Visa 2008 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2008 Visa annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

|

|

Table of Contents

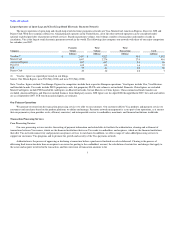

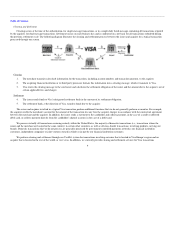

Largest Operators of Open-Loop and Closed-Loop Retail Electronic Payments Networks

The largest operators of open-loop and closed-loop retail electronic payments networks are Visa, MasterCard, American Express, Discover, JCB and

Diners Club. With the exception of Discover, which primarily operates in the United States, all of the other network operators can be considered multi-

national or global providers of payments network services. Based on payments volume, total volume, number of transactions and number of cards in

circulation, Visa is the largest retail electronic payments network in the world. The following chart compares our network with those of our major competitors

for calendar year 2007:

Company

Payments

Volume

Total

Volume

Total

Transactions Cards

(billions) (billions) (billions) (millions)

Visa Inc.(1) $ 2,457 $ 3,822 50.3 1,592

MasterCard 1,697 2,276 27.0 916

American Express 637 647 5.0 86

Discover 102 119 1.6 57

JCB 55 61 0.6 58

Diners Club 29 30 0.2 7

(1) Visa Inc. figures as reported previously in our filings.

Source: The Nilson Report, issue 902 (May 2008) and issue 903 (May 2008).

Note: Visa Inc. figures exclude Visa Europe. Figures for competitors include their respective European operations. Visa figures include Visa, Visa Electron,

and Interlink brands. Visa cards include PLUS proprietary cards, but proprietary PLUS cash volume is not included. Domestic China figures are excluded.

MasterCard figures include PIN-based debit card figures on MasterCard cards, but not Maestro or Cirrus figures. China commercial funds transfers are

excluded. American Express and Discover include business from third-party issuers. JCB figures are for April 2006 through March 2007, but cards and outlets

are as of September 2007. JCB total transaction figures are estimates.

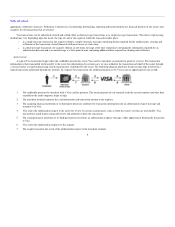

Our Primary Operations

We generate revenue from the transaction processing services we offer to our customers. Our customers deliver Visa products and payment services to

consumers and merchants based on the product platforms we define and manage. Payments network management is a core part of our operations, as it ensures

that our payments system provides a safe, efficient, consistent, and interoperable service to cardholders, merchants, and financial institutions worldwide.

Transaction Processing Services

Core Processing Services

Our core processing services involve the routing of payment information and related data to facilitate the authorization, clearing and settlement of

transactions between Visa issuers, which are the financial institutions that issue Visa cards to cardholders, and acquirers, which are the financial institutions

that offer Visa network connectivity and payments acceptance services to merchants. In addition, we offer a range of value-added processing services to

support our customers' Visa programs and to promote the growth and security of the Visa payments network.

Authorization is the process of approving or declining a transaction before a purchase is finalized or cash is disbursed. Clearing is the process of

delivering final transaction data from an acquirer to an issuer for posting to the cardholder's account, the calculation of certain fees and charges that apply to

the issuer and acquirer involved in the transaction, and the conversion of transaction amounts to the

7