US Bank 2006 Annual Report Download

Download and view the complete annual report

Please find the complete 2006 US Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

strategic acquisitions

2006 annual report and form 10-k

enhanced customer data protection

top banking team

agency ratings

expanded distribution

european payments expansion

positive results

return to shareholders

credit quality

financial performance

investments in our business

new products

Table of contents

-

Page 1

2006 annual report and form 10-k positive results enhanced customer data protection strategic acquisitions return to shareholders financial performance top banking team agency ratings credit quality expanded distribution investments in our business european payments expansion new products -

Page 2

...products and services is provided through four major lines of business: Wholesale Banking, Payment Services, Wealth Management and Consumer Banking. Detailed information about these businesses can be found throughout this report. U.S. Bancorp is headquartered in Minneapolis, MN. U.S. Bancorp employs... -

Page 3

... business and economic conditions, changes in interest rates, legal and regulatory developments, increased competition from both banks and non-banks, changes in customer behavior and preferences, effects of mergers and acquisitions and related integration, and effects of critical accounting policies... -

Page 4

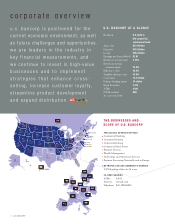

... USB At year-end 2006 ANA A THE BUSINESSES AND S C O P E O F U. S. B A N C O R P SPECIALIZED SERVICES/OFFICES Commercial Banking Consumer Banking Corporate Banking Commercial Real Estate Payment Services Wealth Management Technology and Operations Services Payment Processing Nationally and in... -

Page 5

...MIX BY BUSINESS LINE WHOLESALE BANKING U.S. Bancorp provides expertise, resources, prompt decision-making and commitment to partnerships that make us a leader in Corporate, Commercial and Commercial Real Estate Banking. From real-time cash ï¬,ow management to working capital ï¬nancing to equipment... -

Page 6

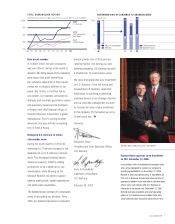

... , 8 (In Dollars) DIVIDENDS DECLARED PER COMMON SHARE 1.40 (In Dollars) 3, 33 ,16 . 3,168 1. 1.65 .780 2,500 1.50 .70 0 02 0 0 05 0 0 03 0 05 0 0 0 04 0 RETURN ON AVERAGE ASSETS 2.4 (In Percents) RETURN ON AVERAGE COMMON EQUITY 24 (In Percents) D I V I D E N D PAY O U T R AT I O 60... -

Page 7

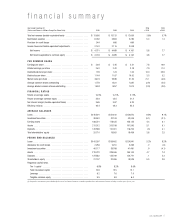

...ï¬ciency ratio (a) ...AVERAGE BALANCES Loans ...Investment securities ...Earning assets ...Assets ...Deposits ...Total shareholders' equity ...PERIOD END BALANCES Loans ...Allowance for credit losses ...Investment securities ...Assets ...Deposits ...Shareholders' equity ...Regulatory capital ratios... -

Page 8

... yield curve. To that end, we acquired additional card portfolios and expanded our merchant acquiring and processing business in Western Europe and Canada. Preparing U.S. Bancorp for future growth The long-term goals of our company have not changed. Tactics may change as circumstances do, but... -

Page 9

... companies. U.S. Bancorp has paid a dividend for 144 consecutive years. We value and appreciate your investment in U.S. Bancorp. From the hiring and development of talented, dedicated employees to providing outstanding customer service to our strategic direction and our everyday management, we work... -

Page 10

... Corporate Banking Correspondent Banking Dealer Commercial Services Community Banking Equipment Finance Foreign Exchange Government Banking International Banking Treasury Management Small Business Equipment Finance Small Business Administration (SBA) Division Title Industry Banking 8 U.S. BANCORP -

Page 11

... cash letters. FULL FINANCIAL PA RT N E R S H I P S Extending credit is a critical component of Wholesale Banking, but not the only one. Our ï¬nancial partnership with our business customers extends beyond lending to deposit and payment solutions, employee services, asset management, and trust... -

Page 12

... 10 percent of all ATMs in the United States. KEY BUSINESS UNITS Corporate Payment Systems Merchant Payment Services NOVA Information Systems, Inc. Retail Payment Solutions: Debit, Credit, Specialty Cards and Gift Cards Transactions Services: ATM and Debit Processing and Services 10 U.S. BANCORP -

