Freddie Mac 2012 Annual Report Download

Download and view the complete annual report

Please find the complete 2012 Freddie Mac annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

|

|

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2012

Commission File Number: 001-34139

Federal Home Loan Mortgage Corporation

(Exact name of registrant as specified in its charter)

Freddie Mac

Federally chartered 8200 Jones Branch Drive 52-0904874 (703) 903-2000

corporation McLean, Virginia 22102-3110 (I.R.S. Employer (Registrant’s telephone number,

(State or other jurisdiction of

incorporation or organization)

(Address of principal executive offices,

including zip code)

Identification No.) including area code)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

Voting Common Stock, no par value per share (OTCQB: FMCC)

Variable Rate, Non-Cumulative Preferred Stock, par value $1.00 per share (OTCQB: FMCCI)

5% Non-Cumulative Preferred Stock, par value $1.00 per share (OTCQB: FMCKK)

Variable Rate, Non-Cumulative Preferred Stock, par value $1.00 per share (OTCQB: FMCCG)

5.1% Non-Cumulative Preferred Stock, par value $1.00 per share (OTCQB: FMCCH)

5.79% Non-Cumulative Preferred Stock, par value $1.00 per share (OTCQB: FMCCK)

Variable Rate, Non-Cumulative Preferred Stock, par value $1.00 per share (OTCQB: FMCCL)

Variable Rate, Non-Cumulative Preferred Stock, par value $1.00 per share (OTCQB: FMCCM)

Variable Rate, Non-Cumulative Preferred Stock, par value $1.00 per share (OTCQB: FMCCN)

5.81% Non-Cumulative Preferred Stock, par value $1.00 per share (OTCQB: FMCCO)

6% Non-Cumulative Preferred Stock, par value $1.00 per share (OTCQB: FMCCP)

Variable Rate, Non-Cumulative Preferred Stock, par value $1.00 per share (OTCQB: FMCCJ)

5.7% Non-Cumulative Preferred Stock, par value $1.00 per share (OTCQB: FMCKP)

Variable Rate, Non-Cumulative Perpetual Preferred Stock, par value $1.00 per share (OTCQB: FMCCS)

6.42% Non-Cumulative Perpetual Preferred Stock, par value $1.00 per share (OTCQB: FMCCT)

5.9% Non-Cumulative Perpetual Preferred Stock, par value $1.00 per share (OTCQB: FMCKO)

5.57% Non-Cumulative Perpetual Preferred Stock, par value $1.00 per share (OTCQB: FMCKM)

5.66% Non-Cumulative Perpetual Preferred Stock, par value $1.00 per share (OTCQB: FMCKN)

6.02% Non-Cumulative Perpetual Preferred Stock, par value $1.00 per share (OTCQB: FMCKL)

6.55% Non-Cumulative Perpetual Preferred Stock, par value $1.00 per share (OTCQB: FMCKI)

Fixed-to-Floating Rate Non-Cumulative Perpetual Preferred Stock, par value $1.00 per share (OTCQB: FMCKJ)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934

during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing

requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required

to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that

the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best

of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this

Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the

definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer [ ] Accelerated filer [X]

Non-accelerated filer (Do not check if a smaller reporting company) [ ] Smaller reporting company [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

The aggregate market value of the common stock held by non-affiliates computed by reference to the price at which the common equity was last sold on

June 29, 2012 (the last business day of the registrant’s most recently completed second fiscal quarter) was $162.5 million.

As of February 15, 2013, there were 650,038,674 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE: None

Table of contents

-

Page 1

... Federal Home Loan Mortgage Corporation (Exact name of registrant as specified in its charter) Freddie Mac Federally chartered corporation (State or other jurisdiction of incorporation or organization) 8200 Jones Branch Drive McLean, Virginia 22102-3110 (Address of principal executive offices... -

Page 2

... and Analysis ...Off-Balance Sheet Arrangements ...Contractual Obligations ...Critical Accounting Policies and Estimates ...Risk Management and Disclosure Commitments ...Quantitative and Qualitative Disclosures About Market Risk ...Financial Statements and Supplementary Data ...Changes in and... -

Page 3

..., Single-Family Credit Guarantee Portfolio ...Mortgage-Related Investments Portfolio ...Affordable Housing Goals for 2012 to 2014 ...Affordable Housing Goals and Results for 2010 and 2011 ...Quarterly Common Stock Information ...Mortgage Market Indicators ...Summary Consolidated Statements of... -

