TomTom 2008 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2008 TomTom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

/ 55

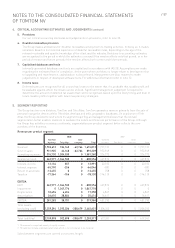

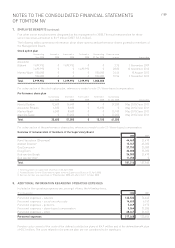

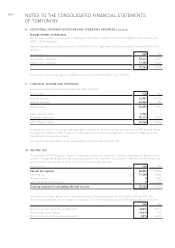

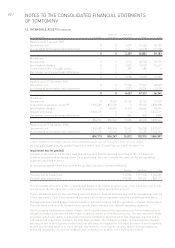

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

OF TOMTOM NV

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Financial assets (continued)

Financial assets at fair value through profit or loss

Financial assets at fair value through profit or loss are financial assets held for trading. A financial asset is

classified in this category if acquired principally for the purpose of selling in the short-term. Derivatives are

categorised within this category if their fair value is a positive number, otherwise the derivative is classified as a

financial liability.

Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not

quoted in an active market. They are included in current assets, except for maturities greater than 12 months

after the balance sheet date, which are classified as non-current assets. Loans and receivables are measured at

amortised cost using the effective interest method, less any impairment. The Group’s loans and receivables

comprise ‘trade receivables’ and ‘cash and cash equivalents’ in the balance sheet (note 16 and 19).

Fair value

The fair value of investments that are actively traded in organised financial markets is determined by reference to

quoted market bid prices at the close of business on the balance sheet date. For investments for which there is

no active market, fair value is determined using valuation techniques. Such techniques include recent arm’s

length transactions; reference to the current market value of another instrument which is substantially the same;

discounted cash flow analysis or other valuation models.

The Group holds an investment in Infotech, which has been included within the category financial assets

designated at fair value through profit and loss from the date of acquisition. Gains or losses on this investment

are recognised in the income statement.

For certain of the Group’s financial instruments, including trade receivables, trade payables and other accrued

liabilities, the carrying amounts approximate fair value due to their short maturities.

Inventories

Inventories are stated at the lower of cost and net realisable value. The cost of inventories comprises costs of

purchase, assembly and conversion to finished products. Borrowing costs are excluded. The cost of inventories is

recorded using the first-in first-out (FIFO) cost basis, net of reserves for obsolescence and any excess stock. Net

realisable value represents the estimated selling price less an estimate of the costs of completion and direct

selling costs.

Trade receivables

Trade receivables are initially recognised at fair value, and subsequently measured at amortised cost (if the time

value is material), using the effective interest method, less provision for impairment. A provision for impairment

of trade receivables is established when there is objective evidence that the Group will not be able to collect all

amounts due, according to the original terms of the receivables. Significant financial difficulties of the debtor,

probability that the debtor will enter bankruptcy or financial reorganisation, and default or delinquency in

payments (more than 30 days overdue) are considered indicators that the trade receivable is impaired. The

amount of the provision is the difference between the asset’s carrying amount and the present value of estimated

future cash flows, discounted at the original effective interest rate. The carrying amount of the asset is reduced

through the use of an allowance account and the amount of the loss is recognised in the income statement within

‘cost of sales’. When a trade receivable is uncollectable, it is written off against the allowance account for trade

receivables. Subsequent recoveries of amounts previously written off are credited against ‘cost of sales’ in the

income statement.

Cash and cash equivalents

Cash and cash equivalents are stated at face value and comprise cash on hand, deposits held on call with banks,

and other short-term highly liquid investments that are readily convertible to a known amount of cash and are

subject to an insignificant risk of changes in value.

Financial liabilities and equity instruments

Financial liabilities and equity instruments issued by the Group are classified according to the substance of the

contractual arrangements entered into, and the definitions of a financial liability and an equity instrument. An

equity instrument is any contract that evidences a residual interest in the assets of the Group after deducting all

of its liabilities. Equity instruments are recorded at the proceeds received, net of direct issue costs.