Page 13

... credit card merchant acquiring and processing in Europe. November 2006 PAY M E N T S E R V I C E S D R I V E S SUCCESS AND REVENUE U.S. Bank is now the world's leading provider of freight audit and payments ® through PowerTrack, our patented, electronic business-to-business payment network... -

Page 14

... of the full spectrum of corporate trust products and services required by corporations and municipalities for raising capital. We are also experts in trust, custody, retirement and health savings account solutions for corporations, businesses, public and non-profit entities. Through FAF Advisors... -

Page 15

.... March 2006 U.S. Bancorp Asset Management changes its name to FAF Advisors to more closely align company with its First American Funds family of mutual funds and facilitate continued expansion. September 2006 U.S. Bank acquires the municipal and corporate bond trustee business from SunTrust Banks... -

Page 16

... bank lenders in loan dollar volume. KEY BUSINESS UNITS Community Banking Metropolitan Branch Banking In-store and Corporate On-site Banking Small Business Banking Consumer Lending 24-Hour Banking & Financial Sales Home Mortgage Community Development Workplace and Student Banking 14 U.S. BANCORP -

Page 17

...500th in-store branch. November 2006 U.S. Bancorp to double branch presence in Montana with agreement to acquire United Financial Corp., parent of Heritage Bank. FORTIFYING POSITIONS OF STRENGTH U.S. Bank inaugurated its "power bank" sales and customer service initiative in the St. Louis market in... -

Page 18

..., a trade association of 100 of the largest financial services companies in the country. During this annual event, companies and employees volunteer to build, paint, repair and renovate homes in their communities. In 2006, U.S. Bank and our employees participated in 55 Community Build Day projects... -

Page 19

...of the highlights of the year 2006 in our lines of business and seen our goals and ...management's discussion and analysis reports of management and independent accountants...annual report on form 10-k CEO and CFO certiï¬cations executive ofï¬cers directors corporate information U.S. BANCORP... -

Page 20

...expansion in trust and payment processing businesses, higher trading income, and gains in 2006 from the initial public offering and subsequent sale of the equity interest in a card association and the sale of a 401(k) deï¬ned contribution recordkeeping business. These favorable changes in fee-based... -

Page 21

...Earning assets Assets Noninterest-bearing deposits Deposits Short-term borrowings Long-term debt Shareholders' equity PERIOD END BALANCES Loans Allowance for credit losses Investment securities Assets Deposits Long-term debt Shareholders' equity Regulatory capital ratios Tier 1 capital... -

Page 22

...asset/ liability decisions. An increase in the margin beneï¬t of net free funds and loan fees partially offset these factors. Beginning in the third quarter of 2006, the Federal Reserve Bank paused from its policies of increasing interest rates and tightening the money supply that began in mid-2004... -

Page 23

...trust deposits related to recent acquisitions. The change in demand balances reï¬,ected a migration of customer accounts to interest-bearing products given the rising interest rate environment. The decline in business customer balances also reï¬,ected customer utilization of excess liquidity to fund... -

Page 24

... market savings account balances declined from 2004 to 2005 by $3.5 billion (10.8 percent), with declines in both the branches and other business lines. The decline was primarily the result of deposit pricing by the Company for money market products in relation to other ï¬xed-rate deposit products... -

Page 25

...) 2006 2005 2004 2006 v 2005 2005 v 2004 Credit and debit card revenue Corporate payment products revenue ATM processing services Merchant processing services Trust and investment management fees Deposit service charges Treasury management fees Commercial products revenue Mortgage banking... -

Page 26

... organic growth in most fee income categories, particularly payment processing revenues and deposit service charges. The growth in credit and debit card revenue was principally driven by higher customer transaction volumes and rate changes. The corporate payment products revenue growth reï¬,ected... -

Page 27

... related to brand awareness and credit card and prepaid gift card programs. Technology and communications expense was higher, reflecting depreciation of technology investments, network costs associated with the expansion of the payment processing businesses, and higher outside data processing... -

Page 28

...S TAT E Commercial mortgages Construction and development Total commercial real estate RESIDENTIAL MORTGAGES Residential mortgages Home equity loans, ï¬rst liens Total residential mortgages R E TA I L Credit card Retail leasing Home equity and second mortgages Other retail Revolving credit... -

Page 29

... Financial services Commercial services and supplies Capital goods Property management and development Agriculture Healthcare Paper and forestry products, mining and basic materials Consumer staples Transportation Private investors Energy Information technology Other Total Loans... -

