Kodak 2011 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2011 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

-

565

-

566

-

567

-

568

-

569

-

570

-

571

-

572

-

573

-

574

-

575

-

576

-

577

-

578

-

579

-

580

-

581

|

|

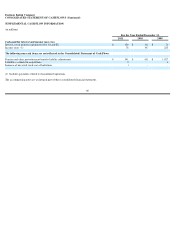

Eastman Kodak Company

NOTES TO FINANCIAL STATEMENTS

NOTE 1: CHAPTER 11 FILING

On January 19, 2012 (the “Petition Date”), Eastman Kodak Company (the “Company”) and its U.S. subsidiaries (together with the Company, the

“Debtors”) filed voluntary petitions for relief (the “Bankruptcy Filing”) under chapter 11 of the United States Bankruptcy Code (the “Bankruptcy

Code”) in the United States Bankruptcy Court for the Southern District of New York (the “Bankruptcy Court”) case number 12-10202. The

Company’s foreign subsidiaries (collectively, the “Non-Filing Entities”) were not part of the Bankruptcy Filing. The Debtors will continue to operate

their businesses as “debtors-in-possession” under the jurisdiction of the Bankruptcy Court and in accordance with the applicable provisions of the

Bankruptcy Code and the orders of the Bankruptcy Court. The Non-Filing Entities will continue to operate in the ordinary course of business.

The Bankruptcy Filing is intended to permit the Company to reorganize and increase liquidity in the U.S. and abroad, monetize non-strategic

intellectual property, fairly resolve legacy liabilities, and focus on the most valuable business lines to enable sustainable profitability. The Company’s

goal is to develop and implement a reorganization plan that meets the standards for confirmation under the Bankruptcy Code. Confirmation of a

reorganization plan could materially alter the classifications and amounts reported in the Company’s consolidated financial statements, which do not

give effect to any adjustments to the carrying values of assets or amounts of liabilities that might be necessary as a consequence of a confirmation of a

reorganization plan or other arrangement or the effect of any operational changes that may be implemented.

Operation and Implication of the Bankruptcy Filing

Under Section 362 of the Bankruptcy Code, the filing of voluntary bankruptcy petitions by the Debtors automatically stayed most actions against the

Debtors, including most actions to collect indebtedness incurred prior to the Petition Date or to exercise control over the Company’

s property. Accordingly,

although the Bankruptcy Filing triggered defaults for certain of the Debtor’

s debt obligations, creditors are stayed from taking any actions as a result of such

defaults. Absent an order of the Bankruptcy Court, substantially all of the Company’s pre-

petition liabilities are subject to settlement under a reorganization

plan. As a result of the Bankruptcy Filing the realization of assets and the satisfaction of liabilities are subject to uncertainty. The Debtors, operating as

debtors-in-possession under the Bankruptcy Code, may, subject to approval of the Bankruptcy Court, sell or otherwise dispose of assets and liquidate or

settle liabilities for amounts other than those reflected in the consolidated financial statements. Further, a confirmed reorganization plan or other

arrangement may materially change the amounts and classifications in the Company’s consolidated financial statements.

Subsequent to the Petition Date, the Company received approval from the Bankruptcy Court to pay or otherwise honor certain pre-petition obligations

generally designed to stabilize the Company’s operations. These obligations related to certain employee wages, salaries and benefits, and the payment of

vendors and other providers in the ordinary course for goods and services received after the Petition Date. The Company has retained, pursuant to

Bankruptcy Court approval, legal and financial professionals to advise the Company in connection with the Bankruptcy Filing and certain other

professionals to provide services and advice in the ordinary course of business. From time to time, the Company may seek Bankruptcy Court approval to

retain additional professionals.

The U.S. Trustee for the Southern District of New York (the “U.S. Trustee”) has appointed an official committee of unsecured creditors (the “UCC”). The

UCC and its legal representatives have a right to be heard on all matters that come before the Bankruptcy Court on all matters affecting the Debtors. There

can be no assurance that the UCC will support the Company’s positions on matters to be presented to the Bankruptcy Court in the future or on any

reorganization plan, once proposed.

Reorganization Plan

In order for the Company to emerge successfully from chapter 11, the Company must obtain the Bankruptcy Court’s approval of a reorganization plan,

which will enable the Company to transition from chapter 11 into ordinary course operations outside of bankruptcy. In connection with a reorganization

plan, the Company also may require a new credit facility, or “exit financing.” The Company’

s ability to obtain such approval and financing will depend on,

among other things, the timing and outcome of various ongoing matters related to the Bankruptcy Filing. A reorganization plan determines the rights and

satisfaction of claims of various creditors and security holders, and is subject to the ultimate outcome of negotiations and Bankruptcy Court decisions

ongoing through the date on which the reorganization plan is confirmed.

Although the Company’s goal is to file a plan of reorganization, the Company may determine that it is in the best interests of the Debtors’ estates to seek

Bankruptcy Court approval of a sale of all or a portion of the Company’s assets pursuant to Section 363 of the Bankruptcy Code or seek confirmation of a

reorganization plan providing for such a sale or other arrangement.

61