Page 4

... Reserve Recorded ...Single-Family Credit Loss Sensitivity ...Repurchase Request Activity and Counterparty Balances ...Loans Released from Repurchase Obligations ...Mortgage Insurance by Counterparty ...Bond Insurance by Counterparty ...Derivative Counterparty Credit Exposure ...Other Debt Security... -

Page 5

... and Related Matters ...Note 3: Variable Interest Entities ...Note 4: Mortgage Loans and Loan Loss Reserves ...Note 5: Individually Impaired and Non-Performing Loans . Note 6: Real Estate Owned ...Note 7: Investments in Securities ...Note 8: Debt Securities and Subordinated Borrowings ...Note... -

Page 6

... to our profitability. Some of these changes increase our expenses, while others require us to forego revenue opportunities. On February 21, 2012, FHFA sent to Congress a strategic plan for the next phase of the conservatorships of Freddie Mac and Fannie Mae. FHFA stated that the steps envisioned in... -

Page 7

... have on borrowers and the housing market. The report states that the government is committed to ensuring that Freddie Mac and Fannie Mae have sufficient capital to perform under any guarantees issued now or in the future and the ability to meet any of their debt obligations, and further states that... -

Page 8

... in UPB of single-family conforming mortgage loans, representing approximately 2.0 million and 1.5 million homes, respectively. Borrowers typically pay a lower interest rate on loans acquired or guaranteed by Freddie Mac, Fannie Mae, or Ginnie Mae. Mortgage originators are able to offer homebuyers... -

Page 9

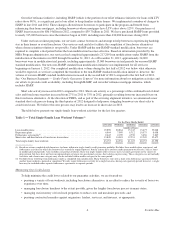

...quarters. Table 1 - Total Single-Family Loan Workout Volumes(1) 12/31/2012 For the Three Months Ended 09/30/2012 06/30/2012 03/31/2012 (number of loans) 12/31/2011 Loan modifications ...Repayment plans ...Forbearance agreements(2) ...Short sales and deed in lieu of foreclosure transactions ...Total... -

Page 10

... our credit losses. We require our single-family seller/servicers to first evaluate problem loans for a repayment or forbearance plan before considering modification. If a borrower is not eligible for a modification, our seller/servicers pursue foreclosure alternatives (e.g., short sales) before... -

Page 11

... claims paying obligations to us as those claims emerge. See "NOTE 4: MORTGAGE LOANS AND LOAN LOSS RESERVES - Table 4.5 - Recourse and Other Forms of Credit Protection" for information about credit enhancements of our single-family credit guarantee portfolio. Developing Mortgage Market Enhancements... -

Page 12

... the borrowers' potential to make their mortgage payments. Relief refinance mortgages of all LTV ratios comprised approximately 18% and 11% of the UPB in our total single-family credit guarantee portfolio at December 31, 2012 and 2011, respectively. HARP loans represented 11% and 6% of the UPB of... -

Page 13

...the aggregate UPB of loans with LTV ratios greater than 100% in relation to the total UPB of loans in the category. (5) See "RISK MANAGEMENT - Credit Risk - Mortgage Credit Risk - Single-family Mortgage Credit Risk - Delinquencies" for further information about our reported serious delinquency rates... -

Page 14

...new loan purchase and guarantee activity. We believe this is due, in part, to declines in the amount of single-family mortgage debt outstanding in the market and a decline in our single-family competitive position compared to other market participants (primarily Fannie Mae and Ginnie Mae). See "RISK... -

Page 15

...Family Mortgage Credit Risk - Delinquencies" for further information about our reported serious delinquency rates. (2) Consists of the UPB of loans in our single-family credit guarantee portfolio that have undergone a TDR or that are seriously delinquent. During the third quarter of 2012, we changed... -

Page 16

...statistics. See "MD&A - RISK MANAGEMENT - Credit Risk - Mortgage Credit Risk - Single-family Mortgage Credit Risk - Credit Performance - Delinquencies" for further information about factors affecting our reported delinquency rates. Consolidated Financial Results - 2012 versus 2011 Net income was $11... -

Page 17

...including changes in interest rates, home ownership rates, home prices, the supply of housing and lender preferences regarding credit risk and borrower preferences regarding mortgage debt. The amount of residential mortgage debt available for us to purchase and the mix of available loan products are... -