Page 30

... of tax-exempt industrial development loans were secured by real estate. The Company's commercial real estate mortgages and construction loans had unfunded commitments of $8.9 billion at December 31, 2006, compared with $9.8 billion at December 31, 2005. The Company also ï¬nances the operations of... -

Page 31

...with asset/liability management decisions to reduce its risk to rising interest rates. Average residential mortgage loan balances increased as a result of the timing of these asset/liability decisions. Retail Total retail loans outstanding, which include credit card, retail leasing, home equity and... -

Page 32

... loans. Credit card growth was driven by balance transfers, balance growth within co-branded card contracts and afï¬nity programs. Of the total retail loans and residential mortgages outstanding, approximately 81.0 percent were to customers located in the Company's primary banking regions... -

Page 33

...used as collateral for public deposits and wholesale funding sources. While it is the Company's intent to hold its investment securities indefinitely, the Company may take actions in response to structural changes in the balance sheet and related interest rate risk and to meet liquidity requirements... -

Page 34

... given alternative funding sources. Borrowings The Company utilizes both short-term and long-term borrowings to fund earning asset growth in excess of deposit growth. Short-term borrowings, which include federal funds purchased, commercial paper, securities sold under agreements to repurchase... -

Page 35

...in the portfolio. Commercial banking operations rely on prudent credit policies and procedures and individual lender and business line manager accountability. Lenders are assigned lending authority based on their level of experience and customer service requirements. Credit ofï¬cers reporting to an... -

Page 36

... asset-based lending, commercial lease ï¬nancing, agricultural credit, warehouse mortgage lending, commercial real estate, health care and correspondent banking. The Company also offers an array of retail lending products including credit cards, retail leases, home equity, revolving credit, lending... -

Page 37

...of the credit card balances relate to bank branch, co-branded and affinity programs that generally experience better credit quality performance than portfolios generated through national direct mail programs. At December 31, 2006, approximately 80.8 percent of the student loan portfolio is federally... -

Page 38

... LOAN RATIOS AS A PERCENT OF ENDING LOANS BALANCES At December 31, 90 days or more past due excluding nonperforming loans 2006 2005 2004 2003 2002 COMMERCIAL Commercial Lease ï¬nancing Total commercial C O M M E R C I A L R E A L E S TAT E Commercial mortgages Construction and development... -

Page 39

... payment requirements. Under this program, retail customers that met certain criteria had the terms of their credit card and other loan agreements modiï¬ed to allow amortization of their balances over a period of up to 60 months. Residential mortgage loans on nonaccrual status decreased during 2006... -

Page 40

... several payment cycles. Loans that have interest rates reduced below comparable market rates remain classiï¬ed as restructured loans; however, 38 U.S. BANCORP December 31 (Dollars in Millions) Amount 2006 Commercial Commercial real estate ********* Residential mortgages ********** Credit card... -

Page 41

... lending markets in residential mortgages, home equity and installment loan ï¬nancing. USBCF manages loans originated through a broker network, correspondent relationships and U.S. Bank branch ofï¬ces. Generally, loans managed by the Company's consumer ï¬nance division exhibit higher credit... -

Page 42

...Consumer ï¬nance category included credit originated and managed by USBCF, as well as home equity and second mortgages with a loan-to-value greater than 100 percent that were originated in the branches. Within the consumer ï¬nance division, the Company originates loans to customers that may be de... -

Page 43

... Commercial mortgages Construction and development Total commercial real estate Residential mortgages Retail Credit card Retail leasing Home equity and second mortgages Other retail Total retail Total net charge-offs Provision for credit losses Acquisitions and other changes Balance... -

Page 44

... in Millions) 2006 2005 2004 2003 2002 Allowance as a Percent of Ending Loan Balances 2006 2005 2004 2003 2002 COMMERCIAL Commercial Lease ï¬nancing Total commercial C O M M E R C I A L R E A L E S TAT E Commercial mortgages Construction and development ******* Total commercial real estate... -

Page 45

... management tool, the entire allowance for credit losses is available for the entire loan portfolio. The actual amount of losses incurred can vary signiï¬cantly from the estimated amounts. Residual Value Risk Management The Company manages its risk to changes in the residual value of leased assets... -

Page 46

... manage operational risks. Each business unit of the Company is required to develop, maintain and test these plans at least annually to ensure that recovery activities, if needed, can support mission critical functions including technology, networks and data centers supporting customer applications... -

Page 47

... value of equity of the Company was liability sensitive to changes in interest rates. Use of Derivatives to Manage Interest Rate and Other Risks In the ordinary course of business, the Company enters into derivative transactions to manage its interest rate, prepayment, credit and foreign currency... -

