Freddie Mac 2009 Annual Report Download - page 10

Download and view the complete annual report

Please find page 10 of the 2009 Freddie Mac annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

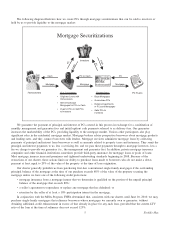

|

|

December 2009) each accounted for more than 10%, and collectively represented approximately 40% of our multifamily

purchase volume during 2009.

Our Business Segments

We manage our business, under the direction of the Conservator, through three reportable segments:

• Investments;

• Single-family Guarantee; and

• Multifamily.

For a summary and description of our financial performance and financial condition on a consolidated as well as

segment basis, see “MD&A” and “FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA” and the accompanying

notes to our consolidated financial statements.

As described below in “Conservatorship and Related Developments — Impact of Conservatorship and Related Actions

on Our Business,” we are subject to a variety of different, and potentially competing, objectives in managing our business.

These objectives create conflicts in strategic and day-to-day decision making that will likely lead to suboptimal outcomes for

one or more, or possibly all, of these objectives.

Investments Segment

Our Investments business is responsible for investment activity in single-family mortgages and mortgage-related

securities, other investments, debt financing, and managing our interest rate risk, liquidity and capital positions. We invest

principally in mortgage-related securities and single-family mortgages.

Although we are primarily a buy-and-hold investor in mortgage assets, we may sell assets to reduce risk, provide

liquidity, support the performance of our PCs or structure certain transactions that are designed to improve our returns. We

estimate our expected investment returns using an OAS approach, which is an estimate of the yield spread between a given

financial instrument and a benchmark (LIBOR, agency or Treasury) yield curve. In this approach, we consider potential

variability in the instrument’s cash flows resulting from any options embedded in the instrument, such as prepayment

options. Our Investments segment activities sometimes include the purchase of mortgages and mortgage-related securities

with less attractive investment returns and with incremental risk in order to achieve our affordable housing goals and

subgoals. Additionally, in this segment we maintain a cash and other investments portfolio, comprised primarily of cash and

cash equivalents, non-mortgage-related securities, federal funds sold and securities purchased under agreements to resell, to

help manage our liquidity needs.

The unpaid principal balance of our mortgage-related investments portfolio, including CMBS held by our Multifamily

segment, was $755.3 billion as of December 31, 2009. Under the Purchase Agreement with Treasury and FHFA regulation,

the unpaid principal balance of our mortgage-related investments portfolio could not exceed $900 billion as of December 31,

2009, and must decline by 10% per year thereafter until it reaches $250 billion. The annual 10% reduction in the size of our

mortgage-related investments portfolio, the first of which is effective on December 31, 2010, is calculated based on the

maximum allowable size of the mortgage-related investments portfolio, rather than the actual unpaid principal balance of the

mortgage-related investments portfolio, as of December 31 of the preceding year. Due to this restriction, the unpaid principal

balance of our mortgage-related investments portfolio may not exceed $810 billion as of December 31, 2010. The Purchase

Agreement also limits the amount of indebtedness we can incur. In each case, the limitations will be determined without

giving effect to any change in the accounting standards related to transfers of financial assets and consolidation of VIEs or

any similar accounting standard.

Treasury has stated it does not expect us to be an active buyer to increase the size of our mortgage-related investments

portfolio, and also does not expect that active selling will be necessary to meet the required portfolio reduction targets.

FHFA has also stated its expectation in the Acting Director’s February 2, 2010 letter that we will not be a substantial buyer

or seller of mortgages for our mortgage-related investments portfolio, except for purchases of delinquent mortgages out of

PC pools. FHFA has stated that, given the size of our current mortgage-related investments portfolio and the potential

volume of delinquent mortgages to be purchased out of PC pools, it expects that any net additions to our mortgage-related

investments portfolio would be related to that activity. On February 10, 2010, we announced that we will purchase

substantially all of the single-family mortgage loans that are 120 days or more delinquent from our PCs and Structured

Securities due to the changing economics of keeping these loans in PCs. As of December 31, 2009, the total unpaid principal

balance of such mortgages was approximately $70.2 billion.

Debt Financing

We fund our on balance sheet investment activities in our Investments and Multifamily segments by issuing short-term

and long-term debt. Competition for funding in the capital markets can vary with economic and financial market conditions

and regulatory environments. Our access to the debt markets has improved since the height of the credit crisis in the fall of

7Freddie Mac