Huntington National Bank 2010 Annual Report Download

Download and view the complete annual report

Please find the complete 2010 Huntington National Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

|

|

WELCOME.

2010 ANNUAL REPORT

Table of contents

-

Page 1

2010 ANNUAL REPORT WELCOME. -

Page 2

... bank holding company headquartered in Columbus, Ohio. Founded in 1866, it provides full-service commercial, small business, and consumer banking services; mortgage banking services; treasury management and foreign exchange services; equipment leasing; wealth and investment management services... -

Page 3

...our Midwest franchise." We did. Our agreement with Giant Eagle to open over 100 in-store banking offices will eventually result in Huntington being the most convenient bank in Ohio by having the most branches of any bank. • "We are getting stronger every day." We did. We consistently grew revenues... -

Page 4

...the growth was centered in lower-cost demand deposits and money market accounts. Without many opportunities to profitably grow loans, $2.9 billion of our deposit growth funded an increase average total investment securities. We, obviously, would rather use these funds to make higher-return loans, so... -

Page 5

... executing to this philosophy, coupled with increased convenience and superior service, positions Huntington as the most customer-attractive bank in our markets. While we will make less on some customer checking accounts in the short-term, the objective is the acceleration of growth of new customers... -

Page 6

... until the next business day to correct an overdraft balance in their account and avoid an overdraft fee. Customers are responding very positively, with this contributing to our higher than expected growth in consumer households. In 2009, service charge on deposit accounts represented 12% of... -

Page 7

... and industrial, as well as small business loans. Commercial real estate loans are expected to continue to decline, though at a slower rate. Home equity and residential mortgages are likely to show only modest growth. Core deposits are expected to show continued growth. Fee income is expected to be... -

Page 8

... of small business loans, a 27% increase. The Small Business Administration ranked Huntington as the 5th largest SBA lender in the country for their fiscal year ending September 30, 2010. In our markets we are the top SBA lender. • $100 Million Ohio Affordable Housing Commitment - In July 2010, we... -

Page 9

... financial services executives in the United States. Huntington is already benefitting enormously from his insights and advice. Each of the last two years represented major milestones in positioning Huntington for long-term growth. In 2009, we aggressively addressed our credit issues. Making... -

Page 10

..." and the "Additional Disclosure" sections in Huntington's Form 10-K for the year ending December 31, 2010, for a listing of risk factors. All forwardlooking statements speak only as of the date they are made and are based on information available at that time. We assume no obligation to update... -

Page 11

... File Number 1-34073 Huntington Bancshares Incorporated (Exact name of registrant as specified in its charter) Maryland (State or other jurisdiction of incorporation or organization) 31-0724920 (I.R.S. Employer Identification No.) 41 S. High Street, Columbus, Ohio (Address of principal executive... -

Page 12

...Item 5. Market for Registrant's Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities ...Item 6. Selected Financial Data ...Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations ...Introduction ...Executive Overview ...Discussion... -

Page 13

...HASP HCER Act IPO Asset Based Lending Allowance for Credit Losses Automobile Finance and Commercial Real Estate Asset-Liability Management Committee Allowance for Loan and Lease Losses Adjustable Rate Mortgage American Recovery and Reinvestment Act of 2009 Accounting Standards Codification Automated... -

Page 14

... Service London Interbank Offered Rate Loan to Value Management's Discussion and Analysis of Financial Condition and Results of Operations Market Risk Committee Mortgage Servicing Rights Nonaccrual Loans Net Asset Value Net Charge-off Nonperforming Assets Nonsufficient Funds and Overdraft Office... -

Page 15

... services to consumer and small business customers located within our primary banking markets consisting of five areas covering the six states of Ohio, Michigan, Pennsylvania, Indiana, West Virginia, and Kentucky. Its products include individual and small business checking accounts, savings accounts... -

Page 16

... a team of relationship managers providing public finance, brokerage, trust, lending, and treasury management services. A Treasury / Other function includes our insurance brokerage business, which specializes in commercial property/casualty, employee benefits, personal lines, life and disability and... -

Page 17

... banking philosophy, such as our 24-Hour Gracetm account feature introduced in 2010, which gives customers an additional business day to cover overdrafts to their consumer account without being charged overdraft fees. The table below shows our competitive ranking and market share based on deposits... -

Page 18

... to the Bank Holding Company Act. We are required to file reports and other information regarding our business operations and the business operations of our subsidiaries with the Federal Reserve. Because we are a public company, we are also subject to regulation by the SEC. The SEC has established... -

Page 19

...of funds by a subsidiary bank or its subsidiaries to its parent corporation or any nonbank subsidiary of its parent corporation, whether in the form of loans, extensions of credit, investments, or asset purchases, or otherwise undertaking certain obligations on behalf of such affiliates. Furthermore... -

Page 20

... bank holding companies. Under the guidelines and related policies, bank holding companies must maintain capital sufficient to meet both a risk-based asset ratio test and a leverage ratio test on a consolidated basis. The risk-based ratio is determined by allocating assets and specified off-balance... -

Page 21

... and limited-life preferred stock, mandatory convertible securities, qualifying subordinated debt, and the allowance for credit losses, up to 1.25% of risk-weighted assets. • Total Capital is Tier 1 plus Tier 2 capital. The Federal Reserve and the other federal banking regulators require that all... -

Page 22

...requirements and restrictions, including orders to sell sufficient voting stock to become Adequately-capitalized, requirements to reduce total assets, cessation of receipt of deposits from correspondent banks, and restrictions on making any payment of principal or interest on their subordinated debt... -

Page 23

... issued policy statements that provide that insured banks and bank holding companies should generally only pay dividends out of current operating earnings. The amount and timing of payments for FDIC Deposit Insurance are changing. In late 2008, under the assessment regime that was applicable prior... -

Page 24

...expect the 2011 FDIC assessment impact on our Consolidated Financial Statements to be materially higher than the prior period. As a financial holding company, we are subject to additional regulations. In order to maintain its status as a financial holding company, a bank holding company's depository... -

Page 25

... Credit Reporting Act. The Sarbanes-Oxley Act of 2002 imposed new or revised corporate governance, accounting, and reporting requirements on us and all other companies having securities registered with the SEC. In addition to a requirement that chief executive officers and chief financial officers... -

Page 26

..., establish controls, perform self-testing, and oversee the quarterly self-assessment process. Segment risk officers report directly to the related segment manager with a dotted line to the Chief Risk Officer. Corporate Risk Management establishes policies, sets operating limits, reviews new or... -

Page 27

... 31, 2010, represents Management's estimate of probable losses inherent in our loan and lease portfolio as well as our unfunded loan commitments and letters of credit. We periodically review our ACL for adequacy. In doing so, we consider economic conditions and trends, collateral values, and credit... -

Page 28

... achieved on the sale of foreclosed properties. Continued decline in home values may escalate these problems resulting in higher delinquencies, greater charge-offs, and increased losses on the sale of foreclosed real estate in future periods. Market Risks: 1. Changes in interest rates could reduce... -

Page 29

... earnings over the life of the instrument and reduces Tier I and Total Risk-based Capital regulatory ratios. Somewhat offsetting these negative impacts to OCI in a rising interest rate environment, is a decrease in pension and other post-retirement obligations. If short-term interest rates remain at... -

Page 30

... agreements, noncore deposits, and medium- and long-term debt, which includes a domestic bank note program and a Euronote program. The Bank is also a member of the FHLB, which provides funding through advances to members that are collateralized with mortgage-related assets. We maintain a portfolio... -

Page 31

...in retaining existing customer relationships or achieving anticipated operating efficiencies. 3. We are subject to routine on-going tax examinations by the IRS and by various other jurisdictions, including the states of Ohio, Kentucky, Indiana, Michigan, Pennsylvania, West Virginia and Illinois. The... -

