RBS 2013 Annual Report Download - page 189

Download and view the complete annual report

Please find page 189 of the 2013 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

|

|

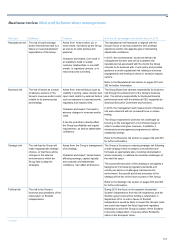

Business review Risk and balance sheet management

187

Risk coverage

The Group continued to strengthen its approach to risk management

amid a challenging and ever-changing external environment in 2013.

Areas of progress included:

• The completion of the phased roll-out of the Group's conduct risk

policies and of a more effective operating model, supported by the

development and delivery of awareness initiatives and targeted

training;

• The implementation of the enhanced country risk appetite

framework, including top-down risk appetite, and of enhanced

assurance processes;

• The introduction of a new integrated operating model for managing

regulatory developments, which combines divisional and functional

teams to leverage expertise more effectively; and

• Further strengthening of the Group’s credit risk management

framework.

The main risk types faced by the Group are presented below, together with a summary of the key areas of focus and how the Group managed these

risks in 2013. In preparing disclosures related to these risks, the Group has considered the recommendations of the Enhanced Disclosure Task Force

issued in October 2012. A summary of the recommendations and list of disclosures that meet these recommendations has been included on page 557.

Risk type Definition Features How the Group manages risk and the focus in 2013

Capital adequacy

risk

The risk that the Group has

insufficient capital.

Arises from: Inefficient management

of capital resources.

Character and impact: Characterised

typically by credit risk losses.

It has the potential to disrupt the

business if there is insufficient capital

to support business activities. It also

has the potential to cause the Group

to fail to meet regulatory

requirements. Group capital and

earnings may be affected, impairing

the activities of all divisions.

The Group’s Core Tier 1 ratio on a Basel 2.5 basis was

10.9% and on a fully loaded Basel III (FLB3) basis was

8.6% at 31 December 2013. The Group is targeting a

FLB3 Common Equity Tier 1 ratio of c.11% by the end of

2015 and 12% or above by the end of 2016. The timely

run-down of RCR and the successful divestment of

Citizens are key to the achievement of the Group’s capital

plans.

Refer to the Capital management section on pages 192 to

208 for further information.

Liquidity and

funding risk

The risk that the Group is

unable to meet its financial

liabilities as they fall due.

Arises from: The Group’s day-to-day

operations.

Character and impact: Dependent on

company-specific factors such as

maturity profile and composition of

sources and uses of funding, the

quality and size of the liquid asset

buffer as well as broader market

factors, such as wholesale market

conditions alongside depositor and

investor behaviour.

It has the potential to cause the Group

to fail to meet regulatory liquidity

requirements, become unable to

support normal banking activity or at

worst cease to be a going concern.

Adverse impact on customer and

investor confidence in the Group and

the wider financial system is also

possible.

Liquidity and funding metrics continued to strengthen with

short-term wholesale funding of £32.4 billion, covered

more than four times by a liquidity portfolio of £146.1

billion. Liquidity coverage and net stable funding ratios

also improved.

Refer to the Liquidity and funding risk section on pages

209 to 226 for further information.

*unaudited