Motorola 2000 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2000 Motorola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36

|

|

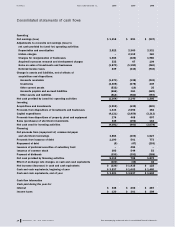

26 MOTOROLA, INC. AND SUBSIDIARIES

Advertising and sales promotion costs: Advertising and sales promotion costs are expensed as

incurred and are included in selling, general and administrative expenses in the consolidated state-

ments of operations.

Inventories: Inventories are valued at the lower of average cost (which approximates computation on a

first-in, first-out basis) or market (net realizable value or replacement cost).

Property, plant and equipment: Property, plant and equipment are stated at cost less accumulated

depreciation. Depreciation is recorded principally using the declining-balance method, based on

the estimated useful lives of the assets (buildings and building equipment, 5-40 years; machinery

and equipment, 2-12 years).

Intangible assets: Goodwill and other intangible assets are recorded at cost and amortized primarily

on a straight-line basis over periods ranging from 3 to 40 years.

Investments: Investments include available for sale securities at fair value and investments under the

cost and equity methods of accounting. For the available for sale securities, any unrealized holding gains

and losses, net of deferred taxes, are excluded from operating results and are recognized as a sepa-

rate component of stockholders’ equity until realized. The fair values of the securities are determined

based on prevailing market prices.

Long-lived assets: Long-lived assets held and used by the Company and intangible assets are reviewed

for impairment whenever events or changes in circumstances indicate that the carrying amount of

assets may not be recoverable. The Company evaluates recoverability of assets to be held and used

by comparing the carrying amount of an asset to future net undiscounted cash flows to be generated

by the asset. If such assets are considered to be impaired, the impairment to be recognized is meas-

ured by the amount by which the carrying amount of the assets exceeds the fair value of the assets

calculated using a discounted future cash flows analysis. Assets to be disposed of are reported at

the lower of the carrying amount or fair value less costs to sell.

Fair values of financial instruments: The fair values of financial instruments are determined based on

quoted market prices and market interest rates as of the end of the reporting period.

Foreign currency translation: Many of the Company’s non-U.S. operations use the respective local

currencies as the functional currency. Those non-U.S. operations which do not use the local curren-

cies use the U.S. dollar as the functional currency. The effects of translating the financial position and

results of operations of local currency functional operations into U.S. dollars are included in a sepa-

rate component of stockholders’ equity.

Foreign currency transactions: The effects of remeasuring the non-functional currency assets or liabil-

ities into the functional currency as well as gains and losses on hedges of existing assets or liabilities

are marked-to-market, and the result is recorded within selling, general and administrative expenses in

the consolidated statements of operations. Gains and losses on financial instruments that hedge firm

future commitments are deferred until such time as the underlying transactions are recognized or

Condensed notes to consolidated financial statements