Fannie Mae 2011 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2011 Fannie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

|

|

characteristics of our loan acquisitions, in more detail in “MD&A—Risk Management—Credit Risk

Management—Single-Family Mortgage Credit Risk Management.”

Whether the loans we acquire in the future will exhibit an overall credit profile similar to our more recent

acquisitions will depend on a number of factors, including our future pricing and eligibility standards and those

of mortgage insurers and FHA, the percentage of loan originations representing refinancings, our future

objectives, government policy, market and competitive conditions, and the volume and characteristics of loans

we acquire under the recently announced changes to the terms of HARP.

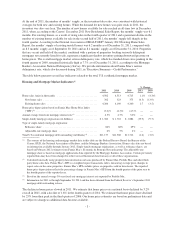

Expected Losses on Our Legacy Book of Business

The single-family credit losses we realized in 2009 through 2011, combined with the amounts we have reserved

for single-family credit losses as of December 31, 2011, as described below, total approximately $140 billion. A

substantial majority of these losses are attributable to single-family loans we purchased or guaranteed from 2005

through 2008.

While loans we acquired in 2005 through 2008 will give rise to additional credit losses that we will realize when

the loans are charged off (upon foreclosure or our acceptance of a short sale or deed-in-lieu of foreclosure), we

estimate that we have reserved for the substantial majority of the remaining losses on these loans. Even though

we believe a substantial majority of the credit losses we have yet to realize on these loans has already been

reflected in our results of operations as credit-related expenses, our credit-related expenses have remained high as

weakness in the housing and mortgage markets continues. We expect that our credit-related expenses will

continue to be high in 2012 but that, overall, our credit-related expenses will be lower in 2012 than in 2011. The

amount of credit-related expenses we incur each period will be affected by changes in expected and actual home

prices, modifications and foreclosure activity during the period.

We expect our loss reserves will remain significantly elevated relative to historical levels for an extended period

because (1) we expect future defaults on loans in our legacy book of business and the resulting charge-offs will

occur over a period of years and (2) a significant portion of our reserves represents concessions granted to

borrowers upon modification of their loans and will remain in our reserves until the loans are fully repaid or

default. In addition, given the large existing and anticipated supply of single-family homes in the market, we

anticipate that it will take years before our REO inventory is reduced to pre-2008 levels.

We show how we calculate our realized credit losses in “Table 15: Credit Loss Performance Metrics.” Our

reserves for credit losses described in this discussion consist of (1) our allowance for loan losses, (2) our

allowance for accrued interest receivable, (3) our allowance for preforeclosure property taxes and insurance

receivables, and (4) our reserve for guaranty losses (collectively, our “total loss reserves”), plus the portion of

fair value losses on loans purchased out of unconsolidated MBS trusts reflected in our consolidated balance

sheets that we estimate represents accelerated credit losses we expect to realize. For more information on our

reserves for credit losses, see “Table 11: Total Loss Reserves.”

The fair value losses that we consider part of our reserves are not included in our “total loss reserves.” We

recorded the majority of these fair value losses prior to our adoption in 2010 of accounting guidance on the

transfers of financial assets and the consolidation of variable interest entities. Before we adopted this guidance,

upon our acquisition of credit-impaired loans out of unconsolidated MBS trusts, we recorded fair value loss

charge-offs against our reserve for guaranty losses. The amount of these charge-offs was the amount by which

the acquisition cost of these loans exceeded their estimated fair value. We expect to realize a portion of these fair

value losses as credit losses in the future (for loans that eventually involve foreclosures, short sales or

deeds-in-lieu of foreclosure), yet these fair value losses have already reduced the mortgage loan balances

reflected in our consolidated balance sheets and have effectively been recognized in our consolidated statements

of operations and comprehensive loss through our provision for guaranty losses. We consider these fair value

losses as an “effective reserve,” apart from our total loss reserves, to the extent that we expect to realize these

amounts as credit losses on the acquired loans in the future.

-13-