NVIDIA 2014 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2014 NVIDIA annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

Table of Contents

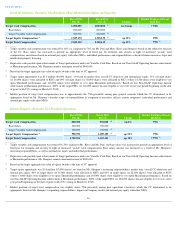

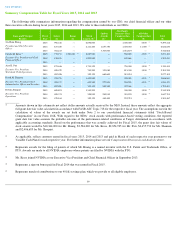

Additional Executive Compensation Practices, Policies and Procedures

Compensation Recovery Policy

In April 2009, our Board adopted a Compensation Recovery Policy which covers all of our employees. Under this policy, if we are required

to prepare an accounting restatement to correct an accounting error on an interim or annual financial statement included in a report on Form 10-

Q or Form 10-

K due to material noncompliance with any financial reporting requirement under the federal securities laws, or a Restatement, and

if the Board or a committee of independent directors concludes that our CEO, CFO or any other officer or employee received a variable

compensation payment that would not have been payable if the original interim or annual financial statements reflected the Restatement, then

under the Compensation Recovery Policy:

We will review and update the Compensation Recovery Policy as necessary for compliance with the clawback policy provisions of the

Dodd-Frank Wall Street Reform and Consumer Protection Act when the final regulations related to that policy are issued.

Tax and Accounting Implications

Section 162(m) of the Internal Revenue Code limits the amount that we may deduct from our federal income taxes for remuneration paid to

our CEO and three most highly compensated executive officers (other than our CFO) to $1 million per person covered per year, unless certain

requirements are met. Section 162(m) of the Internal Revenue Code provides an exception from this deduction limitation for certain forms of

“performance-based compensation”. While our CC is mindful of the benefit to NVIDIA’

s performance of full deductibility of compensation, our

CC believes that it should not be constrained by the requirements of Section 162(m) of the Internal Revenue Code where those requirements

would impair flexibility in compensating our NEOs in a manner that can best promote our corporate objectives. Therefore, our CC has not

adopted a policy that requires that all compensation be deductible and approval of compensation, including the grant of “performance-

based

compensation”

to our NEOs, by our CC is not a guarantee of deductibility under the Internal Revenue Code. Our CC intends to continue to

compensate our NEOs in a manner consistent with the best interests of NVIDIA and our stockholders.

Our CC also considers the impact of Section 409A of the Internal Revenue Code, and in general, our executive plans and programs are

designed to comply with the requirements of that section so as to avoid the possible adverse tax consequences that may arise from non-

compliance.

37

• Our CEO and CFO will be required to disgorge the net after-

tax amount of that portion of the variable compensation payment that

would not have been payable if the original interim or annual financial statements reflected the Restatement; and

•

The Board or the committee of independent directors may require any other officer or employee to repay all (or a portion of) the

variable compensation payment that would not have been payable if the original interim or annual financial statements reflected the

Restatement, as determined by the Board or such committee in its sole discretion. In using its discretion, the Board or the independent

committee may consider whether such person was involved in the preparation of our financial statements or otherwise caused the need

for the Restatement and may, to the extent permitted by applicable law, recoup amounts by (1) requiring partial or full repayment by

such person of any variable or incentive compensation or any gains realized on the exercise of stock options or on the open-

market sale

of vested shares, (2) canceling (in full or in part) any outstanding equity awards held by such person and/or (3) adjusting the future

compensation of such person.