Mercury Insurance 2008 Annual Report Download - page 5

Download and view the complete annual report

Please find page 5 of the 2008 Mercury Insurance annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

• Implement best practices and standardized proce-

dures across all functions.

• Simplify our processes for greater efficiency and

improved customer service.

• Increase customer reach by leveraging the Internet

more effectively and increasing the number of rela-

tionships with qualified agents.

• Continue our Service Excellence program, which

was rolled out in 2008.

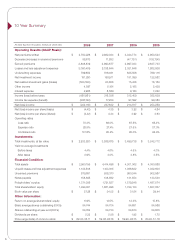

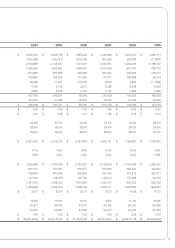

Quite clearly, our investment results in 2008 were

significantly impacted by the decline in the capital

markets as a result of the financial crisis and global

recession. About half of Mercury’s losses came from

our municipal bond portfolio. Nevertheless, the port-

folio still remains in very good shape, with an aver-

age rating of AA, and we expect most of our bonds

to recover to their par value. Our equity investments

were down about 50% for the year. Historically, the

portfolio has provided many years of successful

returns. Unfortunately, in 2008, all of the previous

gains evaporated. The outlook for the equity markets

is very hard to discern, espe-

cially with so many new eco-

nomic policies coming to

bear. However, the market

value of our equity portfolio is

less at year-end 2008 than

year-end 2007, with the per-

centage of equities to total

invested assets declining

from 12% to 8%. The Company will maintain most of

the current positions as long as we are satisfied with

the return potential.

Net investment income, which excludes realized

gains and losses, was $133.7 million after-tax, com-

pared to $137.8 million in 2007. The decrease in

income was attributable to a reduction in the amount

of invested assets and in the after tax yield from

4.0% in 2007 to 3.9% in 2008.

We ended the year with a very strong capital posi-

tion, despite the declines in the value of our invest-

ment portfolio. At year-end, our Shareholders’ Equity

was $1.5 billion and our underwriting leverage

remains conservative, with a premium to surplus

ratio of 2 to 1. In February 2009, Mercury’s Board of

Directors kept the dividend rate unchanged at $0.58

cents per share, providing a generous dividend yield

based on the recent market price of our stock. We

will continue to evaluate our dividend quarterly based

on our results and capital position.

In January of 2009, we completed our purchase of

AIS, a major producer of personal lines insurance in

the state of California. AIS represented approximately

15% of Mercury’s premium volume in 2008. We are

pleased to report that the transition and integration

efforts are going very smoothly and anticipate the

purchase of AIS will be slightly accretive to earnings

in 2009.

AIS will continue to operate as an independent

agency, maintaining virtually the same management

prior to our purchase. AIS is led by President and

CEO Mark Ribisi. Mark has spent his entire career in

the auto insurance industry and is a 20-year veteran

of AIS. We look forward to working with Mark and

his team as we continue to grow our business.

As we look ahead, the current year is sure to bring

its own challenges but we believe our long history of

stability, service and integrity puts us on solid ground to

weather the storm. We stand poised and ready for an

eventual economic recovery and look forward to end-

ing 2009 better than we found it. We hope you will be

able to attend our annual meeting on May 13, 2009.

Sincerely,

George Joseph

Chairman of the Board

Gabriel Tirador

President and Chief Executive Officer

We ended the year with

a very strong capital

position, despite the

declines in the value of

our investment portfolio.

3