Page 32

...file income tax returns with the IRS and various state, city, and foreign jurisdictions. Federal income tax audits have been completed through 2007. In addition, various state and other jurisdictions remain open to examination, including Ohio, Kentucky, Indiana, Michigan, Pennsylvania, West Virginia... -

Page 33

... Act represents a comprehensive overhaul of the financial services industry within the United States, establishes the new federal CFPB, and requires the bureau and other federal agencies to implement many new and significant rules and regulations. At this time, it is difficult to predict the extent... -

Page 34

..., as well as the Bank's, are located in the Huntington Center, a thirty-seven-story office building located in Columbus, Ohio. Of the building's total office space available, we lease approximately 33%. The lease term expires in 2030, with six five-year renewal options for up to 30 years but... -

Page 35

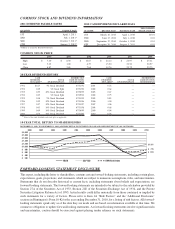

... December 31, 2010. The KBW Bank Index is a market capitalizationweighted bank stock index published by Keefe, Bruyette & Woods. The index is composed of the largest banking companies and includes all money center banks and regional banks, including Huntington. An investment of $100 on December 31... -

Page 36

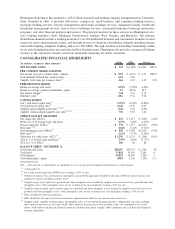

...19 Cash dividends declared per common share ...0.0400 Balance sheet highlights Total assets (period end) ...$53,819,642 Total long-term debt (period end)(2) ...3,813,827 Total shareholders' equity (period end) ...4,980,542 Average long-term debt(2) ...3,953,177 Average shareholders' equity ...5,482... -

Page 37

...end)(6),(8) ...Tangible equity to tangible assets (period end)(7),(8) ...Tier 1 leverage ratio (period end) ...Tier 1 risk-based capital ratio (period end) ...Total risk-based capital ratio (period end) ...Other data Full-time equivalent employees (period end) ...Domestic banking offices (period end... -

Page 38

..., automobile financing, equipment leasing, investment management, trust services, brokerage services, customized insurance service programs, and other financial products and services. Our over 600 banking offices are located in Indiana, Kentucky, Michigan, Ohio, Pennsylvania, and West Virginia... -

Page 39

... a result of an increase in mortgage banking income, reflecting an increase in origination and secondary marketing income as loan originations and loan sales were substantially higher, and MSR hedging. This was partially offset by a decline in service charges on deposit accounts, which was due to... -

Page 40

... Ohio banks, based on current data. In-store branches have a strong record for checking account acquisition and are expected to increase the number of households served and drive revenue. Additionally, it will give customers the convenience of operating seven days per week and extended hours banking... -

Page 41

... an amendment to Regulation E relating to certain overdraft fees for consumer deposit accounts and the passage of the Dodd-Frank Act. Effective July 1, 2010, the Federal Reserve Board amended Regulation E to prohibit charging overdraft fees for ATM or point-of-sale debit card transactions that... -

Page 42

... our 24-Hour GraceTM service to accelerate acquisition of new checking customers, while improving retention of existing customers. The recently passed Dodd-Frank Act is complex and we continue to assess how this legislation and subsequent rule-making will affect us. As hundreds of regulations are... -

Page 43

... C&I loans. Home equity and residential mortgages are likely to show only modest growth. CRE loans are expected to continue to decline, but at a slower rate. Core deposits are expected to show continued growth. Further, we expect the shift toward lower-cost demand deposit accounts will continue. Fee... -

Page 44

... interest income after provision for credit losses ...Service charges on deposit accounts Mortgage banking income ...Trust services ...Electronic banking...Insurance income ...Brokerage income ...Bank owned life insurance income . Automobile operating lease income . Securities losses ...Other income... -

Page 45

... have been higher than basic earnings per common share (anti-dilutive) for the year. (3) On a FTE basis assuming a 35% tax rate. DISCUSSION OF RESULTS OF OPERATIONS This section provides a review of financial performance from a consolidated perspective. It also includes a Significant Items section... -

Page 46

... net deferred tax asset relating to the assets acquired from the March 31, 2009 restructuring. • During the 2010 second quarter, the portfolio of Franklin-related loans ($333.0 million of residential mortgages and $64.7 million of home equity loans) was transferred to loans held for sale. At the... -

Page 47

...addition to the items discussed separately in this section, a number of other items impacted financial results. These included: 2009 • $23.6 million ($0.03 per common share) negative impact due to a special FDIC insurance premium assessment. This amount was recorded to noninterest expense. • $12... -

Page 48

... held for sale ...Net tax benefit recognized(4) ...Franklin relationship restructuring(4) ...Net gain on early extinguishment of debt...Gain related to sale of Visa» stock ...Deferred tax valuation allowance benefit(4) ...Goodwill impairment ...FDIC special assessment ...Preferred stock conversion... -

Page 49

...(primarily loans, securities, and direct financing leases), and interest expense of funding sources (primarily interest-bearing deposits and borrowings). Earning asset balances and related funding sources, as well as changes in the levels of interest rates, impact net interest income. The difference... -

Page 50

... Yield/ Rate Total Loans and direct financing leases ...$(71.3) Investment securities ...96.8 Other earning assets ...(3.8) Total interest income from earning assets . . Deposits ...Short-term borrowings ...Federal Home Loan Bank advances ...Subordinated notes and other long-term debt, including... -

Page 51

...Commercial real estate ...Total commercial ...Automobile loans and leases ...Home equity ...Residential mortgage ...Other consumer ...Total consumer ...Total loans and leases ...Deposits Demand deposits - noninterest-bearing ...Demand deposits - interest-bearing ...Money market deposits ...Savings... -

Page 52

...Commercial real estate ...Total commercial ...Automobile loans and leases ...Home equity ...Residential mortgage ...Other consumer ...Total consumer ...Total loans and leases ...Deposits Demand deposits - noninterest-bearing ...Demand deposits - interest-bearing ...Money market deposits ...Savings... -

Page 53

... mortgages reflecting the impact of loan sales, as well as the continued refinance of portfolio loans. The majority of this refinance activity was fixed-rate loans, which we typically sell in the secondary market. Partially offset by: • $0.2 billion, or 3%, increase in average home equity loans... -

Page 54

...) 2010 2008 Interest-bearing deposits in banks ...Trading account securities...Federal funds sold and securities purchased under resale agreement ...Loans held for sale ...Investment securities: Taxable ...Tax-exempt ...Total investment securities ...Loans and leases:(3) Commercial: Commercial... -

Page 55

...Average Rate(2) 2010 2009 2008 Interest-bearing deposits in banks ...Trading account securities ...Federal funds sold and securities purchased under resale agreement. Loans held for sale ...Investment securities: Taxable...Tax-exempt ...Total investment securities ...Loans and leases:(3) Commercial... -

Page 56

... all our loan portfolios, although our commercial loan portfolios were the most affected. The following table details the Franklin-related impact to the provision for credit losses for each of the past four years. Table 10 - Provision for Credit Losses - Franklin-Related Impact 2010 (Dollar amounts... -

Page 57

...2009 2010 (Dollar amounts in thousands) Amount Percent 2009 Change from 2008 Amount Percent 2008 Service charges on deposit accounts ...Mortgage banking income ...Trust services ...Electronic banking ...Insurance income ...Brokerage income ...Bank owned life insurance income ...Automobile operating... -

Page 58

...marketing ...Servicing fees...Amortization of capitalized servicing(1) ...Other mortgage banking income ...Sub-total ...MSR valuation adjustment(1) ...Net trading gains (losses) related to MSR hedging ...Total mortgage banking income . . Mortgage originations (in millions) ...Average trading account... -

