Berkshire Hathaway 2011 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2011 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

|

|

Management’s Discussion (Continued)

Investment and Derivative Gains/Losses (Continued)

underlying equity and credit markets. We have not actively traded into and out of credit default and equity index put option contracts.

Under many of the contracts, no settlements will occur until the contract expiration dates, which may occur many years from now.

We recorded pre-tax losses of $251 million on our credit default contracts in 2011 and gains of $250 million in 2010 and

$789 million in 2009. Gains and losses generated by our credit default contracts reflect changes in the estimated values of the

contracts which reflect changes in credit default spreads relative to the remaining terms of the contracts. In 2011, the losses were

primarily related to our contracts involving non-investment grade corporate issuers, due to widening credit default spreads and

loss events. The gains in 2010 reflected the overall narrowing of credit default spreads for corporate issuers and were somewhat

offset by losses due to the widening of spreads for municipalities. The gains from our credit default contracts in 2009 derived

primarily from the narrowing of spreads for corporate issuers.

During the fourth quarter of 2011, two losses occurred under our contracts covering non-investment grade issuers and one

additional loss occurred in early 2012. Our risk of additional cash losses with respect to our non-investment grade issuers will

decline significantly in 2012 as a result of contract expirations. We paid $86 million to settle the two losses occurring in 2011.

No credit loss events occurred under our contracts in 2010. There were several credit loss events in the first half of 2009,

primarily related to contracts involving non-investment grade (or high-yield) corporate issuers and during 2009 we paid losses

of about $1.9 billion.

In 2011, we recorded pre-tax losses of approximately $1.8 billion on our equity index put option contracts. The losses

reflected declines ranging from about 5.5% to 17% with respect to three of the four equity indexes covered under our contracts

and lower interest rate inputs. In 2010 and 2009, gains on equity index put option contracts were $172 million and $2.7 billion,

respectively. In the fourth quarter of 2010, we settled certain equity index put option contracts early at the request of the

counterparty. The net gain in 2010 arising from these settled contracts was $561 million, which is represented by the difference

between the recorded fair values of the contracts at December 31, 2009 and the settlement payment amounts. Otherwise, we

recognized pre-tax losses of $389 million under our remaining equity index put option contracts reflecting generally lower

interest rate assumptions and the effect of foreign currency exchange rate changes. The derivative contract gains in 2009

reflected increases in the underlying equity indexes ranging from approximately 19% to 23%, partially offset by the impact of a

weaker U.S. Dollar on non-U.S. equity index put option contracts and lower interest rates. Our ultimate payment obligations, if

any, under our remaining equity index put option contracts will be determined as of the contract expiration dates, which begin in

2018, based on the intrinsic value as of those dates. Our recorded liability for these contracts was $8.5 billion as of

December 31, 2011.

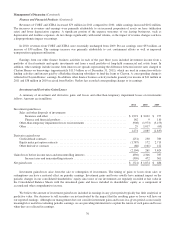

Financial Condition

Our balance sheet continues to reflect significant liquidity and a strong capital base. Our consolidated shareholders’ equity

at December 31, 2011 was $164.8 billion, an increase of approximately $7.5 billion from December 31, 2010. Consolidated

cash and investments of insurance and other businesses approximated $153.9 billion at December 31, 2011, including cash and

cash equivalents of $33.5 billion. These assets are held predominantly in our insurance businesses.

In February 2011, $2.0 billion of the parent company’s senior unsecured notes matured. In August 2011, we issued $2.0

billion of parent company senior unsecured notes. On January 31, 2012, we issued an additional $1.7 billion of parent company

senior unsecured notes, the proceeds of which were used to fund the repayment of $1.7 billion of notes maturing in February

2012. On September 16, 2011, we acquired all of the outstanding stock of The Lubrizol Corporation for cash consideration of

$135 per share or approximately $8.7 billion in the aggregate. We funded the acquisition price with existing cash balances. See

Note 2 to the Consolidated Financial Statements.

In late September 2011, our Board of Directors authorized Berkshire Hathaway to repurchase Class A and Class B shares

of Berkshire at prices no higher than a 10% premium over the book value of the shares. Berkshire may repurchase shares in

open market purchases or through privately negotiated transactions, at management’s discretion. The repurchase program is

expected to continue indefinitely and the amount of purchases will depend entirely upon the levels of cash available, the

attractiveness of investment and business opportunities either at hand or on the horizon and the degree of discount of the market

price to management’s estimate of intrinsic value. The repurchase program does not obligate Berkshire to repurchase any dollar

amount or number of Class A or Class B shares. Berkshire plans to use cash on hand to fund repurchases and repurchases will

not be made if they would reduce Berkshire’s consolidated cash equivalent holdings below $20 billion. Financial strength and

redundant liquidity will always be of paramount importance at Berkshire. To date, share repurchases have been insignificant.

78