RBS 2013 Annual Report Download - page 331

Download and view the complete annual report

Please find page 331 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

338 -

339

339 -

340

340 -

341

341 -

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

Business review Risk and balance sheet management

329

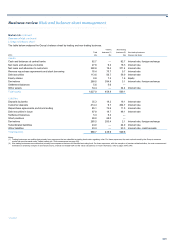

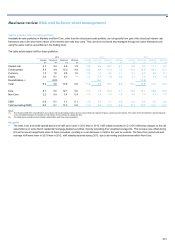

Risks not in VaR (RNIVs)*

The table below analyses capital requirements related to RNIVs.

2013 2012

£m £m

Risks Not in VaR (RNIV) 30 94

Risks Not in SVaR (RNISV) 39 149

Stressed RNIV (SRNIV) 149 187

218 430

Key points

• The decreases in the VaR RNIV and SVaR RNIV were driven by

progress in obtaining reliable sources of equity market data and by

an improvement in the VaR model for asset-backed products.

• The decrease in the Stressed RNIV primarily reflected a reduction in

RBSSI’s asset-backed products exposures.

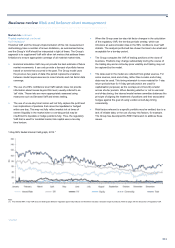

Stress testing*

The Group undertakes daily market risk stress testing to identify

vulnerabilities and potential losses in excess of or not captured in VaR.

The calculated stresses measure the impact of changes in risk factors on

the fair values of the Group’s trading and available-for-sale portfolios.

The Group conducts scenario-based sensitivity analysis and historical,

macroeconomic and bottom-up stress testing.

Scenario-based sensitivity analysis measures the sensitivity of the

current portfolio to defined movements in market risk factors. These risk

factor movements and the resulting valuation changes are typically

smaller than those considered in other stress tests.

Historical stress testing is a measure that is used for internal

management. Using a similar technical framework to VaR, the current

portfolio is stressed using historical data since 1 January 2005. The

methodology simulates the impact of the worst loss that would be

incurred by historical risk factor movements over the period, assuming a

holding period specific to the risk factors and the businesses. At present,

a holding period of 60 business days is applied for credit risk factors

(including in the case of ABS) and for the AFS portfolios that are held by

Markets Treasury and generally a period of 10 business days for other

risk factors. The Group reviews the holding periods annually and is

considering introducing greater distinction between the liquidity

assumptions associated with each risk factor.

The main strength of this methodology is that it is founded on objective

data and the potential loss is directly informed by real-life examples. As

with all historically based methodologies, an obvious limitation is that the

approach it is not forward-looking. However, this weakness is materially

addressed by the other stress testing approaches that constitute the RBS

stress testing framework.

Historical stress tests form part of the Group market risk limit framework

and their results are reported daily to senior management.

*unaudited

Macroeconomic stress tests are carried out periodically as part of the

firm-wide, cross-risk capital planning process. The scenario narratives

are translated into risk factor shocks using historical events and insights

by economists, risk managers and the front office. Market risk stress

results are combined with those for other risks into the capital plan that is

presented to the Board. The cross-risk capital planning process is

conducted twice a year, in April/May and October/November, with a

planning horizon of five years. The scenario narratives cover both

regulatory scenarios such as the PRA Anchor and Fed Stress

comprehensive capital assessment review (CCAR) and macroeconomic

scenarios identified by the firm such as a Euro Break-Up and the US

Fiscal Cliff.

Bottom-up stress testing begins with the analysis of a portfolio and

expresses the key vulnerabilities of the portfolio in terms of plausible, so-

called vulnerability scenarios under which the portfolio would suffer

material losses. These scenarios can be historical, forward-looking,

macroeconomic or hypothetical. Bottom-up stress testing is used for

internal management information and is not subject to limits. However,

relevant scenarios are reported to senior management.

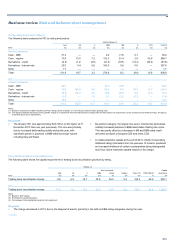

Economic capital

A market risk economic capital framework was developed in 2013 and

will be introduced in the Group’s internal reporting during 2014.

The associated models calculate the market and default risk in the

trading book. The results are annualised to be consistent with the other

Group economic capital models to permit consolidation of all risk types as

part of the Group-wide economic capital programme.

Other risk measures

In addition to SVaR and stress tests, the Group uses a range of other risk

measures to complement VaR. These measures often represent local

(small-amplitude) risk calculations which provide valuable additional

controls, often at individual desk or business unit level. They mainly

include, but are not limited to, sensitivity and position-based risk

measures.

Sensitivity measures refer to the changes in deal or portfolio value that

result from small changes in market parameters that are subject to the

Group market risk limit framework.

Position-based measures are also used and are stated in terms that

relate directly to the business activity they are applied to. Examples of

such measures include the aggregate open foreign exchange position or

the long, short and net amount of security or currency held and aged

inventory in trading books.