Page 48

... payments are calculated. Interest rate caps protect against rising interest rates while interest rate ï¬,oors protect against declining interest rates. In connection with its mortgage banking operations, the Company enters into forward commitments to sell mortgage loans related to ï¬xed-rate... -

Page 49

... 2006. The Company enters into derivatives to protect its net investment in certain foreign operations. The Company uses forward commitments to sell speciï¬ed amounts of certain foreign currencies to hedge its capital volatility risk associated with ï¬,uctuations in foreign currency exchange rates... -

Page 50

... Federal Home Loan Banks that provide a source of funding through FHLB advances. The Company maintains a Grand Cayman branch for issuing eurodollar time deposits. The Company also issues commercial paper through its Canadian branch. In addition, the Company establishes relationships with dealers... -

Page 51

... rating agencies' recognition of the Company's sector-leading core earnings performance and lower credit risk proï¬le. The parent company's routine funding requirements consist primarily of operating expenses, dividends paid to shareholders, debt service, repurchases of common stock and funds used... -

Page 52

... capital requirements for well-capitalized bank holding companies. To achieve these capital goals, the Company employs a variety of capital management tools including dividends, common share repurchases, and the issuance of subordinated debt and other capital instruments. Total shareholders' equity... -

Page 53

...of the Program Maximum Number of Shares that May Yet Be Purchased Under the Program regulatory ratios, at both the bank and bank holding company level, continue to be in excess of stated ''wellcapitalized'' requirements. Table 21 provides a summary of capital ratios as of December 31, 2006 and 2005... -

Page 54

... growth in credit and debit card revenue was primarily driven by 52 U.S. BANCORP higher customer transaction volumes. The corporate payment products revenue growth reï¬,ected organic growth in sales volumes and card usage and acquired business expansion. Merchant processing services revenue was... -

Page 55

...reporting systems by speciï¬cally attributing managed balance sheet assets, deposits and other liabilities and their related income or expense. Goodwill and other intangible assets are assigned to the lines of business based on the mix of business of the acquired entity. Within the Company, capital... -

Page 56

...Banking offers lending, equipment ï¬nance and small-ticket leasing, depository, treasury management, capital markets, foreign exchange, international trade services and other ï¬nancial services to middle market, large corporate, commercial real estate, and public sector clients. Wholesale Banking... -

Page 57

... and commercial loans. Residential mortgages, including traditional residential mortgages and ï¬rst-lien home equity loans, grew Wealth Management 2006 2005 Percent Change 2006 Payment Services 2005 Percent Change 2006 Treasury and Corporate Support 2005 Percent Change 2006 Consolidated Company... -

Page 58

... trust businesses. Payment Services includes consumer and business credit cards, stored-value cards, debit cards, corporate and purchasing card services, consumer lines of credit, ATM processing and merchant processing. Payment Services contributed $967 million of the Company's net income in 2006... -

Page 59

...26 percent in 2006, compared with 3.38 percent in 2005. Treasury and Corporate Support includes the Company's investment portfolios, funding, capital management and asset securitization activities, interest rate risk management, the net effect of transfer pricing related to average balances and the... -

Page 60

... the credit portfolio, changes in the allowance for credit losses may not directly coincide with changes in the risk ratings of the credit portfolio reï¬,ected in the risk rating process. This is in part due to the timing of the risk rating process in relation to changes in the business cycle, the... -

Page 61

... for further information. Mortgage Servicing Rights MSRs are capitalized as separate assets when loans are sold and servicing is retained or may be purchased from others. MSRs are initially recorded at fair value, if practicable, and at each subsequent reporting date. The Company determines the... -

Page 62

...no change made in the Company's internal controls over ï¬nancial reporting (as deï¬ned in Rules 13a-15(f) and 15d-15(f) under the Exchange Act) that has materially affected, or is reasonably likely to materially affect, the Company's internal control over ï¬nancial reporting. The annual report of... -

Page 63

...the ï¬nancial statements and other information presented throughout the Annual Report on Form 10-K rests with the management of U.S. Bancorp. The Company believes that the consolidated ï¬nancial statements have been prepared in conformity with accounting principles generally accepted in the United... -

Page 64

... balance sheets of U.S. Bancorp as of December 31, 2006 and 2005, and the related consolidated statements of income, shareholders' equity, and cash ï¬,ows for each of the three years in the period ended December 31, 2006. These ï¬nancial statements are the responsibility of the Company's management... -

