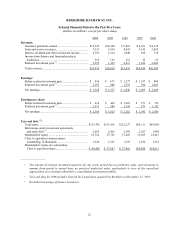

Berkshire Hathaway 2000 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2000 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

|

|

14

Now, speculation — in which the focus is not on what an asset will produce but rather on what the next

fellow will pay for it — is neither illegal, immoral nor un-American. But it is not a game in which Charlie and I

wish to play. We bring nothing to the party, so why should we expect to take anything home?

The line separating investment and speculation, which is never bright and clear, becomes blurred still

further when most market participants have recently enjoyed triumphs. Nothing sedates rationality like large doses

of effortless money. After a heady experience of that kind, normally sensible people drift into behavior akin to that

of Cinderella at the ball. They know that overstaying the festivities that is, continuing to speculate in companies

that have gigantic valuations relative to the cash they are likely to generate in the future will eventually bring on

pumpkins and mice. But they nevertheless hate to miss a single minute of what is one helluva party. Therefore, the

giddy participants all plan to leave just seconds before midnight. There’s a problem, though: They are dancing in

a room in which the clocks have no hands.

Last year, we commented on the exuberance and, yes, it was irrational that prevailed, noting that

investor expectations had grown to be several multiples of probable returns. One piece of evidence came from a

Paine Webber-Gallup survey of investors conducted in December 1999, in which the participants were asked their

opinion about the annual returns investors could expect to realize over the decade ahead. Their answers averaged

19%. That, for sure, was an irrational expectation: For American business as a whole, there couldn’t possibly be

enough birds in the 2009 bush to deliver such a return.

Far more irrational still were the huge valuations that market participants were then putting on businesses

almost certain to end up being of modest or no value. Yet investors, mesmerized by soaring stock prices and

ignoring all else, piled into these enterprises. It was as if some virus, racing wildly among investment professionals

as well as amateurs, induced hallucinations in which the values of stocks in certain sectors became decoupled from

the values of the businesses that underlay them.

This surreal scene was accompanied by much loose talk about “value creation.” We readily acknowledge

that there has been a huge amount of true value created in the past decade by new or young businesses, and that

there is much more to come. But value is destroyed, not created, by any business that loses money over its lifetime,

no matter how high its interim valuation may get.

What actually occurs in these cases is wealth transfer, often on a massive scale. By shamelessly

merchandising birdless bushes, promoters have in recent years moved billions of dollars from the pockets of the

public to their own purses (and to those of their friends and associates). The fact is that a bubble market has allowed

the creation of bubble companies, entities designed more with an eye to making money off investors rather than for

them. Too often, an IPO, not profits, was the primary goal of a company’s promoters. At bottom, the “business

model” for these companies has been the old-fashioned chain letter, for which many fee-hungry investment bankers

acted as eager postmen.

But a pin lies in wait for every bubble. And when the two eventually meet, a new wave of investors learns

some very old lessons: First, many in Wall Street a community in which quality control is not prized will sell

investors anything they will buy. Second, speculation is most dangerous when it looks easiest.

At Berkshire, we make no attempt to pick the few winners that will emerge from an ocean of unproven

enterprises. We’re not smart enough to do that, and we know it. Instead, we try to apply Aesop’s 2,600-year-old

equation to opportunities in which we have reasonable confidence as to how many birds are in the bush and when

they will emerge (a formulation that my grandsons would probably update to “A girl in a convertible is worth five

in the phonebook.”). Obviously, we can never precisely predict the timing of cash flows in and out of a business or

their exact amount. We try, therefore, to keep our estimates conservative and to focus on industries where business

surprises are unlikely to wreak havoc on owners. Even so, we make many mistakes: I’m the fellow, remember,

who thought he understood the future economics of trading stamps, textiles, shoes and second-tier department

stores.

Lately, the most promising “bushes” have been negotiated transactions for entire businesses, and that

pleases us. You should clearly understand, however, that these acquisitions will at best provide us only reasonable

returns. Really juicy results from negotiated deals can be anticipated only when capital markets are severely

constrained and the whole business world is pessimistic. We are 180 degrees from that point.