US Bank 2010 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2010 US Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

|

|

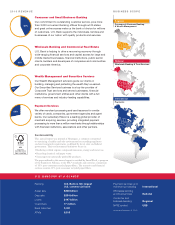

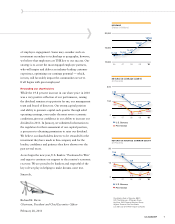

U.S. BANCORP 5

Richard K. Davis

Chairman, President and

Chief Executive Officer

diversified business model, recent investments, deeper

customer relationships and overall financial strength.

Continued challenges

Despite these positive results, U.S. Bancorp and the industry

still face challenges in loan demand which, though showing

some welcome signs of recovery, remains muted. Credit-

worthy businesses are applying for credit lines, but many are

not actively utilizing them. Commercial utilization levels

are at historic lows, and only a continuing and robust

recovery will allow that to change.

Capital and liquidity positions

We continued to generate significant capital in 2010, ending

the year with a Tier 1 common equity ratio of 7.8 percent

and a Tier 1 capital ratio of 10.5 percent, both measures

significantly higher than the regulatory levels required to be

considered “well-capitalized.” Our ability to generate capital

each and every quarter, and the significant growth we have

experienced in deposits over the past few years have provided

us with the capacity to fund and grow our balance sheet.

Further, the strength of our capital and liquidity has been

recognized by the rating agencies, as our debt ratings continue

to place us among the highest-rated banks in the country.

Our role in the recovery

The financial services industry is no longer in a crisis

situation; many banks are doing well, and the economy is

slowly recovering. As one of America’s strongest banks,

we are proud to be an industry leader, providing guidance

on public messaging and communicating on behalf of our

industry with regulators and legislators.

It is now time for America’s banking industry to be heard.

A healthy and vibrant banking industry is essential to drive

the economy forward and help our country recover from

this recession. When the intensity of the economic downturn

became clear several years ago, and as some financial compa-

nies’ role in the downturn became known, the entire industry

lost a great deal of respect and its reputation suffered. This

proved to be harmful to all banks, customers, shareholders

and communities. It is now clear that strong banks, including

U.S. Bancorp, are critically important to the recovery and must

have a voice in the direction of industry regulation. U.S. Bancorp

will continue to work with the administration, legislators,

the regulators — and our peer banks — to make it clear to

all that the banking industry holds the key to accelerating the

economic recovery. Importantly, however, we must continue

to highlight the consequences of excessive regulation that

could be injurious, rather than supportive, of a full recovery.