Page 18

..., we purchase single-family mortgage loans originated by our seller/servicers in the primary mortgage market. In most instances, we use the mortgage securitization process to package the mortgage loans into guaranteed mortgage-related securities. We guarantee the payment of principal and interest... -

Page 19

... - Credit Risk - Institutional Credit Risk - Single-Family Mortgage Seller/Servicers." Our Competition Historically, our principal competitors have been Fannie Mae, Ginnie Mae and FHA/VA, and other financial institutions that retain or securitize mortgages, such as commercial and investment banks... -

Page 20

... and sell the home. The terms of single-family mortgages that we purchase or guarantee allow borrowers to prepay these loans, thereby allowing borrowers to refinance their loans when mortgage rates decline. Because of the nature of long-term, fixed-rate mortgages, borrowers with these mortgages are... -

Page 21

... delivery fees charged on single-family mortgages in states where costs related to foreclosures are statistically higher than the national average. FHFA stated in its September 2012 announcement that it expects to direct us and Fannie Mae to implement the pricing adjustments in 2013. 16 Freddie Mac -

Page 22

...our mortgage-related investments portfolio, as it is generally easier to purchase and sell PCs than unsecuritized mortgage loans, and allows more cost effective interest-rate risk management. For our fixed-rate PCs, we guarantee the timely payment of principal and interest. For our single-family ARM... -

Page 23

... pension funds, insurance companies, securities dealers, money managers, REITs, and commercial banks, purchase our PCs. For the past several years, the Federal Reserve has purchased significant amounts of mortgage-related securities issued by us, Fannie Mae and Ginnie Mae. These purchases, which... -

Page 24

... sell us mortgage-related assets or we use our own mortgage-related assets (e.g., PCs and REMICs and Other Structured Securities) in exchange for the REMICs and Other Structured Securities. The creation of REMICs and Other Structured Securities allows for setting differing terms for specific classes... -

Page 25

... the principal and interest payments on those certificates. In this type of transaction, our credit risk is reduced by the structural credit protections from the related subordinated tranches, which we do not guarantee. In the second type, we purchase single-class pass-through securities, place... -

Page 26

...the loans are evaluated using a number of critical risk characteristics, including, but not limited to, the borrower's credit score and credit history, the borrower's monthly income relative to debt payments (or DTI), the original LTV ratio, the type of mortgage product, the property type and market... -

Page 27

...future sales of mortgage loans to Freddie Mac and Fannie Mae and, under this new framework, lenders will be relieved of certain repurchase obligations for loans that meet specific payment requirements. Examples, subject to certain exclusions, include: • loans with 36 months of consecutive, on-time... -

Page 28

... affect their obligation to service these loans in accordance with our servicing standards. Freddie Mac will continue to work with lenders to resolve contractual claims on loans delivered prior to January 1, 2013. Credit Enhancements Our charter requires that single-family mortgages with LTV ratios... -

Page 29

...the housing market. Through our participation in this program, we help borrowers maintain home ownership. Some of the key initiatives of this program include HAMP and HARP, which are discussed below. Home Affordable Modification Program HAMP commits U.S. government, Freddie Mac, and Fannie Mae funds... -

Page 30

... FHFA, Freddie Mac, and Fannie Mae announced a series of FHFA-directed changes to HARP, in an effort to attract more eligible borrowers who can benefit from refinancing their home mortgages. We subsequently made similar changes to the relief refinance mortgage initiative for loans with LTV ratios of... -

Page 31

...-family Mortgage Credit Risk - Single-Family Loan Workouts and the MHA Program" for additional information about HARP and our relief refinance mortgage initiative. Non-HAMP Standard Modifications In late 2011, as part of the servicing alignment initiative (described below), we implemented a new... -

Page 32

... loans related to our single-family business. For our liquidity needs, we maintain a portfolio comprised primarily of cash and cash equivalents, non-mortgage-related securities (primarily Treasury securities), and securities purchased under agreements to resell. Debt Financing We fund our investment... -

Page 33

...in guarantor swap transactions. We also issue PCs backed by mortgage loans that we purchased for cash. The relative price performance of our PCs and comparable Fannie Mae securities can directly affect the volume and/or profitability of our new single-family guarantee business. From time to time, we... -

Page 34

... to purchase, repurchases have been rare. We generally require multifamily seller/servicers to service mortgage loans they have sold to us in order to mitigate potential losses. This includes property monitoring tasks beyond those typically performed by single-family servicers. We 29 Freddie Mac -