Page 65

..., and the related consolidated statements of income, shareholders' equity, and cash ï¬,ows for each of the three years in the period ended December 31, 2006 and our report dated February 23, 2007 expressed an unqualiï¬ed opinion thereon. Minneapolis, Minnesota February 23, 2007 U.S. BANCORP 63 -

Page 66

... Bancorp Consolidated Balance Sheet At December 31 (Dollars in Millions) 2006 2005 ASSETS Cash and due from banks Investment securities Held-to-maturity (fair value $92 and $113, respectively Available-for-sale Loans held for sale Loans Commercial Commercial real estate Residential mortgages... -

Page 67

... INCOME Credit and debit card revenue Corporate payment products revenue ATM processing services Merchant processing services Trust and investment management fees Deposit service charges Treasury management fees Commercial products revenue Mortgage banking revenue Investment products fees... -

Page 68

... on securities available for sale Unrealized gain on derivatives Foreign currency translation Realized loss on derivatives Reclassiï¬cation for realized losses ********* Change in retirement obligation Income taxes Total comprehensive income ******* Cash dividends declared: Preferred Common... -

Page 69

... income Adjustments to reconcile net income to net cash provided by operating activities Provision for credit losses Depreciation and amortization of premises and equipment Amortization of intangibles Provision for deferred income taxes Gain on sales of securities and other assets, net Loans... -

Page 70

... Trust and Custody and Fund Services. Payment Services includes consumer and business credit cards, stored-value cards, debit cards, corporate and purchasing card services, consumer lines of credit, ATM processing and merchant processing. Treasury and Corporate Support includes the Company... -

Page 71

... with mortgage banking activities are considered derivatives and recorded on the balance sheet at fair value with changes in fair value recorded in income. All other unfunded loan commitments are generally related to providing credit facilities to customers of the bank and are not actively traded... -

Page 72

... to manage its interest rate, foreign currency and prepayment risk and to accommodate the business requirements of its customers. All derivative instruments are recorded as other assets, other liabilities or short-term borrowings at fair value. Subsequent changes in a derivative's fair value are... -

Page 73

... credit and debit card revenue. Payments to partners and expenses related to rewards programs are recorded when earned by the partner or customer. Merchant Processing Services Merchant processing services the acquired businesses (''goodwill'') is not amortized. Other intangible assets are amortized... -

Page 74

... projected cash ï¬,ows as of the measurement date for future beneï¬t payments. Periodic pension expense (or income) includes service costs, interest costs based on the assumed discount rate, the expected return on plan assets based on an actuarially derived market-related value and amortization of... -

Page 75

... ON CASH AND DUE FROM BANKS Bank subsidiaries are required to maintain minimum average reserve balances with the Federal Reserve Bank. The amount of those reserve balances was approximately $359 million at December 31, 2006. Note 4 INVESTMENT SECURITIES The amortized cost, gross unrealized holding... -

Page 76

... or any earlier call date. As of the reporting date, the Company expects to receive all contractual principal and interest related to these securities. Because the Company has the ability and intent to hold its investment securities until their anticipated recovery in value or maturity, they are... -

Page 77

...2006 2005 COMMERCIAL Commercial Lease ï¬nancing Total commercial COMMERCIAL REAL ESTATE Commercial mortgages Construction and development Total commercial real estate RESIDENTIAL MORTGAGES Residential mortgages Home equity loans, ï¬rst liens Total residential mortgages RETAIL Credit card... -

Page 78

... of the Company's nonperforming assets as of December 31, 2006 and 2005, see Table 14 included in Management's Discussion and Analysis which is incorporated by reference into these Notes to Consolidated Financial Statements. The following table lists information related to nonperforming loans as of... -

Page 79

... in mortgage banking revenue. The Company has equity interests in two joint ventures that are accounted for utilizing the equity method. The principal activity of one entity is to provide commercial real estate ï¬nancing that the joint venture securitizes and sells to third party investors. The... -

Page 80

The conduit had commercial paper liabilities of $2.2 billion at December 31, 2006, and $3.8 billion at December 31, 2005. The Company beneï¬ts by transferring the investment securities into a conduit that provides diversiï¬cation of funding sources in a capital-efï¬cient manner and the generation... -

Page 81

... 31, 2006. Servicing and other related fees included in mortgage banking revenue were $319 million in 2006. Changes in fair value of capitalized MSRs are summarized as follows: Year Ended December 31 (Dollars in Millions) 2006 2005 2004 Balance at beginning of period 1,123 Rights purchased 52... -

