Visa 2008 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2008 Visa annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

|

|

Table of Contents

scrutiny worldwide, which may have a material adverse impact on our revenues, our prospects for future growth and our overall business," and Item 8

—"Financial Statements and Supplementary Data" elsewhere in this report.

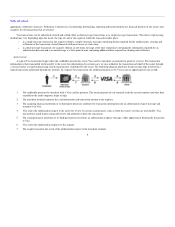

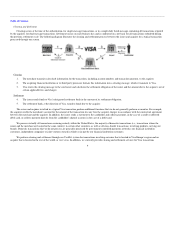

Merchant Discount Rates. Acquirers generally charge merchants a fee for each transaction, called a "merchant discount." This fee would typically cover

costs they incur for participation in four-party payments networks, including those relating to interchange, and compensate them for various other services

they provide to merchants. Merchant discount rates and other merchant fees are set by our acquirers without our involvement and by agreement with their

merchant customers and are established in competition with other acquirers, other payment card systems and other forms of payment. We do not establish or

regulate merchant discount rates or any other fees charged by our acquirers.

Intellectual Property

We rely on a combination of patent, trademark, copyright and trade secret laws in the United States and other jurisdictions, as well as confidentiality

procedures and contractual provisions, to protect our proprietary technology.

We own a number of valuable trademarks and designs, which are essential to our business, including Visa, Interlink, PLUS, Visa Electron, the "Winged

V" design, the "Dove" design and the "Bands Design—Blue, White & Gold." We also own numerous other valuable trademarks and designs covering various

brands, products, programs and services. Through agreements with our customers, we authorize and monitor the use of our trademarks in connection with

their participation in our payments network.

In addition, we own a number of patents and patent applications relating to payments solutions, transaction processing, security systems and other

matters.

Competition

We compete in the global payment marketplace against all forms of payment, including paper-based forms (principally cash and checks), card-based

payments (including credit, charge, debit, ATM, prepaid, private-label and other types of general purpose and limited use cards) and other electronic

payments (including wire transfers, electronic benefits transfers, automatic clearing house, or ACH, payments and electronic data interchange).

Within the general purpose payment card industry, we face substantial and intense competition worldwide. The leading global card brands in the

general purpose payment card industry are Visa, MasterCard, American Express and Diners Club. Other general purpose card brands are more concentrated in

specific geographic regions, such as JCB in AP and Discover in the United States. In certain countries, our competitors have leading positions, such as JCB in

Japan and China UnionPay in China, which is the sole domestic payment processor and operates the sole domestic acceptance mark in China due to local

regulation. We also compete against private-label cards, which can generally be used to make purchases solely at the sponsoring retail store, gasoline retailer

or other merchant.

In the debit card market segment, Visa and MasterCard are the primary global brands. In addition, our Interlink and Visa Electron brands compete with

Maestro, owned by MasterCard, and various regional and country-specific debit network brands, such as STAR, owned by First Data Corporation, PULSE,

owned by Discover, NYCE, owned by Metavante Corporation, and others in the United States, Interac in Canada, and EFTPOS in Australia. In addition to our

PLUS brand, the primary cash access card brands are Cirrus, owned by MasterCard, and many of the online debit network brands referenced

17