Navy Federal Credit Union 2005 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2005 Navy Federal Credit Union annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49

|

|

11

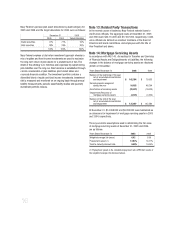

Note 5: Derivative Instruments and Economic

Hedging Activities

Navy Federal is an active participant in the production of mortgage

loans which are sold to investors in the secondary market. This

mortgage banking activity involves making mortgage loan commit-

ments to members at specified interest rates. Navy Federal is

exposed to changes in the value of its mortgage loan commitments

as interest rates may change between the time that it enters into a

mortgage loan commitment and the time that it ultimately delivers

mortgage loans to investors. To protect against this interest rate

risk, Navy Federal enters into forward sales contracts at specified

prices to deliver mortgage loans to investors. These forward sales

commitments act as an economic hedge against the risk of

changes in the value of both the mortgage loan commitments and

mortgage loans held for sale. As required by FAS 133,

Accounting

for Derivative Instruments and Hedging Activities,

as amended and

interpreted, Navy Federal accounts for both the mortgage loan

commitments and the forward sales contracts as derivative instru-

ments on its Consolidated Statements of Financial Condition as fair

value with changes in fair value included in current earnings. These

derivative instruments are economic hedges to which Navy Federal

does not receive hedge accounting treatment.

The notional value of the mortgage loan commitments totaled

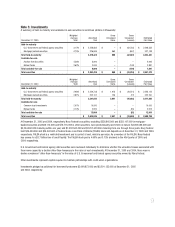

$206,241,000 and $208,999,000, respectively, as of December 31,

2005 and 2004. A net loss of $1,516,000 and $1,205,000 on

the mortgage loans commitment derivative was reported in the

Statement of Financial Condition at December 31, 2005 and

2004, respectively.

The notional value of the forward sales contracts was $370,040,000

and $382,751,000, respectively, as of December 31, 2005 and 2004.

A net loss of $1,315,000 and a net gain of $1,117,000 on the

forward sales contracts derivative was reported in the Statement

of Financial Condition at December 31, 2005 and 2004, respectively.

The net change in the fair value of these derivative instruments

was a loss of $2,744,000 and $2,199,000 during the years ended

December 31, 2005 and 2004, respectively, and was included in

earnings as “Unrealized loss from derivative and economic hedging

activities” in the Statement of Operations.

Note 6: Legal Contingencies

Navy Federal is a party to various legal actions normally associated

with financial institutions, the aggregate effect of which, in man-

agement’s and legal counsel’s opinion, would not be material to the

financial condition or results of operations of Navy Federal.

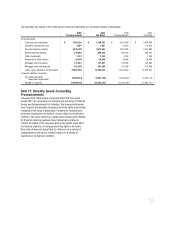

Note 7: Commitments

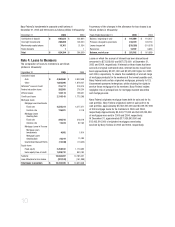

Navy Federal is a party to conditional commitments to lend funds

in the normal course of business to meet the financing needs of

its members. Unused commitments for loans to members are

amounts which Navy Federal has agreed to lend a member as long

as the member does not default on existing loans or violate any

condition of the loan agreement. Commitments generally have fixed

expiration dates or other termination clauses. Since many of the

commitments are expected to expire without being drawn upon,

the total commitment amounts do not necessarily represent future

cash requirements. Navy Federal uses the same credit policies

in making commitments as it does for all loans to members and,

accordingly, at December 31, 2005, the credit risk related to these

commitments was similar to that on its existing loans.

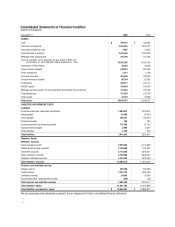

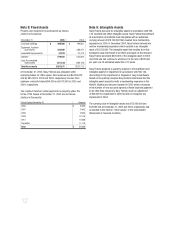

The following financial instruments were outstanding in 2005 and

2004

(dollars in thousands):

Unused commitments: 2005 2004

Credit cards $ 3,958,828 $ 3,504,353

NAVchek lines of credit 527,916 511,654

Home equity lines of credit 1,101,992 839,361

Preapproved auto loans 160,638 122,960

Utility deposit guarantee

programs 2,855 2,594

Letter of credit 7,500 7,500

Total $ 5,759,729 $ 4,988,422