Sunoco 2015 Annual Report Download - page 9

Download and view the complete annual report

Please find page 9 of the 2015 Sunoco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

|

|

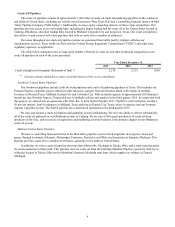

7

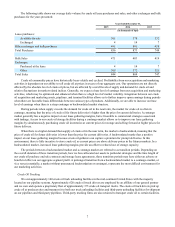

The following table shows our average daily volume for crude oil lease purchases and sales, and other exchanges and bulk

purchases for the years presented:

Year Ended December 31,

2015 2014 2013

(in thousands of bpd)

Lease purchases:

Available for sale 361 378 332

Exchanged 4 14 7

Other exchanges and bulk purchases 491 481 410

Total Purchases 856 873 749

Bulk Sales 471 483 419

Exchanges:

Purchased at the lease 4 14 7

Other 369 372 321

Total Sales 844 869 747

Crude oil commodity prices have historically been volatile and cyclical. Profitability from our acquisition and marketing

activities is dependent on our ability to sell crude oil at prices in excess of our aggregate cost. Our operations are not directly

affected by the absolute level of crude oil prices, but are affected by overall levels of supply and demand for crude oil and

relative fluctuations in market-related indices. Generally, we expect a base level of earnings from our acquisition and marketing

activities, which may be optimized and enhanced when there is a high level of market volatility. Integration between our crude

oil acquisition and marketing assets, pipelines, and terminal facilities allows us to further improve upon earnings during periods

when there are favorable basis differentials between various types of products. Additionally, we are able to increase our base

level of earnings when there is a steep contango or backwardated market structure.

During periods when supply exceeds the demand for crude oil in the near term, the market for crude oil is often in

contango, meaning that the price of crude oil for future deliveries is higher than the price for current deliveries. A contango

market generally has a negative impact on our lease gathering margins, but is favorable to commercial strategies associated

with tankage. Access to our crude oil storage facilities during a contango market allows us to improve our lease gathering

margins by simultaneously purchasing crude oil inventories at current prices for storage and selling forward at higher prices for

future delivery.

When there is a higher demand than supply of crude oil in the near term, the market is backwardated, meaning that the

price of crude oil for future deliveries is lower than the price for current deliveries. A backwardated market has a positive

impact on our lease gathering margins because crude oil gatherers can capture a premium for prompt deliveries. In this

environment, there is little incentive to store crude oil, as current prices are above delivery prices in the futures markets. In a

backwardated market, increased lease gathering margins provide an offset to reduced use of storage capacity.

The periods between a backwardated market and a contango market are referred to as transition periods. Depending on

the overall duration of these transition periods, how we have allocated our assets to particular strategies and the time length of

our crude oil purchase and sale contracts and storage lease agreements, these transition periods may have either an adverse or

beneficial effect on our aggregate segment profit. A prolonged transition from a backwardated market to a contango market, or

vice versa (essentially, a market without pronounced backwardation or contango), represents the most difficult environment for

our marketing activities.

Crude Oil Trucking

We own approximately 140 crude oil truck unloading facilities in the mid-continent United States with the majority

located on our pipeline systems. Approximately 620 crude oil truck drivers are employed by an affiliate of our general partner

and we own and operate a proprietary fleet of approximately 375 crude oil transport trucks. The crude oil truck drivers pick up

crude oil at producer sites and transport it to both our truck unloading facilities and third-party unloading facilities for shipment

on our pipelines and third-party pipelines. Third-party trucking firms are also retained to transport crude oil to certain facilities.