Page 59

... banking philosophy during the 2010 third quarter, as well as the continued underlying decline in activity as customers better manage their account balances. As part of our Fair Play banking philosophy, we voluntary reduced certain NSF / OD fees and implemented our 24-Hour GraceTM overdraft policy... -

Page 60

... and additional third party processing fees. Partially offset by: • $22.3 million, or 18%, decline in trust services income, reflecting the impact of reduced market values on asset management revenues, as well as lower yields on proprietary money market funds. Noninterest Expense (This section... -

Page 61

... quarter, and was related to the sale of a small paymentsrelated business in July 2009. (See Goodwill discussion located within the Critical Account Policies and Use of Significant Estimates for additional information). • $91.4 million increase in deposit and other insurance expense. This increase... -

Page 62

... remain open to examination, including Ohio, Kentucky, Indiana, Michigan, Pennsylvania, West Virginia and Illinois. Both the IRS and state tax officials, including Ohio and Kentucky, have proposed adjustments to our previously filed tax returns. We believe that our tax positions related to... -

Page 63

..., and managing of our credit risk. In addition to the traditional credit risk mitigation strategies of credit policies and processes, market risk management activities, and portfolio diversification, we added more quantitative measurement capabilities utilizing external data sources, enhanced... -

Page 64

... estate properties, real estate investment trusts, and real estate developers. We mitigate our risk on these loans by requiring collateral values that exceed the loan amount and underwriting the loan with projected cash flow in excess of the debt service requirement. These loans are made to finance... -

Page 65

... current low interest rate environment, many borrowers have utilized the line-of-credit home equity product as the primary source of financing their home. As a result, the proportion of first-lien loans has increased significantly in our portfolio over the past 24 months. Real estate market values... -

Page 66

...of our loans secured by real estate are discussed in detail in later sections. Commercial Credit The primary factors considered in commercial credit approvals are the financial strength of the borrower, assessment of the borrower's management capabilities, cash flows from operations, industry sector... -

Page 67

... review and assessment of the quality and / or risk of the new loan production. This group is part of our Risk Management area, and conducts portfolio reviews on a risk-based cycle to evaluate individual loans, validate risk ratings, as well as test the consistency of credit processes. Similarly... -

Page 68

... covenants. All Classified commercial loans are managed by our SAD. The SAD is a specialized credit group that handles the day-to-day management of workouts, commercial recoveries, and problem loan sales. Its responsibilities include developing action plans, assessing risk ratings, and determining... -

Page 69

... overall portfolio. CRE PORTFOLIO We manage the risks inherent in this portfolio the same as the C&I portfolio, with the addition of preleasing requirements, as applicable. Generally, we: (1) limit our loans to 80% of the appraised value of the commercial real estate, (2) require net operating cash... -

Page 70

... 17 - Core Commercial Real Estate Loans by Property Type and Property Location Ohio (Dollar amounts in millions) At December 31, 2010 Michigan Pennsylvania Indiana Kentucky Florida West Virginia Other Total Amount % Core portfolio: Retail properties ...$ 458 Office...Multi family ...Industrial and... -

Page 71

... property type, geographic location, and other data, to assess and manage our credit concentration risks. We review the majority of this portfolio segment on a monthly basis. Single Family Home Builders At December 31, 2010, we had $0.6 billion of CRE loans to single family home builders. Such loans... -

Page 72

... increased risk levels, we believe our strategy and operational capabilities significantly mitigate these risks. RESIDENTIAL-SECURED PORTFOLIOS The residential mortgage and home equity portfolios are primarily located throughout our footprint. The continued slowdown in the housing market negatively... -

Page 73

.... Home Equity Portfolio Our home equity portfolio (loans and lines-of-credit) consists of both first- and second- mortgage loans with underwriting criteria based on minimum credit scores, debt-to-income ratios, and LTV ratios. We offer closed-end home equity loans which are generally fixed-rate with... -

Page 74

... applicable regulations, for loans identified as higher risk. Loans are identified as higher risk based on performance indicators and the updated values are utilized to facilitate our portfolio management, as well as our workout and loss mitigation functions. We continue to make origination policy... -

Page 75

... loans held for sale(2) ...Other nonperforming assets(3) ... Total nonperforming assets ...$844,752 Nonaccrual loans as a % of total loans and leases ...Nonperforming assets ratio(4) ...Nonperforming Franklin assets(1) Commercial ...Residential mortgage ...Other real estate owned ...Home equity... -

Page 76

... December 31, 2009, nonaccrual Franklin loans were reported as residential mortgage loans, home equity loans, and other real estate owned. (2) Represents impaired loans obtained from the Sky Financial acquisition. Held for sale loans are carried at the lower of cost or fair value less costs to sell... -

Page 77

... of year ...$2,058,091 New nonperforming assets ...925,699 Franklin-related impact, net(1) ...(329,023) Acquired nonperforming assets ...- Returns to accruing status ...(370,798) Loan and lease losses ...(639,766) Other real estate owned losses ...(7,936) Payments ...(650,429) Sales ...(141,086... -

Page 78

... and the terms of the loan are modified to meet a borrower's specific circumstances at a point in time. All loan modifications, including those classified as TDRs, are reviewed and approved. Our ALLL is largely driven by updated risk ratings to commercial loans, updated borrower credit scores on... -

Page 79

... new notes. The senior note is underwritten based upon our normal underwriting standards at current market rates and is sized so projected cash flows are sufficient to repay contractual principal and interest. The terms on the subordinate note(s) vary by situation, but often defer interest payments... -

Page 80

...31, 2009, nonaccrual Franklin loans were reported as residential mortgage loans, home equity loans, and other real estate owned. The over 90-day delinquency ratio for total loans not guaranteed by a U.S. government agency was 0.23% at December 31, 2010, representing a 17 basis point decline compared... -

Page 81

... the single family home builder and developer loans in the commercial portfolio, experienced the majority of the credit issues related to the residential real estate market. We regularly assess the adequacy of the ACL by performing on-going evaluations of the loan and lease portfolio, including such... -

Page 82

...3,451 1,902 1,163 Total commercial real estate ...28,433 13,951 3,456 1,950 1,765 Total commercial ...90,272 51,607 15,725 15,567 14,141 Consumer: Automobile loans and leases ...19,736 19,809 17,543 13,549 15,014 Home equity ...1,458 4,224 2,901 2,795 3,096 Residential mortgage ...10,532 1,697 1,765... -

Page 83

... Loan and Lease Losses and Allowance for Credit Losses - Franklin-Related Impact 2010 (Dollar amounts in millions) 2009 December 31, 2008 2007 2006 Allowance for loan and lease losses Franklin ...$ - Non-Franklin ...1,249.0 Total ...$ 1,249.0 Allowance for credit losses Franklin ...$ - Non-Franklin... -

Page 84

...in commercial real estate valuations for properties located in areas with limited sale or refinance activities. Residential real estate values continued to be negatively impacted by high unemployment, increased foreclosure activity, and the elimination of home-buyer tax credits. In the near-term, we... -

Page 85

... industrial ...$ 340,614 Commercial real estate ...588,251 Total commercial ...928,865 Consumer Automobile loans and leases Home equity ...Residential mortgage ...Other loans ...49,488 150,630 93,289 26,736 320,143 1,249,008 42,127 34% $ 492,205 18 751,875 52 1,244,080 15 20 12 1 48 100% 57,951 102... -

Page 86

... real estate: Construction ...Commercial ...Commercial real estate ...Total commercial ...Consumer: Automobile loans and leases ...Home equity ...Residential mortgage ...Other loans ...Total consumer ...Net charge-offs as a % of average loans ...(1) Percentage of related average loan balances... -