Page 35

... and FHFA regarding Freddie Mac and Fannie Mae. These actions included the execution of the Purchase Agreement, pursuant to which we issued to Treasury both senior preferred stock and a warrant to purchase common stock. At that time, FHFA set forth the purpose and goals of the conservatorship... -

Page 36

... and our Conservator have placed on Freddie Mac in addressing housing and mortgage market conditions and our public mission, we may be required to take additional actions that could have a negative impact on our business, operating results or financial condition, and thus could contribute to a need... -

Page 37

...housing and financial markets. This strategy is designed to reduce the portfolio and provide the best return to the taxpayer while minimizing market disruption. The table below presents the UPB of our mortgage-related investments portfolio, for purposes of the limit imposed by the Purchase Agreement... -

Page 38

... Conservator is required to maintain a full accounting of the conservatorship and make its reports available upon request to stockholders and members of the public. We remain liable for all of our obligations relating to our outstanding debt and mortgage-related securities. FHFA has stated that our... -

Page 39

... reduction in our net worth during 2010, 2011, and 2012) in funds to us under the terms and conditions set forth in the Purchase Agreement. Beginning January 1, 2013, the amount of available funding remaining under the Purchase Agreement is $140.5 billion. This amount will be reduced by any future... -

Page 40

..., the holders of these debt securities or Freddie Mac mortgage guarantee obligations may file a claim in the United States Court of Federal Claims for relief requiring Treasury to fund to us the lesser of: (a) the amount necessary to cure the payment defaults on our debt and Freddie Mac mortgage... -

Page 41

... by our Board of Directors. Through December 31, 2012, the senior preferred stock accrued quarterly cumulative dividends at a rate of 10% per year. However, under the August 2012 amendment to the Purchase Agreement, the fixed dividend rate was replaced with a net worth sweep dividend beginning in... -

Page 42

... other executive officer (as such terms are defined by SEC rules) without the consent of the Director of FHFA, in consultation with the Secretary of the Treasury. The Purchase Agreement also provides that, on an annual basis, we are required to deliver a risk management plan to Treasury setting out... -

Page 43

...a five-year term, removable only for cause. In the discussion below, we refer to Freddie Mac and Fannie Mae as the "enterprises." The Federal Housing Finance Oversight Board, or the Oversight Board, is responsible for advising the Director of FHFA with respect to overall strategies and policies. The... -

Page 44

... "NOTE 14: REGULATORY CAPITAL." Also, see "RISK FACTORS - Legal and Regulatory Risks" for more information. New Products The GSE Act requires the enterprises to obtain the approval of FHFA before initially offering any product, subject to certain exceptions. The GSE Act provides for a public comment... -

Page 45

... data relating to our mortgage purchases, information or reports as required by law. See "RISK FACTORS - Legal and Regulatory Risks - We may make certain changes to our business in an attempt to meet our housing goals and subgoals." FHFA has established four goals and one subgoal for single-family... -

Page 46

... plans for goals that we did not achieve in 2010 or 2011. Affordable Housing Allocations The GSE Act requires us to set aside in each fiscal year an amount equal to 4.2 basis points for each dollar of the UPB of total new business purchases, and allocate or transfer such amount to: (a) HUD to fund... -

Page 47

..., and reporting and disclosure of Freddie Mac subordinated debt have been suspended during the term of conservatorship and thereafter until directed otherwise. See "NOTE 14: REGULATORY CAPITAL - Subordinated Debt Commitment" for more information regarding subordinated debt. Department of Housing and... -

Page 48

...help bring private capital back to the mortgage market, including increasing guarantee fees, phasing in a 10% down payment requirement, reducing conforming loan limits, and winding down Freddie Mac and Fannie Mae's investment portfolios, consistent with the senior preferred stock purchase agreements... -

Page 49

...These changes align our and Fannie Mae's requirements in these areas. The second goal describes steps that FHFA plans to take to gradually shift mortgage credit risk from Freddie Mac and Fannie Mae to private investors and eliminate the direct funding of mortgages by the enterprises. The plan states... -

Page 50

...the rate of foreclosures generally and result in significant changes to mortgage servicing and foreclosure practices that could adversely affect our business. Mortgage originators and assignees, including Freddie Mac, may be subject to increased legal risk for loans that do not meet the requirements... -

Page 51

... information on operational risks related to these developments in mortgage servicing, see "MD&A - RISK MANAGEMENT - Operational Risks." FHFA Advisory Bulletin On April 9, 2012, FHFA issued an advisory bulletin, "Framework for Adversely Classifying Loans, Other Real Estate Owned, and Other Assets... -

