Motorola 2000 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2000 Motorola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36

|

|

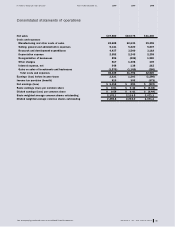

MOTOROLA, INC. AND SUBSIDIARIES 25

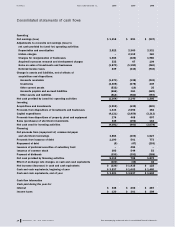

Condensed notes to consolidated financial statements

Basis of presentation and summary of significant accounting policies

Basis of presentation: On January 5, 2000, Motorola, Inc. (“Motorola”) completed its previously

announced merger with General Instrument Corporation (“General Instrument”) by exchanging 301 mil-

lion shares (reflecting adjustment for the 3-for-1 common stock split described below) of its common

stock for all of the common stock of General Instrument. Each share of General Instrument was

exchanged for 1.725 shares (reflecting adjustment for the 3-for-1 common stock split described

below) of Motorola’s common stock. Motorola has accounted for the merger as a pooling-of-interests,

and accordingly, all prior period consolidated financial statements have been restated to include

the results of operations, financial position and cash flows of General Instrument. The effects of

conforming General Instrument’s accounting policies to those of Motorola were not material.

For the year ended December 31, 1999, net sales for Motorola and General Instrument were

$30.9 billion and $2.2 billion, respectively. Net earnings for Motorola and General Instrument were

$817 million and $74 million, respectively. For the year ended December 31, 1998, net sales for

Motorola and General Instrument were $29.4 billion and $2.0 billion, respectively. The net loss for

Motorola was $962 million, and the net earnings for General Instrument were $55 million. Results

of operations for the year ended December 31, 2000 reflect the pooling-of-interests. Subsequent

references to “Motorola, Inc.” and “the Company” reflect the pooling-of-interests.

On June 1, 2000, the Company completed a 3-for-1 common stock split in the form of a 200% stock

dividend. On that date, the Company distributed 1.4 billion common shares to stockholders of record

on May 15, 2000. The par value of the common stock remained at $3 per share. The effect of the

stock split has been recognized retroactively in the stockholders’ equity accounts as of January 1,

1998, and in all share and per share data in the consolidated financial statements and the condensed

notes to the consolidated financial statements. The stockholders’ equity accounts have been restated

to reflect the reclassification of an amount equal to the par value of the increase in issued common

shares from additional paid-in capital and retained earnings to common stock.

Principles of consolidation: The consolidated financial statements include the accounts of the

Company and all majority-owned subsidiaries in which it has control. The Company’s investments in

non-controlled entities in which it has the ability to exercise significant influence over operating and

financial policies are accounted for by the equity method. The Company’s investments in other entities

are carried at their historical cost. Certain of these cost-based investments are marked-to-market at

the balance sheet date to reflect their fair value with the unrealized gains and losses, net of tax,

included in a separate component of stockholders’ equity.

Cash equivalents: The Company considers all highly liquid investments purchased with an original

maturity of three months or less to be cash equivalents.

Revenue recognition: The Company recognizes revenue at the time of shipment, and accruals are

established for price protection, returns and cooperative marketing programs with distributors. For

long-term contracts, the Company uses the percentage-of-completion method to recognize revenues and

costs. For contracts involving new technologies, revenues and profits or parts thereof are deferred until

technological feasibility is established, customer acceptance is obtained and other contract-specific

terms have been completed. In the fourth quarter of 2000, the Company adopted Staff Accounting

Bulletin Number 101, “Revenue Recognition in Financial Statements” (SAB 101). The Company’s

adoption of SAB 101 did not have a significant impact on its consolidated financial position or

results of operations.

1