Freddie Mac 2012 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2012 Freddie Mac annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

|

|

Our charter generally prohibits us from purchasing first-lien single-family mortgages if the outstanding UPB of the

mortgage at the time of our purchase exceeds 80% of the value of the property securing the mortgage unless we have one of

the following credit protections:

• mortgage insurance from a mortgage insurer that we determine is qualified on the portion of the UPB of the mortgage

that exceeds 80%;

• a seller’s agreement to repurchase or replace any mortgage that has defaulted; or

• retention by the seller of at least a 10% participation interest in the mortgage.

Under our charter, our mortgage purchase operations are confined, so far as practicable, to mortgages that we deem to

be of such quality, type and class as to meet generally the purchase standards of other private institutional mortgage

investors. This is a general marketability standard.

Our charter requirement for credit protection on mortgages with LTV ratios greater than 80% does not apply to

multifamily mortgages or to mortgages that have the benefit of any guarantee, insurance or other obligation by the U.S. or

any of its agencies or instrumentalities (e.g., the FHA, the VA or the USDA Rural Development). Additionally, as part of

HARP, we may purchase single-family mortgages that refinance borrowers whose mortgages we currently own or guarantee

without obtaining additional credit enhancement in excess of that already in place for any such loan, even if the LTV ratio of

the new loan is above 80%.

Our Business Segments

Our operations consist of three reportable segments, which are based on the type of business activities each performs —

Single-family Guarantee, Investments, and Multifamily. Certain activities that are not part of a reportable segment are

included in the All Other category.

We evaluate segment performance and allocate resources based on a Segment Earnings approach. For more information

on our segments, including financial information, see “MD&A — CONSOLIDATED RESULTS OF OPERATIONS —

Segment Earnings” and “NOTE 13: SEGMENT REPORTING.”

Single-Family Guarantee Segment

The Single-family Guarantee segment reflects results from our single-family credit guarantee activities. In our Single-

family Guarantee segment, we purchase single-family mortgage loans originated by our seller/servicers in the primary

mortgage market. In most instances, we use the mortgage securitization process to package the mortgage loans into

guaranteed mortgage-related securities. We guarantee the payment of principal and interest on the mortgage-related security

in exchange for management and guarantee fees.

Our Customers

Our customers are predominantly lenders in the primary mortgage market that originate mortgages for homeowners.

These lenders include mortgage banking companies, commercial banks, savings banks, community banks, credit unions,

HFAs, and savings and loan associations.

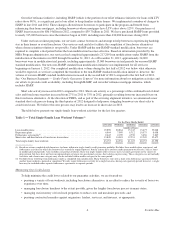

We acquire a significant portion of our mortgages from several large lenders. These lenders are among the largest

mortgage loan originators in the U.S. During 2012, three mortgage lenders, Wells Fargo Bank, N.A, U.S. Bank, N.A., and

JPMorgan Chase Bank, N.A., each accounted for 10% or more of our single-family mortgage purchase volume and

collectively accounted for approximately 49% of our single-family mortgage purchase volume. In the last two years, a

number of our largest mortgage seller/servicers have reduced or eliminated their purchases of mortgage loans from mortgage

brokers and correspondent lenders. As a result, we are acquiring an increasing portion of our business volume directly from

smaller lenders. Our top ten lenders accounted for approximately 73% and 82% of our single-family mortgage purchase

volume during 2012 and 2011, respectively.

We are the master servicer for the loans we purchase, and delegate the primary servicing function to our customers. A

significant portion of our single-family mortgage loans are serviced by several of our large customers. If our servicers lack

appropriate process controls, experience a failure in their controls, or experience an operating disruption in their ability to

service mortgage loans, our business and financial results could be adversely affected. For additional information about our

13 Freddie Mac