Barclays 2014 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2014 Barclays annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

|

|

barclays.com/annualreport Barclays PLC Annual Report 2014 I 05

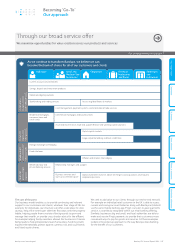

Our approach

Operating environment and approach to risk

Barclays is a global financial services provider operating in

50 countries, with home markets in the UK, US and South

Africa, governed by global and local regulatory standards.

Our environment continues to change. Central banks have launched

unprecedented monetary policies such as Quantitative Easing and near-

zero interest rates to stimulate growth. Further regulatory change,

such as structural reform in the UK and US will require banks to segregate

activities in order to create a safer banking environment and increase focus

on capital, liquidity and funding. Conduct issues have hurt Barclays –

and the banking industry – causing loss of trust amongst stakeholders.

Rebuilding trust is vital, enabling us to meet and exceed the growing

needs of customers and clients. The power of technology has raised

customer and client expectations, but also reduced the cost-to-serve

through automation, process improvement and innovation while

making customer experiences faster, more personalised and lower risk.

Without active risk management to address these external factors, our

long-term goals could be adversely impacted. See page 09 to see how

the strategy adapted in 2014.

The Barclays risk management framework, organised by our Principal

Risks, sets out the activities, tools, techniques and arrangements we

can employ to better identify, monitor and manage actual and potential

risks facing the Bank. Risk appetite is set and verified at an appropriate

level and procedures established to protect Barclays and prevent

detriment to its customers, colleagues and communities. Barclays

also manages human rights risk via our environmental and social risk

procedures and guidance and reputational risk framework, and

integrates human rights issues into business decision-making.

Our Principal Risks

Credit Risk: Financial loss should customers not fulfil contractual

obligations to the Group.

Market Risk: Earnings or capital impact due to volatility of trading

book positions or inability to hedge the banking book balance sheet.

Funding Risk: Failure to maintain capital ratios and liquidity

obligations leading to inability to support normal business activity

and meet liquidity regulatory requirements.

Operational Risk: Losses or costs resulting from human factors,

inadequate internal processes and systems or external events.

Conduct Risk: Detriment caused to our customers, clients,

counterparties, or the Bank and its employees through inappropriate

judgement in execution of business activities.

Reputation Risk: Damage to Barclays brand arising from any

association, action or inaction perceived by stakeholders as

inappropriate or unethical. From the 1st January 2015, Reputation

Risk will be combined with Conduct Risk.

For further information on how we

assess and monitor risks, please see

the Risk review on page 113

Becoming ‘Go-To’

Regulatory change

Regulatory focus has shifted, affecting the sustainability and

profitability of products, businesses and the structural formation

of banks. The impact of regulatory change is a permanent shift.

Trust and conduct

We continue to work to put our legacy issues behind us.

The cost of legacy conduct issues has negative repercussions

but the changes we are making in response to them will have

a positive effect in the long-term.

Technology and rising expectations

Technological improvements enhance the experience of

customers and clients and can reduce costs. The investment

required can be expensive in the short-term but will generate

long-term rewards.

A proactive

approach

We continually take action to achieve our

goal and deliver value to our shareholders

For more information,

please see page 09

Economic environment

Global economic growth is expected to be subdued for

a prolonged period. This makes income growth more

challenging for banks.

In this operating environment

We continue to be proactive in adapting to the external environment

Our approach to value creation is consistent

The Strategic Report Governance Risk review Financial review Financial statements Shareholder information