Page 87

...30 - Net Loan and Lease Charge-offs - Franklin-Related Impact 2010 (Dollar amounts in millions) 2009 December 31, 2008 2007 2006 Commercial and industrial net charge-offs (recoveries) Franklin ...Non-Franklin ...Total ...Commercial and industrial net charge-offs ratio Total ...Non-Franklin ...Total... -

Page 88

...-term positive view for the performance of the home equity portfolio. We have been successful in originating new loans to higher quality borrowers, as evidenced by our 2010 home equity line-of-credit originations were 100% current as of December 31, 2010. Non-Franklin-related residential mortgage... -

Page 89

...,457 5.2 (1) The average duration assumes a market driven pre-payment rate on securities subject to pre-payment. Table 32 - Available-for-sale and Other Securities Portfolio Composition and Maturity At December 31, 2010 Amortized Cost Fair Value (Dollar amounts in thousands) Yield(1) U.S. Treasury... -

Page 90

... related to Alt-A securities. Given the continued disruption in the housing and financial markets, we may be required to recognize additional credit OTTI losses in future periods with respect to our available-for-sale and other securities portfolio. The amount and timing of any additional credit... -

Page 91

...projected cash flows. These reviews are supported with analysis from independent third parties. (See the Investment Securities section located within the Critical Accounting Policies and Use of Significant Estimates section for additional information). The following table presents the credit ratings... -

Page 92

... of business through exposures to market interest rates, foreign exchange rates, equity prices, credit spreads, and expected lease residual values. We have identified two primary sources of market risk: interest rate risk and price risk. Interest Rate Risk OVERVIEW Interest rate risk is the risk to... -

Page 93

... value analysis. An income simulation analysis is used to measure the sensitivity of forecasted net interest income to changes in market rates over a one-year time period. Although bank owned life insurance, automobile operating lease assets, and excess cash balances held at the Federal Reserve Bank... -

Page 94

...2010 for the +200 basis points scenario shows a change to a neutral near-term interest rate risk position compared with December 31, 2009. The primary factors contributing to this change are the decline in market interest rates over the course of 2010 along with growth in deposits and net free funds... -

Page 95

... of 2010 along with growth in deposits and net free funds, offset by increases in fixed-rate loans, securities, and interest rate swaps used for asset-liability management purposes. The following table shows the economic value sensitivity of select portfolios to changes in market interest rates. The... -

Page 96

... of any credit rating changes and / or other trigger events related to financial ratios, deposit fluctuations, debt issuance capacity, stock performance, or negative news related to us or the banking industry. Liquidity risk is reviewed monthly for the Bank and the parent company, as well... -

Page 97

... Bank's and the parent company's credit ratings and /or outlook resulting in a significantly lower rate on the $300.0 million of subordinated debt issued in December of 2010. Bank Liquidity and Sources of Liquidity Our primary sources of funding for the Bank are retail and commercial core deposits... -

Page 98

... by commercial loans and home equity lines-of-credit. The Bank is also a member of the FHLB, and as such, has access to advances from this facility. These advances are generally secured by residential mortgages, other mortgage-related loans, and available-for-sale securities. Information regarding... -

Page 99

...loans, (5) selling of national market certificates of deposit, (6) the relatively shorter-term structure of our commercial loans (see tables below) and automobile loans, and (7) issuing of common and preferred stock. At December 31, 2010, we believe the Bank had sufficient liquidity to meet its cash... -

Page 100

... relating to the mortgage banking business to hedge the exposures we have from commitments to extend new residential mortgage loans to our customers and from our mortgage loans held for sale. At December 31, 2010, and December 31, 2009, we had commitments to sell residential real estate loans... -

Page 101

... or Less (Dollar amounts in millions) 1 to 3 Years December 31, 2010 3 to 5 More than Years 5 Years Total Deposits without a stated maturity ...Certificates of deposit and other time deposits ...FHLB advances ...Short-term borrowings ...Other long-term debt ...Subordinated notes...Operating lease... -

Page 102

... alleged irregularities in the mortgage loan foreclosure processes of certain high volume loan servicers, state law enforcement authorities, the United States Department of Justice, and other federal agencies have stated they are investigating mortgage servicers foreclosure practices, and private... -

Page 103

... the Notes to the Consolidated Financial Statements.) Capital is managed both at the Bank and on a consolidated basis. Capital levels are maintained based on regulatory capital requirements and the economic capital required to support credit, market, liquidity, and operational risks inherent in our... -

Page 104

... 2010 (Dollar amounts in millions) 2009 December 31, 2008 2007 2006 Consolidated capital calculations: Common shareholders' equity ...Preferred shareholders' equity ...Total shareholders' equity ...Goodwill ...Intangible assets...Intangible asset deferred tax liability(1) ...Total tangible equity... -

Page 105

... utilized in the calculation of our consolidated Tier 1, Tier 2, and total risk-based capital amounts during 2010. Table 45 - Regulatory Capital Activity Common Shareholders' Equity(1) (Dollar amounts in millions) Preferred Shareholders' Equity Qualifying Core Capital(2) Disallowed Goodwill... -

Page 106

...on the execution of strategic plans. We have four major business segments: Retail and Business Banking; Commercial Banking; Automobile Finance and Commercial Real Estate; and Wealth Advisors, Government Finance, and Home Lending. A Treasury / Other function includes our insurance business, and other... -

Page 107

... relate to customer derivatives and brokerage services, which are recorded by WGH and shared primarily with Retail and Business Banking and Commercial Banking. Results of operations for the business segments reflect these fee sharing allocations. Expense Allocation The management accounting process... -

Page 108

...) ...$312,347 $(3,094,179) (1) Represents the 2009 first quarter impairment charge, net of tax, associated with the former Regional Banking business segment. See the Goodwill section located in Critical Accounting Policies and Use of Significant Estimates section for additional information. 94 -

Page 109

... ...Commercial real estate ...Total commercial ...Automobile loans and leases ...Home equity ...Residential mortgage ...Other consumer ...Total consumer ...Total loans ...Average Deposits Demand deposits - noninterest-bearing ...Demand deposits - interest-bearing ...Money market deposits...Savings... -

Page 110

... checking and money market deposit products. The $0.6 billion, or 5%, decline in total average loans and leases primarily reflected small business and consumer loan sales. Provision for credit losses declined $312.2 million, or 66%, reflecting lower NCOs, a $0.6 billion decrease in related average... -

Page 111

... million decline in deposit service charges resulting from the amendment to Reg E, the voluntary reduction or elimination of NSF / OD fees, a decline in the number of customers overdrafting their accounts, and our new 24-Hour GraceTM feature, reflecting our Fair Play banking philosophy. The decrease... -

Page 112

...and (4) $2.9 million increase of loan-related fees relating to the improved collection of such fees from customers. These increases were partially offset by a $4.0 million decline in equipment operating lease income as lease originations were structured as direct finance leases beginning in the 2009... -

Page 113

...as the underlying credit quality of the loan portfolios continues to improve and / or stabilize. The comparable year-ago period included higher provisions for credit losses to increase reserves due to economic and commercial real estate and automobileindustry-related weaknesses in our markets. Total... -

Page 114

... commercial real estate credit-related expenses (e.g. appraisals, loan collections, taxes, and OREO expenses) increased $6.2 million. These increases were partially offset by a $4.7 million decrease in losses associated with sales of vehicles returned at the end of their lease terms, as used vehicle... -

Page 115

... ...Number of employees (full-time equivalent) ...Total average assets (in millions) ...Total average loans/leases (in millions) ...Total average deposits (in millions) ...Net interest margin ...NCOs...NCOs as a % of average loans and leases ...Return on average common equity ...Mortgage banking... -

