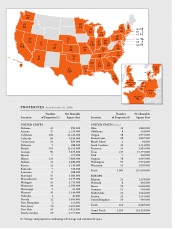

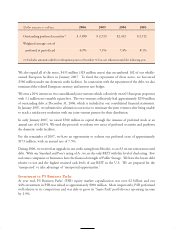

Public Storage 2006 Annual Report Download - page 5

Download and view the complete annual report

Please find page 5 of the 2006 Public Storage annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

I

ntrinsic Val

ue

In un

d

erta

k

ing an

d

structuring a merger, it is as important to un

d

erstan

d

w

h

at you are

b

uying as w

h

a

t

y

ou are

g

ivin

g

up. In t

h

e case o

f

an a

ll

cas

h

transaction, it is easy to un

d

erstan

d

w

h

at you are payin

g

. But

in the case of a stock mer

g

er, such as with Shur

g

ard, we in effect “sold” part of our company, about 23%,

to the Shur

g

ard shareholders in return for 100% of their company and the assumption of debt.

A

ccordingly, we needed to understand our intrinsic or enterprise value and make some assessments of

Sh

urgar

d

’s intrinsic va

l

ue. T

h

is is exact

l

y w

h

at we

d

i

d

.

To un

d

erstan

d

intrinsic va

l

ue, t

h

ere is no

b

etter source t

h

an Warren Bu

ff

ett. His

d

e

f

inition goes

s

omet

h

in

g

l

i

k

e t

h

is:

“Intrinsic va

l

ue is t

h

e

d

iscounte

d

va

l

ue o

f

t

h

e cas

h

t

h

at can

b

e ta

k

en out o

f

a

b

usiness

d

urin

g

its

l

i

f

etime

.

C

a

l

cu

l

atin

g

intrinsic va

l

ue is typica

ll

y

h

i

ghl

y su

bj

ective t

h

at varies

b

ot

h

as estimates o

f

f

uture cas

h

fl

ow

s

a

re revise

d

an

d

as interest rates move. Intrinsic va

l

ue is t

h

e on

l

y

l

o

g

ica

l

way to eva

l

uate t

h

e re

l

ativ

e

a

ttractiveness o

f

investments an

d

b

usinesses. Un

d

erstan

d

in

g

intrinsic va

l

ue is as important

f

or mana

g

er

s

a

s it is

f

or owners. W

h

en mana

g

ers ma

k

e capita

l

a

ll

ocation

d

ecisions, suc

h

as a mer

g

er or acquisition, it

is vita

l

t

h

at

d

ecisions are ma

d

e to increase intrinsic va

l

ue rat

h

er t

h

an

d

estroy it. Many mana

g

ers ten

d

t

o

f

ocus on w

h

et

h

er a transaction is imme

d

iate

l

y

d

i

l

utive or anti-

d

i

l

utive to earnin

g

s per s

h

are rat

h

er t

h

a

n

e

va

l

uate its impact on intrinsic va

l

ue. Over time, t

h

e s

k

i

ll

wit

h

w

h

ic

h

mana

g

ers a

ll

ocate capita

l

wi

ll

h

av

e

a

n enormous im

p

act on a com

p

any’s intrinsic va

l

ue.

”

In assessin

g

a mer

g

er wit

h

S

h

ur

g

ar

d

, we eva

l

uate

d

t

h

e cas

h

fl

ows o

f

b

ot

h

b

usinesses. Here is a snaps

h

ot

of

b

ot

h

companies at t

h

e en

d

o

f

2005 usin

g

Fun

d

s

f

rom Operation (see

b

e

l

ow

f

or exp

l

anation):

Comparison o

f

FFO per Common S

h

are in 200

5

(

Amounts in mi

ll

ions, exce

p

t

p

er s

h

are)

Sh

urgar

d

Pu

bl

ic Storag

e

SHU reported FFO $ 68 PSA reported FFO $ 46

5

Merger costs 14 Hurricane casualty losses 3

Real estate development costs 13 Gain on sale of non-real estate assets (1)

G&A costs 35 EITF D-42 c

h

arges

9

E

uro

p

ean

l

osses 1

8

FFO after ad

j

ustments $ 148 FFO after ad

j

ustments $ 47

6

S

h

ares issue

d

39 S

h

ares outstan

d

in

g

129

FFO per share after adjustments

$

3.79 FFO per share after adjustments

$

3.6

9

S

o ad

j

ustin

g

for special char

g

es, one time items or costs that we did not think would be recurrin

g

, the

transaction was immediately FFO positive for Public Stora

g

e shareholders. However, we would not have

pursued the merger for a few cents of earnings accretion. The real value lies in the opportunity to achiev

e

l

ower costs an

d

h

ig

h

er revenues in S

h

urgar

d

’s

d

omestic an

d

European properties an

d

l

ower t

h

e operating

costs o

f

Pu

bl

ic Storage’s

d

omestic port

f

o

l

io (t

h

roug

h

economies o

f

sca

l

e).