US Bank 2006 Annual Report Download - page 10

Download and view the complete annual report

Please find page 10 of the 2006 US Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

8U.S. BANCORP

wholesale banking

continued demand for corporate and

commercial loans in 2006, stabilized

net interest margin and exceptional

leveraging of cross-sell opportunities

position us well.

KEY BUSINESS UNITS

Middle Market Commercial Banking

Commercial Real Estate

National Corporate Banking

Correspondent Banking

Dealer Commercial Services

Community Banking

Equipment Finance

Foreign Exchange

Government Banking

International Banking

Treasury Management

Small Business Equipment Finance

Small Business Administration

(SBA) Division

Title Industry Banking

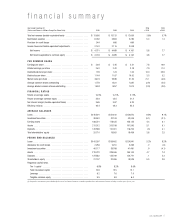

We believe that key indicators in the commercial sector are positive; however,

challenges of competitive credit and deposit pricing continued. The credit profile

of our company remains excellent as we maintain our disciplined underwriting

standards and focus on quality loans. Loans in the Wholesale Banking business

line grew five percent in 2006. Although we may experience some increase in

charge-offs in coming quarters, they should remain manageable. If interest rates

hold steady,we would expect to see continued loan growth and profitability.

During the year,we took a number of actions to further strengthen our commercial

and corporate banking industry position. We added new expertise at the senior

levels in Corporate Banking and Commercial Real Estate and in our food and

agribusiness specialized lending division. We opened new Commercial Real Estate

offices in Atlanta, Boston, Houston and Philadelphia, bringing our number of

CRE offices to 31 across the country, and opened a new foreign exchange office in

Los Angeles, joining those already in Milwaukee, Minneapolis, Portland, St. Louis

and Seattle. We launched a number of new products and expanded several existing

services to provide customer efficiency,fraud protection, treasury management,

and market entry into electronic records management.