Navy Federal Credit Union 2005 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2005 Navy Federal Credit Union annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49

|

|

17

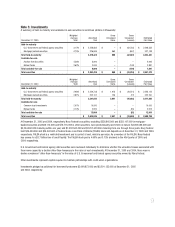

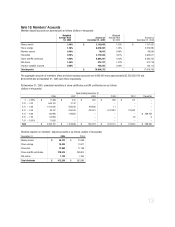

Note 15: Reserves and Undivided Earnings

Navy Federal is subject to regulatory capital requirements adminis-

tered by the NCUA. Failure to meet minimum capital requirements

can initiate certain mandatory—and possibly additional discre-

tionary—actions by regulators that, if undertaken, could have a

direct material effect on Navy Federal’s consolidated financial

statements. Under capital adequacy regulations and the regulatory

framework for prompt corrective action, Navy Federal must meet

specific capital requirements that involve quantitative measures

of Navy Federal’s assets, liabilities and certain commitments as

calculated under generally accepted accounting principles. Navy

Federal’s capital amounts and net worth classification are also

subject to qualitative judgments by the regulators about

components, risk weightings and other factors.

Quantitative measures established by regulation to ensure capital

adequacy require Navy Federal to maintain minimum amounts and

ratios (set forth in the following table) of net worth to total assets.

Credit unions are also required to calculate a risk-based net worth

(RBNW) requirement that establishes whether the credit union will

be considered “complex” under the regulatory framework. Navy

Federal’s RBNW requirement as of December 31, 2005, was 4.60%,

which is less than the regulatory threshold of 6% that would place

Navy Federal in the “complex” category. Management believes as

of December 31, 2005, that Navy Federal met all RBNW capital

adequacy requirements to which it is subject.

As of December 31, 2005, the most recent call reporting period,

the NCUA categorized Navy Federal as “well capitalized” under the

regulatory framework for prompt corrective action with a net worth

of 10.92%. Net worth for this calculation is defined as undivided

earnings plus regular and capital reserves. To be categorized as

“well capitalized,” Navy Federal must maintain a minimum net

worth ratio of 7% of assets. There are no conditions or events

since that notification that management believes have changed

the institution’s category.

The Credit Union’s actual capital amounts and ratios as of

December 31, 2005 and 2004 are also presented in the table

(dollars in thousands):

Actual Net Worth Minimum Net Worth to be

“Well Capitalized”

Amount Ratio Amount Ratio

Dec. 31,

2005 $ 2,692,430 10.92% $ 1,725,105 7.00%

Dec. 31,

2004 $ 2,426,117 10.60% $ 1,602,785 7.00%