Page 82

... Note 10 INTANGIBLE ASSETS Intangible assets consisted of the following: December 31 (Dollars in Millions) Estimated Life (a) Amortization Method (b) Balance 2006 2005 Goodwill Merchant processing contracts Core deposit beneï¬ts Mortgage servicing rights (c Trust relationships Other identi... -

Page 83

... Banking Consumer Banking Wealth Management Payment Services Consolidated Company Balance at December 31, 2004 Goodwill acquired Other (a Balance at December 31, 2005 Goodwill acquired Other (a Balance at December 31, 2006 (a) Other changes in goodwill include the effect of foreign exchange... -

Page 84

... following: (Dollars in Millions) Rate Type Rate (a) Maturity Date 2006 2005 U . S . B A N C O R P (Parent Company) Subordinated notes Convertible senior debentures Medium-term notes Junior subordinated debentures Capitalized lease obligations, mortgage indebtedness and other (b Subtotal... -

Page 85

... liquidity and support its capital requirements. During 2006, subordinated notes of $49 million matured and were repaid by the subsidiary. The Company has an arrangement with the Federal Home Loan Bank whereby based on collateral available (residential and commercial mortgages), the Company could... -

Page 86

... and payments on liquidation or redemption of the Trust Preferred Securities, but only to the extent of funds held by the Trusts. The Company used the proceeds from the sales of the Debentures for general corporate purposes. In connection with the formation of USB Capital IX, the trust issued... -

Page 87

... the Company. Under the plan, each share of common stock carries a right to purchase one one-thousandth of a share of preferred stock. The rights become exercisable in certain limited circumstances involving a potential business combination transaction or an acquisition of shares of the Company and... -

Page 88

... of the Company's regulatory capital: December 31 (Dollars in Millions) 2006 2005 TIER 1 CAPITAL Common shareholders' equity Qualifying preferred stock Qualifying trust preferred securities Minority interests Less intangible assets Goodwill Other disallowed intangible assets ********** Other... -

Page 89

... During 2006, the Company's primary banking subsidiary formed USB Realty Corp, a real estate investment trust, for the purpose of issuing 5,000 shares of Fixed-to-Floating Rate Exchangeable Noncumulative Perpetual Series A Preferred Stock with a liquidation preference of $100,000 per share (''Series... -

Page 90

...-term rate of return (''LTROR''). Annually the Company's Compensation Committee (''the Committee''), assisted by outside consultants, evaluates plan objectives, funding policies and plan investment policies considering its longterm investment time horizon and asset allocation strategies. The process... -

Page 91

... rates of return and asset allocation and LTROR information for a peer group in establishing its assumptions. Postretirement Medical Plan In addition to providing pension beneï¬ts, the Company provides health care and death beneï¬ts to certain retired employees through a retiree medical program... -

Page 92

... return on plan assets Employer contributions Plan participants' contributions Settlements Beneï¬t payments Fair value at end of measurement period F U N D E D S TAT U S Funded status at end of measurement period Unrecognized transition (asset) obligation Unrecognized prior service (credit... -

Page 93

... 21 $ (1) (13) $ (1) (16) $ (1) (19) (a) For 2006, the discount rate was developed using Towers Perrin's cash ï¬,ow matching bond model with a modiï¬ed duration of 12.6 years. For 2005, the discount rate approximated the Moody's Aa corporate bond rating for projected beneï¬t distributions with... -

Page 94

... terms of the various merger agreements. The historical stock award information presented below has been restated to reï¬,ect the options originally granted under acquired companies' plans. At December 31, 2006, there were 14 million shares (subject to adjustment for forfeitures) available for... -

Page 95

...determined value used to measure compensation expense may vary from their actual fair value. The following table includes the weighted average estimated fair value and assumptions utilized by the Company for newly issued grants: 2006 2005 2004 Estimated fair value Risk-free interest rate Dividend... -

Page 96

... effects of fair value adjustments on securities available-for-sale, derivative instruments in cash ï¬,ow hedges and certain tax beneï¬ts related to stock options are recorded directly to shareholders' equity as part of other comprehensive income. At December 31, 2006 and 2005, the Company held an... -

Page 97

... net operating loss carryforwards Federal AMT credits and capital losses Other deferred tax assets, net Gross deferred tax assets D E F E R R E D TA X L I A B I L I T I E S Leasing activities Mortgage servicing rights Pension and postretirement beneï¬ts Deferred fees Loans Intangible asset... -