Page 116

... NCOs, including a $58.3 million increase in residential mortgage NCOs. Credit quality was stressed during 2009 consistent with economic conditions in the Company's markets. Mortgage banking income increased $100.5 million due to more favorable lending conditions in the first half of 2009. Partially... -

Page 117

... Loans/Leases - 2010 Fourth Quarter vs. 2009 Fourth Quarter Fourth Quarter 2010 2009 (Dollar amounts in millions) Change Amount Percent Average Loans/Leases Commercial and industrial ...Commercial real estate ...Total commercial ...Automobile loans and leases ...Home equity ...Residential mortgage... -

Page 118

... Quarter 2010 2009 (Dollar amounts in millions) Change Amount Percent Average Deposits Demand deposits: noninterest-bearing ...Demand deposits: interest-bearing ...Money market deposits ...Savings and other domestic deposits ...Core certificates of deposit ...Total core deposits...Other deposits... -

Page 119

... life insurance income. • $2.1 million, or 8%, increase in trust services income, with 50% of the increase due to increases in asset market values and the remainder reflecting growth in new business. Partially offset by: • $20.9 million, or 27%, decline in service charges on deposit accounts... -

Page 120

...Amount Percent Personnel costs ...Outside data processing and other services ...Net occupancy...Deposit and other insurance expense ...Professional services ...Equipment...Marketing ...Amortization of intangibles ...OREO and foreclosure expense ...Automobile operating lease expense ...Gain on early... -

Page 121

... centered in retail projects. The retail property portfolio remains the most susceptible to a continued decline in market conditions, but we believe that the combination of prior NCOs and existing reserves positions us well to make effective credit decisions in the future. While the office portfolio... -

Page 122

... defaults for second-lien home equity loans incur substantial losses given the reduced collateral equity. Our strategies focus on loss mitigation activity through early intervention and restructuring loan terms. Automobile loan and lease NCOs were $7.0 million, or an annualized 0.51%, down from $12... -

Page 123

......Cash dividends declared ...Common stock price, per share High(4) ...Low(4) ...Close ...Average closing price ...Return on average total assets ...Return on average common shareholders' equity ...Return on average tangible common shareholders' equity(5) ...Efficiency ratio(6) ...Effective tax rate... -

Page 124

... Income Statement, Capital, and Other Data - Continued(1) Capital Adequacy December 31, 2010 September 30, June 30, March 31, Total risk-weighted assets (in millions) ...Tier 1 leverage ratio ...Tier 1 risk-based capital ratio ...Total risk-based capital ratio ...Tangible common equity/asset ratio... -

Page 125

...970 4.209 3.727 Return on average total assets...(2.80)% (1.28)% (0.97)% Return on average common shareholders' equity ...(39.1) (21.5) (23.0) Return on average tangible common shareholders' equity(5) ...(45.1) (24.7) (27.2) Efficiency ratio(6) ...49.0 61.4 51.0 Effective tax rate (benefit) ...(38... -

Page 126

... and timing of our business strategies, including market acceptance of any new products or services introduced to implement our Fair Play banking philosophy; (6) changes in accounting policies and principles and the accuracy of our assumptions and estimates used to prepare our Consolidated Financial... -

Page 127

... from those estimates. The most significant accounting policies and estimates and their related application are discussed below. Total Allowance for Credit Losses Our ACL of $1.3 billion at December 31, 2010, represents our estimate of probable losses inherent in our loan and lease portfolio and our... -

Page 128

...which minimal information is released publicly. When observable market prices do not exist, we estimate fair value primarily by using cash flow and other financial modeling methods. Our valuation methods consider factors such as liquidity and concentration concerns and, for the derivatives portfolio... -

Page 129

...can be found in Note 19 of the Notes to the Consolidated Financial Statements. Financial Instrument(1) Hierarchy Valuation methodology Mortgage loans held for sale Level 2 Available-for-sale Securities & Trading Account Securities(2) Level 1 Huntington elected to apply the fair value option for... -

Page 130

... of basic asset and liability conversion swaps and options, and interest rate caps. These derivative positions are valued using a discounted cash flow method that incorporates current market interest rates. Consist primarily of interest rate lock agreements related to mortgage loan commitments. The... -

Page 131

... Level 3 in the fair value hierarchy. The collateral generally consisted of trust-preferred securities and subordinated debt securities issued by banks, bank holding companies, and insurance companies. A full cash flow analysis was used to estimate fair values and assess impairment for each security... -

Page 132

... loan and deposit growth. The long-term growth rate used in determining the terminal value was estimated at 2.5%. The discount rate of 14% was estimated based on the Capital Asset Pricing Model, which considered the risk-free interest rate (20-year Treasury Bonds), market-risk premium, equity-risk... -

Page 133

... rate. The marks on our outstanding debt and deposits were based upon observable trades or modeled prices using then current yield curves and market spreads. The valuation of the loan portfolio indicated discounts in the ranges of 9%-24%, depending upon the loan type. The estimated fair value... -

Page 134

... commercial loans at December 31, 2010. PENSION Pension plan assets consist of mutual funds and our common stock. Investments are accounted for at cost on the trade date and are reported at fair value. Mutual funds are valued at quoted Net Asset Value. Our common stock is traded on a national... -

Page 135

... to income and nonincome taxes. The effective tax rate is based in part on our interpretation of the relevant current tax laws. We believe the aggregate liabilities related to taxes are appropriately reflected in the consolidated financial statements. We review the appropriate tax treatment of all... -

Page 136

... About Market Risk Information required by this item is set forth in the Market Risk section which is incorporated by reference into this item. Item 8: Financial Statements and Supplementary Data Information required by this item is set forth in the Report of Independent Registered Public Accounting... -

Page 137

...of the Consolidated Financial Statements in conformity with accounting principles generally accepted in the United States. Huntington's Management assessed the effectiveness of the Company's internal control over financial reporting as of December 31, 2010. In making this assessment, Management used... -

Page 138

... REGISTERED PUBLIC ACCOUNTING FIRM To the Board of Directors and Shareholders of Huntington Bancshares Incorporated Columbus, Ohio We have audited the internal control over financial reporting of Huntington Bancshares Incorporated and subsidiaries (the "Company") as of December 31, 2010, based on... -

Page 139

... Incorporated Columbus, Ohio We have audited the accompanying consolidated balance sheets of Huntington Bancshares Incorporated and subsidiaries (the "Company") as of December 31, 2010 and 2009, and the related consolidated statements of income, changes in shareholders' equity, and cash flows... -

Page 140

... December 31, 2010 (Dollar amounts in thousands, except number of shares) ASSETS Cash and due from banks ...Interest-bearing deposits in banks ...Trading account securities ...Loans held for sale (includes $754,117 and $459,719 respectively, measured at fair value)(1) Available-for-sale and other... -

Page 141

... for credit losses ...Service charges on deposit accounts ...Mortgage banking income ...Trust services ...Electronic banking ...Insurance income ...Brokerage income ...Bank owned life insurance income ...Automobile operating lease income ...Net gains (losses) on sales of available-for-sale and... -

Page 142

Huntington Bancshares Incorporated Consolidated Statements of Changes in Shareholders' Equity Preferred Stock Series B Series A Common Stock Shares Amount Shares Amount Shares Amount (All amounts in thousands, except for per share amounts) Accumulated Other Retained Treasury Stock Comprehensive ... -

Page 143

Huntington Bancshares Incorporated Consolidated Statements of Changes in Shareholders' Equity Accumulated Preferred Stock Other Retained Series B Series A Common Stock Capital Treasury Stock Comprehensive Earnings Loss Shares Amount Shares Amount Shares Amount Surplus Shares Amount (Deficit) (All ... -

