Progressive 2012 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2012 Progressive annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

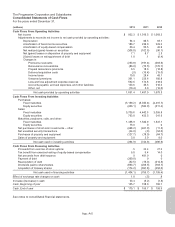

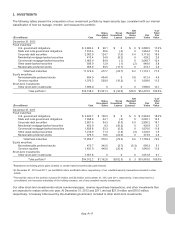

Other-than-Temporary Impairment (OTTI) The following table shows the total non-credit portion of the OTTI recorded in

accumulated other comprehensive income, reflecting the original non-credit loss at the time the credit impairment was

determined:

December 31,

(millions) 2012 2011

Fixed maturities:

Residential mortgage-backed securities $(44.2) $(44.8)

Commercial mortgage-backed securities (.9) (1.0)

Total fixed maturities $(45.1) $(45.8)

The following tables provide rollforwards of the amounts related to credit losses recognized in earnings for the periods

ended December 31, 2012 and 2011, for which a portion of the OTTI losses were also recognized in accumulated other

comprehensive income at the time the credit impairments were determined and recognized:

(millions)

Residential

Mortgage-

Backed

Commercial

Mortgage-

Backed

Corporate

Debt Total

Beginning balance at January 1, 2012 $34.5 $1.3 $ 0 $35.8

Credit losses for which an OTTI was previously recognized .1 0 0 .1

Credit losses for which an OTTI was not previously recognized .3 0 0 .3

Reductions for securities sold/matured 0 (.2) 0 (.2)

Change in recoveries of future cash flows expected to be collected1,2 (3.8) (.2) 0 (4.0)

Reductions for previously recognized credit impairments

written-down to fair value3(4.0) (.3) 0 (4.3)

Ending balance at December 31, 2012 $27.1 $ .6 $ 0 $27.7

(millions)

Residential

Mortgage-

Backed

Commercial

Mortgage-

Backed

Corporate

Debt Total

Beginning balance at January 1, 2011 $32.3 $1.0 $ 6.5 $39.8

Credit losses for which an OTTI was previously recognized 1.4 0 0 1.4

Credit losses for which an OTTI was not previously recognized 1.1 .4 0 1.5

Reductions for securities sold/matured 0 0 0 0

Change in recoveries of future cash flows expected to be collected1,2 .8 .3 (6.5) (5.4)

Reductions for previously recognized credit impairments

written-down to fair value3(1.1) (.4) 0 (1.5)

Ending balance at December 31, 2011 $34.5 $1.3 $ 0 $35.8

1Reflects expected recovery of prior period impairments that will be accreted into income over the remaining life of the security.

2Includes $1.4 million and $2.0 million at December 31, 2012 and 2011, respectively, received in excess of the cash flows expected to be collected

at the time of the write-downs.

3Reflects reductions of prior credit impairments where the current credit impairment requires writing securities down to fair value (i.e., no remaining

non-credit loss).

Although we determined that it is more likely than not that we will not be required to sell the securities prior to the recovery

of their respective cost bases (which could be maturity), we are required to measure the amount of credit losses on the

securities that were determined to be other-than-temporarily impaired. In that process, we considered a number of factors

and inputs related to the individual securities. The methodology and significant inputs used to measure the amount of credit

losses in our portfolio included: current performance indicators on the underlying assets (e.g., delinquency rates,

foreclosure rates, and default rates); credit support (via current levels of subordination); historical credit ratings; and

updated cash flow expectations based upon these performance indicators. In order to determine the amount of credit loss, if

any, the net present value of the cash flows expected (i.e., expected recovery value) was calculated using the current book

yield for each security, and was compared to its current amortized value. In the event that the net present value was below

the amortized value, a credit loss was deemed to exist, and the security was written down.

App.-A-14