Page 98

... year-end. The fair value of ï¬xed-rate certiï¬cates of deposit was estimated by discounting the contractual cash ï¬,ow using the discount rates implied by high-grade corporate bond yield curves. Short-Term Borrowings Federal funds purchased, securities CUSTOMER-RELATED POSITIONS The Company acts... -

Page 99

... subordinated debt was determined by using discounted cash ï¬,ow analysis based on high-grade corporate bond yield curves. Floating rate debt is assumed to be equal to par value. Capital trust and other long-term debt instruments were valued using market quotes. Interest Rate Swaps, Equity Contracts... -

Page 100

... guarantees inherent in the Company's business operations such as indemniï¬ed securities lending programs and merchant charge-back guarantees; indemniï¬cation or buy-back provisions related to certain asset sales; and contingent consideration arrangements related to acquisitions. For certain... -

Page 101

...Company currently processes card transactions for airlines, cruise lines and large tour operators in the United States, Canada and Europe. In the event of liquidation of these merchants, the Company could become ï¬nancially liable for refunding tickets purchased through the credit card associations... -

Page 102

... on the ï¬nancial condition, results of operations or cash ï¬,ows of the Company. business, the Company may enter into revenue share agreements with third party business partners who generate customer referrals or provide marketing or other services related to the generation of revenue. In certain... -

Page 103

... Available-for-sale securities Investments in bank and bank holding company subsidiaries Investments in nonbank subsidiaries Advances to bank subsidiaries Advances to nonbank subsidiaries Other assets Total assets LIABILITIES AND SHAREHOLDERS' EQUITY Short-term funds borrowed Long-term... -

Page 104

...806 Transfer of funds (dividends, loans or advances) from bank subsidiaries to the Company is restricted. Federal law requires loans to the Company or its afï¬liates to be secured and generally limits loans to the Company or an individual afï¬liate to 10 percent of each bank's unimpaired capital... -

Page 105

...) 2006 2005 2004 2003 2002 % Change 2006 v 2005 ASSETS Cash and due from banks Held-to-maturity securities Available-for-sale securities Loans held for sale Loans Less allowance for loan losses Net loans Other assets Total assets LIABILITIES AND SHAREHOLDERS' EQUITY Deposits Noninterest... -

Page 106

... INCOME Credit and debit card revenue Corporate payment products revenue ATM processing services Merchant processing services Trust and investment management fees Deposit service charges Treasury management fees Commercial products revenue Mortgage banking revenue Investment products fees... -

Page 107

... INCOME Credit and debit card revenue Corporate payment products revenue ATM processing services Merchant processing services Trust and investment management fees Deposit service charges Treasury management fees Commercial products revenue Mortgage banking revenue Investment products fees... -

Page 108

... assets Total earning assets Allowance for loan losses Unrealized gain (loss) on available-for-sale securities Other assets (c Total assets LIABILITIES AND SHAREHOLDERS' EQUITY Noninterest-bearing deposits Interest-bearing deposits Interest checking Money market savings Savings accounts... -

Page 109

Related Yields and Rates (a) 2004 Average Balances Yields and Rates Average Balances 2003 Yields and Rates Average Balances 2002 Yields and Rates 2006 v 2005 % Change Average Balances Interest Interest Interest $ 43,009 3,079 39,348 27,267 14,322 39,733 120,670 1,365 168,123 (2,303) (346) 26,119... -

Page 110

... Stock Exchange, under the ticker symbol ''USB.'' STOCK PERFORMANCE CHART The following chart compares the cumulative total shareholder return on the Company's common stock during the ï¬ve years ended December 31, 2006, with the cumulative total return on the Standard & Poor's 500 Commercial Bank... -

Page 111

... incorporated in the Form 10-K. Index Page U.S. Bancorp Incorporated in the State of Delaware IRS Employer Identiï¬cation #41-0255900 Address: 800 Nicollet Mall Minneapolis, Minnesota 55402-7014 Telephone: (651) 466-3000 Securities registered pursuant to Section 12(b) of the Act (and listed on the... -

Page 112

... the Bank Holding Company Act of 1956. U.S. Bancorp provides a full range of ï¬nancial services, including lending and depository services, cash management, foreign exchange and trust and investment management services. It also engages in credit card services, merchant and ATM processing, mortgage... -

Page 113

... other commercial banks, savings and loan associations, mutual savings banks, ï¬nance companies, mortgage banking companies, credit unions and investment companies. In addition, technology has lowered barriers to entry and made it possible for non-banks to offer products and services traditionally... -