Page 144

Huntington Bancshares Incorporated Consolidated Statements of Changes in Shareholders' Equity Accumulated Preferred Stock Other Series B Series A Common Stock Capital Treasury Stock Comprehensive Retained Loss Earnings Shares Amount Shares Amount Shares Amount Surplus Shares Amount (All amounts in ... -

Page 145

... assets ...Proceeds from sale of operating lease assets ...Purchases of premises and equipment ...Proceeds from sales of other real estate ...Other, net...Net cash provided by (used for) investing activities ...Financing activities Increase (decrease) in deposits ...Increase (decrease) in short-term... -

Page 146

... financing, equipment leasing, investment management, trust services, brokerage services, customized insurance service programs, and other financial products and services. Huntington's banking offices are located in Ohio, Michigan, Pennsylvania, Indiana, West Virginia, and Kentucky. Select financial... -

Page 147

... income. Direct financing leases are reported at the aggregate of lease payments receivable and estimated residual values, net of unearned and deferred income. Interest income is accrued as earned using the interest method based on unpaid principal balances. Huntington defers the fees it receives... -

Page 148

... or lease sales with servicing retained, a servicing asset is recorded at fair value for the right to service the loans sold. To determine the fair value, Huntington uses an option adjusted spread cash flow analysis incorporating market implied forward interest rates to estimate the future direction... -

Page 149

... changing market and economic conditions on portfolio performance. The risk-profile component considers items unique to our structure, policies, processes, and portfolio composition, as well as qualitative measurements and assessments of the loan portfolios including, but not limited to, management... -

Page 150

...is reversed with current year accruals charged to interest income, and prior year amounts charged-off as a credit loss. Classes are generally disaggregations of a portfolio. For ACL purposes, the Company's portfolios are: C&I, CRE, Automobile loans and leases, Residential mortgages, Home equity, and... -

Page 151

...'s bank owned life insurance policies are carried at their cash surrender value. Huntington recognizes tax-exempt income from the periodic increases in the cash surrender value of these policies and from death benefits. A portion of cash surrender value is supported by holdings in separate accounts... -

Page 152

... its mortgage loans held for sale. Mortgage loan sale commitments and the related interest rate lock commitments are carried at fair value on the Consolidated Balance Sheet with changes in fair value reflected in mortgage banking revenue. Huntington also uses certain derivative financial instruments... -

Page 153

.... Share-Based Compensation - Huntington uses the fair value recognition concept relating to its sharebased compensation plans. Compensation expense is recognized based on the fair value of unvested stock options and awards over the requisite service period. Segment Results - Accounting policies for... -

Page 154

... loan portfolio in the notes to financial statements, such as aging information and credit quality indicators. Both new and existing disclosures must be disaggregated by portfolio segment or class. The disaggregation of information is based on how Huntington develops its ACL and how it manages its... -

Page 155

..., we recorded $87.0 million of Franklin-related provision for credit losses and NCOs, of which $75.5 million related to the loan sales. At December 31, 2010, the only nonperforming Franklin-related assets remaining were $9.5 million of OREO properties, which have been marked to the lower of cost or... -

Page 156

... billion of real estate loans were pledged to secure advances from the Federal Home Loan Bank. 4. AVAILABLE-FOR-SALE AND OTHER SECURITIES The following tables provide amortized cost, fair value, and gross unrealized gains and losses recognized in OCI by investment category at December 31, 2010 and... -

Page 157

....4 million, of Federal Reserve Bank stock, respectively. Other securities also include corporate debt and marketable equity securities. Nonmarketable equity securities are valued at amortized cost. At December 31, 2010 and 2009, Huntington did not have any material equity positions in FNMA or FHLMC... -

Page 158

... securities with unrealized losses aggregated by investment category and the length of time the individual securities have been in a continuous loss position, at December 31, 2010 and 2009. Less than 12 Months Fair Unrealized Value Losses (Dollar amounts in thousands) Over 12 Months Fair Unrealized... -

Page 159

... of debt securities issued by financial institutions. The collateral generally consisted of trust-preferred securities and subordinated debt securities issued by banks, bank holding companies, and insurance companies. A full cash flow analysis was used to estimate fair values and assess impairment... -

Page 160

... in OCI on debt securities held by Huntington for the years ended December 31, 2010 and 2009 as follows: Year Ended December 31, 2010 2009(1) (Dollar amounts in thousands) Balance, beginning of year ...Reductions from sales ...Credit losses not previous recognized ...Change in expected cash flows... -

Page 161

... separated from the underlying mortgage loans by sale or securitization of the loans with servicing rights retained. At initial recognition, the MSR asset is established at its fair value using assumptions consistent with assumptions used to estimate the fair value of existing MSRs carried... -

Page 162

... value associated with loans that paid off during the period. (3) Represents change in value resulting primarily from market-driven changes in interest rates and prepayment spreads. Amortization Method (Dollar amounts in thousands) 2010 2009 Carrying value, beginning of year ...New servicing assets... -

Page 163

...10% and an estimated return on payments prior to remittance to investors. The servicing asset is then amortized against servicing income. Impairment, if any, is recognized when carrying value exceeds the fair value as determined by calculating the present value of expected net future cash flows. The... -

Page 164

... the contractual terms of the loan agreement. The recovery of the investment in impaired loans with no specific reserves generally is expected from the sale of collateral, net of costs to sell that collateral. (2) As a result of the troubled debt restructuring, the loans to Franklin of $0.7 billion... -

Page 165

... by portfolio segment for the year ended December 31, 2010: Commercial Automobile and Commercial Loans and Home Residential Other Leases Equity(1) Mortgage(2) Consumer Industrial Real Estate (Dollar amounts in thousands) Allowance for Loan and Lease Losses: Balance at January 1, 2010: ...Loan charge... -

Page 166

... Total Credit Risk Profile by FICO score(1) 650-749 G650 Other(2) Automobile loans and leases ...Home equity loans and lines-of-credit: Secured by first-lien ...Secured by second-lien ...Residential mortgage ...Other consumer loans ...(1) Reflects currently updated customer credit scores. $2,516... -

Page 167

... real estate: Retail properties ...Multi family ...Office ...Industrial and warehouse ...Other commercial real estate ...Total CRE ...Automobile loans and leases ...Home equity loans and lines-of-credit: Secured by first-lien ...Secured by second-lien ...Residential mortgage ...Other consumer loans... -

Page 168

...C&I ...Commercial real estate: Retail properties ...Multi family...Office ...Industrial and warehouse ...Other commercial real estate ...Total CRE ...Automobile loans and leases ...Home equity loans and lines-of-credit: Secured by first-lien . . Secured by secondlien ...Residential mortgage ...Other... -

Page 169

... Retail properties ...$ 32.0 Multi family ...5.1 Office ...2.3 Industrial and warehouse...3.3 Other commercial real estate ...26.7 Total CRE ...$ 69.4 Automobile loans and leases ...$ - Home equity loans and lines-of-credit: Secured by first-lien ...- Secured by second-lien ...- Residential mortgage... -

Page 170

... Real Estate segments. Regional Banking goodwill was assigned to the new reporting units affected using a relative fair value allocation. Automobile Finance and Dealer Services (AFDS), Private Financial Group (PFG), and Treasury / Other remained essentially unchanged. In late 2010, Huntington... -

Page 171

At December 31, 2010 and 2009, Huntington's other intangible assets consisted of the following: Gross Carrying Amount (Dollar amounts in thousands) Accumulated Amortization Net Carrying Value December 31, 2010 Core deposit intangible ...$376,846 Customer relationship ...104,574 Other ...25,164 ... -

Page 172

...agreements to repurchase ...Commercial paper ...Other borrowings ...Total short-term borrowings ... $1,965,677 100 74,955 $2,040,732 $851,285 700 24,256 $876,241 Other borrowings consist of borrowings from the Treasury and other notes payable. 10. FEDERAL HOME LOAN BANK ADVANCES Huntington's long... -

