Tesco 2005 Annual Report Download - page 5

Download and view the complete annual report

Please find page 5 of the 2005 Tesco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

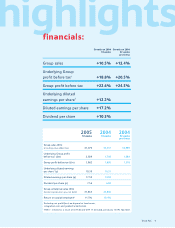

During the second half, like-for-like sales

increased by 9.5% including petrol and by

7.4%, excluding petrol.

UK underlying operating profit was 11.0%

higher at £1,694m (2004 – £1,526m). The

operating margin was maintained at 6.2%.

International Total international sales grew by

13.1% to £7.6bn and by 18.3% at constant

exchange rates. International operations

contributed £370m to underlying operating

profit, up 20.9% on last year, with operating

margins rising to 5.4% (2004 – 5.1%). At

constant exchange rates, international profit

grew by 26.5%.

In the Rest of Europe, sales rose by 13.4% to

£4.3bn (2004 – £3.8bn). At constant exchange

rates, sales grew by 15.7%. Underlying operating

profit increased by 18.5% to £218m (2004 –

£184m). In Asia, sales grew by 12.8% to £3.2bn

(2004 – £2.8bn). At constant exchange rates,

sales grew by 21.8%. Underlying operating profit

increased by 24.6% to £152m (2004 – £122m).

Joint Ventures and Associates Our total share

of profit (excluding goodwill amortisation) for

the year was £135m compared to £99m last

year. Tesco Personal Finance pre-tax profit post

minority interest was £202m, of which our share

was £101m, up 26.5% on last year.

Net interest payable was £170m (2004 – £223m),

giving cover of 12.5 times (2004 – 8.2 times). Tax

has been charged at an effective rate of 30.2%

(2004 – 31.1%). Prior to accounting for the net

profit on disposal of fixed assets, resulting mainly

from the property joint venture with Topland

announced in March 2004, as well as goodwill

amortisation and integration costs, our

underlying tax rate was 29.5% (2004 – 29.5%).

Underlying diluted earnings per share increased

by 12.2% to 18.30p (2004 – 16.31p).

Cash Flow and Balance Sheet The Group

generated net cash of £121m during the year,

benefiting from a strong operating cash inflow of

£3bn, after an additional £200m contribution to

the Group pension scheme and the net proceeds

of £646m from our property joint venture with

Topland. Net debt reduced to £3.8bn at the year

end, representing gearing of 43% (2004 – 51%).

After year end we generated around £350m

from our most recent property joint venture with

the Consensus Business Group.

Group capital expenditure during the year

(excluding acquisitions but including the ten

Safeway stores purchased from Morrisons) was

£2.4bn (2004 – £2.3bn). We expect Group capital

expenditure to be around £2.4bn this year. UK

capital expenditure was £1.7bn (2004 – £1.5bn),

including £835m on new stores and £288m on

extensions and refits. Total international capital

expenditure was £746m (2004 – £765m)

comprising £282m in Asia and £464m in Europe.

Dividends The Board has proposed a final

dividend of 5.27p per share (2004 – 4.77p). This

represents an increase of 10.5%. Together with

the interim dividend of 2.29p (2004 – 2.07p)

already paid, this brings the full year dividend

to 7.56p, also an increase of 10.5% on last year.

The final dividend will be paid on 1 July 2005 to

shareholders on the Register of Members at the

close of business on 22 April 2005. Shareholders

will continue to have the right to receive the

dividend in the form of fully paid ordinary shares

instead of cash. The first day of dealing in the

new shares will be 1 July 2005.

Total Shareholder Return Total Shareholder

Returns (TSR), which is measured as the

percentage change in the share price, plus the

dividend paid, has increased by 108.7% over

the last five years, compared to the decrease

in the FTSE 100 average of 6.2%. Over the

last three years, Tesco TSR has been 34.5%,

compared to the FTSE 100 average of 8.8%.

In the last year, the return in Tesco was 25.1%,

compared to the FTSE 100 average of 15.0%.

Return on Capital Employed (ROCE). At the time

of our share placing in January 2004, we believed

we could increase our 2002/03 financial year post

tax ROCE of 10.2% by up to 200 basis points

over five years based on then current plans. The

excellent progress we have made in the year,

combined with the effect of the Topland property

funding initiative, means that post tax ROCE rose

to 11.5%.

Tesco PLC 3

01 02 0403

CAPITAL EXPENDITURE

£m

2,134

2,027

1,944

1,228

2,285 1,520

05

2,417 1,671

1,276

1,206

GROUP

UK

1 year 3 years 5 years

TOTAL SHAREHOLDER RETURN

RELATIVE TO THE FTSE 100

114.9

25.7

10.1

01 0302

UK SALES AREA OPENED

000 s

q

ft

1,433

04

1,778

05

1,519

1,296

1,298