Tesco 2005 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2005 Tesco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68

|

|

58 Tesco PLC

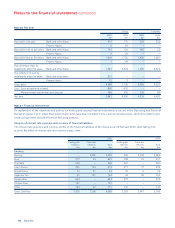

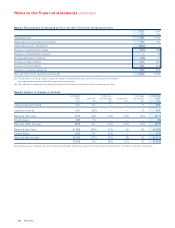

Notes to the financial statements continued

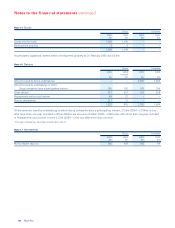

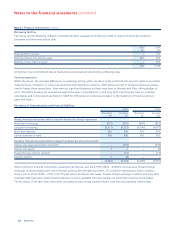

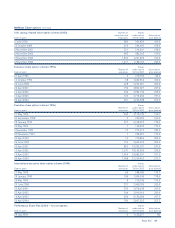

Note 27 Pensions

The Group has continued to account for pensions and other post-employment benefits in accordance with SSAP 24 and the

disclosures in note (a) below are those required by that standard. FRS 17, ‘Retirement Benefits’ was issued in November 2000,

and the transitional disclosures required by that standard, to the extent they are not given in note (a), are set out in note (b).

For the financial period ending April 2006 the Group will adopt International Accounting Standard 19.

The last full actuarial valuation of the main UK scheme was carried out as at 31 March 2002. The next full valuation will be

performed as at 31 March 2005 and the results will not be known until the end of the financial period. An additional contribution

of £200m was made in February 2005 to reduce the expected increase in the actuarial deficit since the last full valuation. Any

decision as to the level of future contributions will be made once the results of the March 2005 valuation are known.

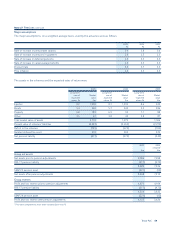

(a) Pension commitments

United Kingdom

The principal plan within the Group is the Tesco PLC Pension Scheme, which is a funded defined benefit pension scheme in

the UK, the assets of which are held as a segregated fund and administered by trustees. The total profit and loss charge of UK

schemes to the Group during the year was £218m (2004 – £152m). A SSAP 24 pension prepayment of £221m (2004 – £12m)

is present in the Group balance sheet, which includes the additional contribution of £200m.

An independent actuary, using the projected unit method, carried out the latest actuarial assessment of the scheme at 31 March

2002. The assumptions that have the most significant effect on the results of the valuation are those relating to the rate of return

on investments and the rate of increase in salaries and pensions.

The key assumptions made were a rate of return on investments of 6.75%, a rate of increase in salaries of 4% and a rate

of increase in pensions of 2.6%.

At the date of the last actuarial valuation, the market value of the scheme’s assets was £1,576m and the actuarial value of these

assets represented 91% of the benefits that had accrued to members, after allowing for expected future increases in earnings and

pensions in payment. The actuarial shortfall of £159m will be met via increased contributions over a period of ten years, being the

expected average remaining service lifetime of employed members.

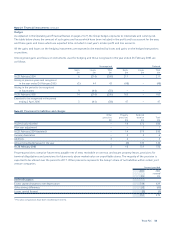

The T&S Stores Senior Executive Pension Scheme is a funded defined benefit scheme open to senior executives and certain other

employees at the invitation of the company. An independent actuary, using the projected unit method, carried out the latest

actuarial assessment of the scheme as at 6 April 2001. At that time, the market value of the scheme’s assets was £5.8m and the

actuarial value of these assets represented 110% of the benefits that had accrued to members, after allowing for expected future

increases in earnings.

Overseas

The Group operates a number of schemes worldwide, which include defined benefit and defined contribution schemes. The

contributions payable for non-UK schemes of £10m (2004 – £8m) have been fully expensed against profits in the current year.

A funded defined benefit scheme operates in the Republic of Ireland. An independent actuary, using the projected unit method,

carried out the latest actuarial assessment of the scheme as at 1 April 2004. At that time the market value of the scheme’s assets

was £62m and the actuarial value of these assets represented 99% of the benefits that had accrued to members, after allowing

for expected future increases in earnings.

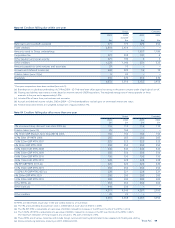

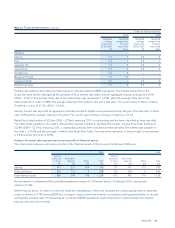

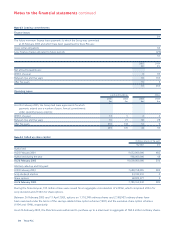

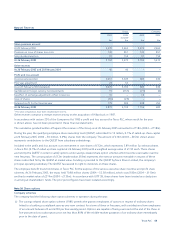

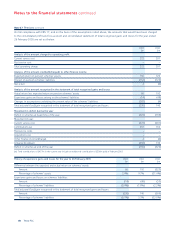

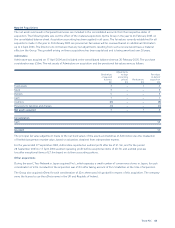

(b) FRS 17, ‘Retirement Benefits’

The valuations used for FRS 17 have been based on the most recent actuarial valuations and updated by Watson Wyatt LLP to

take account of the requirements of FRS 17 in order to assess the liabilities of the schemes at 26 February 2005. Schemes’ assets

are stated at their market values at 26 February 2005. Heissmann Consultants (Ireland) Limited have updated the most recent

Republic of Ireland valuation. The liabilities relating to post-retirement healthcare benefits (note 28) have also been determined

in accordance with FRS 17, and are incorporated in the following tables.