Page 173

...Huntington or any consolidated affiliates. The transfer did not meet the sale requirement of ASC 860 and therefore has been recorded as a secured financing on the Consolidated Balance Sheet of Huntington at December 31, 2010. In the 2009 first quarter, the Bank issued $600 million of guaranteed debt... -

Page 174

... swaps, are used to match the funding rates on certain assets to hedge the interest rate values of certain fixed-rate debt by converting the debt to a variable rate. See Note 20 for more information regarding such financial instruments. All principal is due upon maturity of the note as described in... -

Page 175

...-for-sale debt securities ...Net change in unrealized holding gains (losses) on available-for-sale equity securities ...Unrealized gains and losses on derivatives used in cash flow hedging relationships arising during the period ...Change in pension and post-retirement benefit plan assets and... -

Page 176

... change in unrealized holding (losses) gains on available-for-sale equity securities ...Unrealized gains and losses on derivatives used in cash flow hedging relationships arising during the period ...Cumulative effect of changing measurement date provisions for pension and post-retirement assets and... -

Page 177

...the preferred stock and additional paid-in-capital for the warrant based on their relative fair values. The resulting discount on the preferred stock was amortized against retained earnings and was recorded in Huntington's Consolidated Statements of Income as dividends on preferred shares, resulting... -

Page 178

... investors. In aggregate, 0.2 million shares of Series A Preferred Stock were exchanged for 41.1 million shares of Huntington Common Stock. A deemed dividend of $56.0 million was recorded for common shares issued in excess of the stated conversion rate. Each share of the Series A Preferred Stock... -

Page 179

...-BASED COMPENSATION Huntington sponsors nonqualified and incentive share based compensation plans. These plans provide for the granting of stock options and other awards to officers, directors, and other employees. Compensation costs are included in personnel costs on the Consolidated Statements... -

Page 180

... employee turnover, and adjusted share-based compensation expense to account for the higher forfeiture rate. Huntington's stock option activity and related information for the year ended December 31, 2010, was as follows: WeightedAverage Exercise Price WeightedAverage Remaining Contractual Life... -

Page 181

...The IRS and state tax officials from Ohio and Kentucky have proposed adjustments to the Company's previously filed tax returns. Management believes the tax positions taken by the Company related to such proposed adjustments were correct and supported by applicable statutes, regulations, and judicial... -

Page 182

... adverse impact on our consolidated financial position. Huntington accounts for uncertainties in income taxes in accordance with ASC 740, Income Taxes. At December 31, 2010, Huntington had gross unrecognized tax benefits of $49.5 million in income tax liability related to tax positions. Due to the... -

Page 183

... bank owned life insurance income ...(20,595) Asset securitization activities ...46,160 Federal tax loss carryforward /carryback ...- General business credits...(23,360) Reversals of valuation allowance ...(899) Capital loss ...(62,681) Loan acquisitions ...(43,650) Goodwill impairment ...- State... -

Page 184

... ...Pension and other employee benefits ...Loan acquisitions...Other ...Deferred tax liabilities: Lease financing ...Securities adjustments ...Purchase accounting adjustments ...Mortgage servicing rights...Loan origination costs ...Operating assets ...Partnership investments ...Other ... ...$457,692... -

Page 185

... plan. For any employee retiring on or after January 1, 1993, post-retirement healthcare benefits are based upon the employee's number of months of service and are limited to the actual cost of coverage. Life insurance benefits are a percentage of the employee's base salary at the time of retirement... -

Page 186

... plan year based upon historical returns and projected returns on the underlying mix of invested assets. The following table reconciles the beginning and ending balances of the benefit obligation of the Plan and the post-retirement benefit plan with the amounts recognized in the consolidated balance... -

Page 187

... with the amounts recognized in the consolidated balance sheets: Pension Benefits 2010 2009 (Dollar amounts in thousands) Fair value of plan assets at beginning of measurement year ...$454,114 Changes due to: Actual return on plan assets ...55,583 Employer contributions ...79 Settlements ...(20,911... -

Page 188

... Huntington National Bank, as trustee, held all Plan assets. The Plan assets consisted of investments in a variety of Huntington mutual funds and Huntington common stock as follows: Fair Value 2010 (Dollar amounts in thousands) 2009 Cash ...Cash equivalents: Huntington funds - money market ...Other... -

Page 189

... healthcare cost trend rate assumption based on current market data and Huntington's claims experience. This trend rate is expected to decline over time to a trend level consistent with medical inflation and long-term economic assumptions. Huntington also sponsors other retirement plans, the most... -

Page 190

Pretax (Dollar amounts in thousands) 2010 Tax (Expense) Benefit After-tax Balance, beginning of year ...$(173,029) Net actuarial (loss) gain: Amounts arising during the year ...(45,804) Amortization included in net periodic benefit costs ...23,313 Prior service cost: Amounts arising during the ... -

Page 191

... dates. Dividends received on shares of Huntington common stock by the plan were $5.6 million during 2010 and $5.1 million during 2009. 19. FAIR VALUES OF ASSETS AND LIABILITIES Fair value is defined as the exchange price that would be received for an asset or paid to transfer a liability (an... -

Page 192

.... At December 31, 2010, mortgage loans held for sale had an aggregate fair value of $754.1 million and an aggregate outstanding principal balance of $750.0 million. Interest income on these loans is recorded in interest and fee income - loans and leases. Included in mortgage banking income were net... -

Page 193

... of basic asset and liability conversion swaps and options, and interest rate caps. These derivative positions are valued using a discounted cash flow method that incorporates current market interest rates. Consist primarily of interest rate lock agreements related to mortgage loan commitments. The... -

Page 194

... and 2009 are summarized below: Fair Value Measurements at Reporting Date Using Level 1 Level 2 Level 3 (Dollar amounts in thousands) Netting Adjustments(1) Balance at December 31, 2010 Assets Mortgage loans held for sale ...Trading account securities: U.S. Treasury securities ...Federal agencies... -

Page 195

Fair Value Measurements at Reporting Date Using Level 1 Level 2 Level 3 (In thousands) Netting Adjustments (1) Balance at December 31, 2009 Assets Mortgage loans held for sale ...$ Trading account securities: U.S. Treasury securities Federal agencies: Mortgagebacked ...Municipal securities ...... -

Page 196

... of the reporting period. Level 3 Fair Value Measurements Year Ended December 31, 2010 Available-for-Sale Securities AssetMunicipal PrivateBacked Securities Label CMO Securities MSRs (Dollar amounts in thousands) Derivative Instruments Automobile Loans Equity Investments Balance, beginning of... -

Page 197

MSRs (Dollar amounts in thousands) Level 3 Fair Value Measurements Year Ended December 31, 2009 Available-for-Sale Securities AssetBacked Derivative Municipal Private Instruments Securities Label CMO Securities Automobile Equity Loans Investments Balance, beginning of year ...Total gains/losses: ... -

Page 198

...Value Measurements Year Ended December 31, 2010 Available-for-Sale Securities AssetBacked Automobile Equity Derivative Municipal Private Loans Investments Instruments Securities Label CMO Securities MSRs (Dollar amounts in thousands) Classification of gains and losses in earnings: Mortgage banking... -

Page 199

... and other assets ... $80.4 66.8 $- - $- - $80.4 66.8 $(39.6) $ (6.9) Periodically, Huntington records nonrecurring adjustments of collateral-dependent loans measured for impairment when establishing the allowance for credit losses. Such amounts are generally based on the fair value of the... -

Page 200

... Value Financial Assets: Cash and short-term assets ...Trading account securities...Loans held for sale ...Investment securities ...Net loans and direct financing leases ...Derivatives ...Financial Liabilities: Deposits ...Short-term borrowings ...Federal Home Loan Bank advances...Other long term... -