Page 114

... risk of fraud by employees or persons outside of the Company, the execution of unauthorized transactions by employees, errors relating to transaction processing and technology, breaches of the internal control system and compliance requirements and business continuation and disaster recovery. This... -

Page 115

... accrued taxes liability. For more information, refer to ''Critical Accounting Policies'' in this Annual Report and Form 10-K. Changes in accounting standards could materially impact the Company's financial statements. From time to time, the to acquire ï¬nancial services businesses or assets and... -

Page 116

... the Company's business. Third party vendors provide key components of the Company's business infrastructure such as internet connections, network access and mutual fund distribution. While the Company has selected these third party vendors carefully, it does not control their actions. Any problems... -

Page 117

...Access to SEC Reports U.S. Bancorp's internet Governance Guidelines, Code of Ethics and Business Conduct and Board of Directors committee charters are available free of charge on the Company's web site at usbank.com, by clicking on ''About U.S. Bancorp,'' then ''Corporate Governance.'' Shareholders... -

Page 118

... request made to the Investor Relations contact listed inside the back cover of this Annual Report and Form 10-K. The following table identiï¬es the (i) closing date for each transaction, (ii) issuer, (iii) series of Capital Securities, Preferred Stock or Exchangeable Preferred Stock issued in the... -

Page 119

... since the required information is included in the footnotes or is not applicable. The following Exhibit Index lists the Exhibits to the Annual Report on Form 10-K. (1)(2) 10.9 U.S. Bancorp Executive Deferral Plan, as amended. Filed as Exhibit 10.7 to Form 10-K for the year ended December 31... -

Page 120

... quarterly period ended March 31, 2005 10.36 Terms of Jerry A. Grundhofer's service as Non-Executive Chairman of the Board of Directors. Described in Item 1 of Form 8-K ï¬led on July 20, 2006 10.37 Agreement with David M. Moffett dated January 19, 2007 Statement re: Computation of Ratio of Earnings... -

Page 121

...on its behalf by the undersigned, thereunto duly authorized. U.S. Bancorp By: Richard K. Davis President and Chief Executive Ofï¬cer Pursuant to the requirements of the Securities Exchange Act of 1934, this report has been signed below on February 26, 2007, by the following persons on behalf of the... -

Page 122

... 31.1 CERTIFICATION PURSUANT TO RULE 13a-14(a) UNDER THE SECURITIES EXCHANGE ACT OF 1934 I, Richard K. Davis, certify that: (1) I have reviewed this Annual Report on Form 10-K of U.S. Bancorp; (2) Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to... -

Page 123

... 31.2 CERTIFICATION PURSUANT TO RULE 13a-14(a) UNDER THE SECURITIES EXCHANGE ACT OF 1934 I, David M. Moffett, certify that: (1) I have reviewed this Annual Report on Form 10-K of U.S. Bancorp; (2) Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to... -

Page 124

...of the Securities Exchange Act of 1934; and (2) The information contained in the Form 10-K fairly presents, in all material respects, the ï¬nancial condition and results of operations of the Company. /s / RICHARD K. DAVIS Richard K. Davis Chief Executive Ofï¬cer Dated: February 26, 2007 /s / DAVID... -

Page 125

... Bancorp. From the time of the merger, Mr. Davis was responsible for Consumer Banking, including Retail Payment Solutions (card services), and he assumed additional responsibility for Commercial Banking in 2003. Previously, he had been Vice Chairman of Consumer Banking of Firstar Corporation from... -

Page 126

..., 59, has served in this position since July 2006, when he joined U.S. Bancorp to assume responsibility for Corporate Banking. Prior to joining U.S. Bancorp, he served as Executive Vice President for National City Corporation in Cleveland, with responsibility for Capital Markets, since 2001. 124... -

Page 127

...3. 4. 5. 6. Executive Committee Compensation Committee Audit Committee Community Outreach and Fair Lending Committee Governance Committee Credit and Finance Committee David B. O'Maley 5,6 Chairman, President and Chief Executive Ofï¬cer Ohio National Financial Services, Inc. Cincinnati, Ohio O'dell... -

Page 128

-

Page 129

corporate information Executive Offices U.S. Bancorp 800 Nicollet Mall Minneapolis, MN 55402 Common Stock Transfer Agent and Registrar Mellon Investor Services acts as our transfer agent and registrar, dividend paying agent and dividend reinvestment plan administrator, and maintains all shareholder ... -

Page 130

U.S. Bancorp 800 Nicollet Mall Minneapolis, MN 55402 usbank.com