Unilever 2003 Annual Report Download - page 10

Download and view the complete annual report

Please find page 10 of the 2003 Unilever annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

|

|

Unilever Annual Report & Accounts and Form 20-F 2003 07

Chairmen’s statement

2003 in context

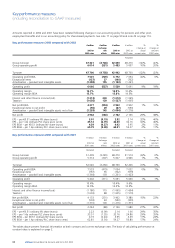

In a difficult year, we are pleased to have achieved 11% growth

in earnings per share (BEIA). We have now met or exceeded our

target of low double-digit earnings per share growth in every year

of the Path to Growth programme and this year’s performance

places our three-year Total Shareholder Return (TSR) in the top

third of our peer group. We fully intend to continue this

performance as we enter the final year of Path to Growth.

Leading brands grew by 2.5%, and operating margin (BEIA) rose

to a record 15.7%, a gain of 1.2% over 2002. Naturally, we are

disappointed with revenue growth, but the shortfall against our

top-line growth target is mainly due to specific issues in a small

number of businesses and a slow start to the year in North

America caused by sharp de-stocking in the retail trade. In Europe

consumer confidence dropped to levels not seen in recent years.

Nevertheless, we have continued to increase investment in our

brands and have maintained our market position. Once again,

we have been extraordinarily well served by skilled and dedicated

people in all parts of the business and we extend our thanks to

them on behalf of all shareholders.

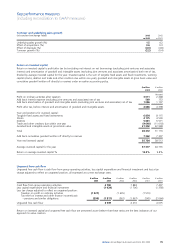

A review of Path to Growth

Path to Growth was designed to simplify the business and release

resources to be put behind fewer, bigger brands. It is all too easy

to lose sight of what we have achieved. By the close of 2004,

with one exception, we intend to have met or substantially

exceeded the very challenging milestones we set the business.

The rationalisation of our manufacturing capacity and our supply

chain is nearing completion. We have charged €5.4 billion of

restructuring costs, which is in line with our €6.2 billion target.

With one year still to go we have comfortably exceeded our

promised Path to Growth savings of €3.9 billion and our

operating margin (BEIA) has already risen from 11.1% to 15.7%.

Capital efficiency has improved by almost 9%, 3% more than

target. Ungeared free cash flow has totalled €16.4 billion since

the start of Path to Growth and net debt reduction is ahead of

plan having reduced from €26.5 billion at the end of 2000 to

€12.6 billion at the end of 2003 at current rates of exchange.

In addition, we have seamlessly integrated €30 billion of

acquisitions, managed over €7 billion of disposals and

implemented a divisional structure to harness our global scale

yet retain a spirit of local enterprise.

We are on track to reduce the brand portfolio from 1 600 to 400

leading brands. They now account for 93% of sales as against

only 75% in 1999. We have significantly increased investment

behind these brands and we now have twelve brands with sales

of over €1 billion compared with four at the start of the strategy.

The exception of course is top-line growth where, after excellent

performances in 2001 and 2002, we have this year fallen short

against our aspirations in testing market conditions. Nevertheless,

leading brands have grown at an average of over 4% per year

during Path to Growth to date.

Overall the business today is lean, sharply focused, high margin,

strongly cash generating and delivering significant incremental

value each year.

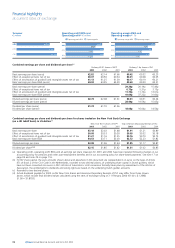

Foods division

In Foods, leading brand growth was 1.2%. Operating margin

(BEIA) improved by 1.8% to 16.0%. We made significant

progress on reducing the tail and on migrating and rationalising

the brands.

Lipton had an outstanding year, boosted by new launches

and a good summer in Europe which also benefited ice cream.

At the same time the hot summer also reduced market growth

in savoury, but Knorr held position. Bertolli and Hellmann’s

continue to make good progress.

Slim•Fast declined by 21% and the focus is now on restoring the

brand to growth. In frozen foods we continue to make gains in

profitability, but have yet to see a consistent pattern of growth.

Becel/Flora grew strongly once again, but the family spreads had

a tough year in a market affected by price competition and low

butter prices.

Our mission is to add vitality to life. We meet everyday needs for nutrition, hygiene, and

personal care with brands that help people feel good, look good and get more out of life.