Page 201

.... The fair values of fixed-rate time deposits are estimated by discounting cash flows using interest rates currently being offered on certificates with similar maturities. Debt Fixed-rate, long-term debt is based upon quoted market prices, which are inclusive of Huntington's credit risk. In the... -

Page 202

...in Huntington's asset and liability management activities at December 31, 2010, identified by the underlying interest rate-sensitive instruments: Fair Value Hedges (Dollar amounts in thousands) Cash Flow Hedges Total Instruments associated with: Loans ...Deposits ...Subordinated notes ...Other long... -

Page 203

...in fair value of interest rate swaps hedging other long-term debt(2) ...1,847 (6,201) 9,859 Change in fair value of hedged other long-term debt(2) ...(1,847) 6,201 (9,859) (1) Effective portion of the hedging relationship is recognized in Interest expense - deposits in the Consolidated Statements of... -

Page 204

... payments at designated times. To the extent these derivatives are effective in offsetting the variability of the hedged cash flows, changes in the derivatives' fair value will not be included in current earnings but are reported as a component of OCI in the Consolidated Statements of Shareholders... -

Page 205

...expose Huntington to market risk but not credit risk. Purchased options contain both credit and market risk. The interest rate risk of these customer derivatives is mitigated by entering into similar derivatives having offsetting terms with other counterparties. The credit risk to these customers is... -

Page 206

... Huntington consolidated the 2009 Trust containing automobile loans on January 1, 2010. Huntington elected the fair value option under ASC 825, Financial Instruments, for both the automobile loans and the related debt obligations. Upon adoption of the new accounting standards, total assets increased... -

Page 207

Consolidated Financial Statements. A list of trust-preferred securities outstanding at December 31, 2010 follows: Rate Principal Amount of Subordinated Note/ Debenture Issued to Trust (1) Investment in Unconsolidated Subsidiary (2) (Dollar amounts in thousands) Huntington Capital I...Huntington ... -

Page 208

... issued by customers and remarketed by The Huntington Investment Company, the Company's broker-dealer subsidiary. Huntington uses an internal loan grading system to assess an estimate of loss on its loan and lease portfolio. The same loan grading system is used to help monitor credit risk associated... -

Page 209

... relating to its mortgage banking business to hedge the exposures from commitments to make new residential mortgage loans with existing customers and from mortgage loans classified as held for sale. At December 31, 2010 and 2009, Huntington had commitments to sell residential real estate loans... -

Page 210

...can initiate certain actions by regulators that, if undertaken, could have a material adverse effect on Huntington's and the Bank's financial statements. Applicable capital adequacy guidelines require minimum ratios of 4.00% for Tier 1 Risk-based Capital, 8.00% for Total Risk-based Capital, and 4.00... -

Page 211

... 24. PARENT COMPANY FINANCIAL STATEMENTS The parent company condensed financial statements, which include transactions with subsidiaries, are as follows. Balance Sheets (Dollar amounts in thousands) December 31, 2010 2009 ASSETS Cash and cash equivalents(1) ...Due from The Huntington National Bank... -

Page 212

Statements of Income (Dollar amounts in thousands) 2010 Year Ended December 31, 2009 2008 Income Dividends from The Huntington National Bank ...Non-bank subsidiaries ...Interest from The Huntington National Bank ...Non-bank subsidiaries ...Other ... ...$ - ...33,000 ...82,749 12,185 2,987 130,921... -

Page 213

... align certain business unit reporting with segment executives to accelerate cross-sell results and provide greater focus on the execution of strategic plans. We have four major business segments: Retail and Business Banking, Commercial Banking, Automobile Finance and Commercial Real Estate, and... -

Page 214

... services to consumer and small business customers located within our primary banking markets consisting of five areas covering the six states of Ohio, Michigan, Pennsylvania, Indiana, West Virginia, and Kentucky. Its products include individual and small business checking accounts, savings accounts... -

Page 215

... is certain operating basis financial information reconciled to Huntington's 2010, 2009, and 2008 reported results by line of business: Retail & Business Banking Former Regional Banking Treasury/ Other Huntington Consolidated Income Statements (Dollar amounts in thousands) Commercial AFCRE WGH... -

Page 216

... impairment charge associated with the former Regional Banking segment. The allocation of this amount to the new business segments was not practical. Assets at December 31, 2010 2009 (Dollar amounts in millions) Deposits at December 31, 2010 2009 Retail and Business Banking ...Commercial Banking... -

Page 217

... share data) Third Second First Interest income ...Interest expense ...Net interest income ...Provision for credit losses ...Noninterest income ...Noninterest expense ...Loss before income taxes...Benefit for income taxes ...Net loss ...Dividends declared on preferred shares...Net loss applicable... -

Page 218

... of Huntington's disclosure controls and procedures (as such term is defined in Rules 13a-15(e) and 15d-15(e) under the Exchange Act) as of the end of the period covered by this report. Based upon such evaluation, Huntington's Chief Executive Officer and Chief Financial Officer have concluded... -

Page 219

... Beneficial Owners and Management and Related Stockholder Matters Equity Compensation Plan Information The following table sets forth information about Huntington common stock authorized for issuance under Huntington's existing equity compensation plans as of December 31, 2010. Number of securities... -

Page 220

... stock to be issued under the following compensation plans: the Executive Deferred Compensation Plan, which provides senior officers designated by the Compensation Committee the opportunity to defer up to 90% of base salary, annual bonus compensation and certain equity awards, and up to 100% of long... -

Page 221

... Senior Executive Vice President Chief Financial Officer (Principal Financial Officer) By: /s/ David S. Anderson David S. Anderson Executive Vice President, Controller (Principal Accounting Officer) Pursuant to the requirements of the Securities Exchange Act of 1934, this report has been signed... -

Page 222

...this Annual Report on Form 10-K, information on those web sites is not part of this report. You also should be able to inspect reports, proxy statements, and other information about us at the offices of the NASDAQ National Market at 33 Whitehall Street, New York, New York. Exhibit Number SEC File or... -

Page 223

... to the 2004 Stock and Long-Term Incentive Plan * Huntington Bancshares Incorporated Employee Stock Incentive Plan (incorporating changes made by first amendment to Plan) * Second Amendment to Huntington Bancshares Incorporated Employee Stock Incentive Plan * Employment Agreement, dated January 14... -

Page 224

Exhibit Number Document Description Report or Registration Statement SEC File or Registration Number Exhibit Reference 10.30 * Performance criteria and potential awards for executive officers for fiscal year 2006 under the Management Incentive Plan and for a long-term incentive award cycle ... -

Page 225

[THIS PAGE INTENTIONALLY LEFT BLANK] -

Page 226

... Chief Executive Officer, Lancaster Colony Corporation Joined Board: 1999 D. James Hilliker Vice President / Managing Shareholder, Better Food Systems, Inc. Joined Board: 2007 David P. Lauer Certified Public Accountant Joined Board: 2003 Jonathan A. Levy(2)(5)(7) Partner, Redstone Investments Joined... -

Page 227

...South High Street, Columbus, Ohio 43215. Information Requests: Copies of Huntington's Annual Report; Forms 10-K, 10-Q, and 8-K; Financial Code of Ethics; and quarterly earnings releases may be obtained, free of charge, by calling (888) 480-3164 or by visiting Huntington's Investor Relations web site... -

Page 228

HUNTINGTON BANCSHARES INCORPORATED Huntington Center 41 South High Street Columbus, Ohio 43287 (614) 480-8300 huntington.com Member FDIC. and Huntington® are federally registered service marks of Huntington Bancshares Incorporated. Huntington Welcome.TM is a service mark of Huntington Bancshares ...