk, see “MD&A — RISK

MANAGEMENT — Credit Risks” and “NOTE 7: MORTGAGE LOANS AND LOAN LOSS RESERVES” to our

consolidated financial statements.

Multifamily Segment

Through our Multifamily segment, we guarantee, securitize and invest in multifamily mortgages and CMBS. We also

securitize and guarantee the payment of principal and interest on multifamily mortgage-related securities and mortgages

underlying multifamily housing revenue bonds. The mortgage loans held in the Multifamily segment are secured by

properties with five or more residential rental units. These loans may have either adjustable or fixed interest rates, and some

may have an interest-only period that converts to amortizing at a future date. The loans are generally structured as balloon

mortgages with terms ranging from five to ten years and include provisions for the payment of yield maintenance fees to us

if the mortgage is paid prior to the end of its term. Our multifamily mortgage products, services and initiatives primarily

finance rental housing for low- and moderate-income families.

Prior to 2008, we purchased and held multifamily loans for investment purposes. In 2008, we began purchasing certain

multifamily mortgages and designating them as held-for-sale, as part of our expansion of multifamily security products. In

2009, we increased our securitization of multifamily loans through the issuance of Structured Transactions totaling

$2.4 billion in unpaid principal balance. We expect to continue purchasing multifamily loans and designating them as held-

for-sale as part of our further expansion of multifamily securitization transactions in 2010. We may also sell multifamily

loans from time to time.

The multifamily property market is affected by the relative affordability of single-family home prices, construction

cycles, and general economic factors, such as employment rates, all of which influence the supply and demand for

apartments and pricing for rentals. Our multifamily loan volume is largely sourced through established institutional channels

where we are generally providing post-construction financing to large apartment project operators with established track

records. Property location and rental cash flows provide support to capitalization values on multifamily properties, on which

investors base lending decisions.

The market for multifamily properties relies on having successful apartment developers and operators to develop,

administer and maintain the properties. Many such companies experienced significant financial difficulties in 2009 due to the

challenging market conditions. As a result, the ability of multifamily apartment developers and operators to continue to

support new property development and invest in existing properties is limited. This could result in lower capacity for industry

growth and reduced expenditures on improvements of existing properties.

Our Multifamily segment also includes certain investments in LIHTC partnerships formed for the purpose of providing

equity funding for affordable multifamily rental properties. In these investments, we provide equity contributions to

partnerships designed to sponsor the development and ongoing operations for low- and moderate-income multifamily

apartments and, we planned to realize a return on our investment through reductions in income tax expense that result from

federal income tax credits and the deductibility of operating losses generated by the partnerships. However, we are no longer

investing in these partnerships to support the low- and moderate-income rental markets, because we do not expect to be able

to use the underlying federal income tax credits or the operating losses generated from the partnerships as a reduction to our

taxable income because of our inability to generate sufficient taxable income. See “NOTE 5: VARIABLE INTEREST

ENTITIES” to our consolidated financial statements for additional information.

We also guarantee the payment of principal and interest on multifamily mortgage loans and securities that are originated

and held by state and municipal housing finance agencies to support tax-exempt and taxable multifamily housing revenue

bonds. By engaging in these activities, we provide liquidity to this sector of the mortgage market. See “MD&A — MHA

PROGRAM AND OTHER EFFORTS TO ASSIST THE U.S. HOUSING MARKET” for further information.

Our Competition

Historically, our principal competitors have been Fannie Mae, the FHLBs, Ginnie Mae and other financial institutions

that retain or securitize mortgages, such as commercial and investment banks, dealers, thrift institutions, and insurance

companies. Since 2008, most of our competitors, other than Fannie Mae, the FHLBs and Ginnie Mae, have ceased their

15 Freddie Mac