Page 52

... programs to assist the U.S. residential mortgage market, future business plans, liquidity, capital management, economic and market conditions and trends, market share, the effect of legislative and regulatory developments, implementation of new accounting guidance, credit losses, internal control... -

Page 53

..., HARP, the non-HAMP standard loan modification initiative, and the new short sale initiative), and the effect of such programs on our credit losses, expenses, and the size and composition of our mortgage-related investments portfolio; • the effect of any deficiencies in foreclosure documentation... -

Page 54

... initiative), our practices with respect to the disposition of REO properties, or investment standards for mortgage-related products; • investor preferences for mortgage loans and mortgage-related and debt securities compared to other investments; • borrower preferences for fixed-rate mortgages... -

Page 55

...the companies). FHFA is driving significant changes in our business model, primarily in our single-family guarantee business, through its strategic plan for Freddie Mac and Fannie Mae and the Conservatorship Scorecard. At the time FHFA released its strategic plan, it stated that the steps envisioned... -

Page 56

... adverse changes in our funding costs or limitations in our access to public debt markets; • changes in accounting practices or guidance; • effects of the MHA Program and other government initiatives, including any future requirements to reduce the principal amount of loans; • losses resulting... -

Page 57

..., our portfolio growth, net worth, credit losses, net interest income, guarantee fee income, net deferred tax assets, loan loss reserves, and future results of operations and financial condition, and thus could contribute to a need for additional draws under the Purchase Agreement. In light of the... -

Page 58

... and standardizing certain mortgage data requirements; (b) aligning certain terms of the contracts we and Fannie Mae use with our respective single-family seller/servicers, as well as certain practices we follow in managing our remedies and our respective business relationships with these companies... -

Page 59

...Purchase Agreement to address a deficit in our net worth, and Treasury is unable to provide us with such funding within the 60-day period specified by FHFA, FHFA would be required to place us into receivership if our assets remain less than our obligations during that 60-day period. 54 Freddie Mac -

Page 60

.... • Our future profits will effectively be distributed to Treasury. Under the Purchase Agreement, we are required to pay dividends to the extent that our Net Worth Amount exceeds a permitted capital reserve amount. The amount of this reserve decreases over time. Accordingly, over the long-term, we... -

Page 61

... sell mortgage assets. Under the terms of the Purchase Agreement and FHFA regulation, our mortgage-related investments portfolio is subject to a cap that decreases each year until the portfolio reaches $250 billion. As a result of the August 2012 amendment to the Purchase Agreement, the annual rate... -

Page 62

... type, the type of property securing the mortgage, the LTV ratio of the loan, and local and regional economic conditions, including home prices and unemployment rates. Our credit losses will remain elevated for the near term due to the substantial number of mortgage loans in our single-family credit... -

Page 63

... subprime, option ARM, and Alt-A loans due to poor performance of the underlying mortgages. The financial condition of bond insurers also continued to deteriorate in 2012. See "MD&A - CONSOLIDATED BALANCE SHEETS ANALYSIS - Investments in Securities" for information about the credit ratings for these... -

Page 64

... impact of our relief refinance initiatives. However, originations of refinance mortgages will likely decline if HARP expires as currently scheduled in December 2013. Interest rates have been at historically low levels for an extended period of time. In addition, many eligible borrowers have already... -

Page 65

... counterparty risk are with: • mortgage seller/servicers; • mortgage insurers; • issuers, guarantors or third-party providers of other credit enhancements (including bond insurers); • counterparties to short-term lending and other investment-related agreements and cash equivalent... -

Page 66

... loan is insured) and the risk that we will incur credit losses on the loan through the workout or foreclosure process. As of December 31, 2012 and 2011, the UPB of loans subject to repurchase requests based on breaches of representations and warranties issued to our single-family seller/servicers... -

Page 67

... RISK MANAGEMENT - Credit Risk - Mortgage Credit Risk - Single-Family Mortgage Credit Risk - Single-Family Loan Workouts and the MHA Program - Relief Refinance Mortgage Initiative and the Home Affordable Refinance Program." We also have exposure to seller/servicers with respect to mortgage insurance... -

Page 68

... See "MD&A - RISK MANAGEMENT - Credit Risk - Institutional Credit Risk - Single-family Mortgage Seller/ Servicers" and "- Multifamily Mortgage Seller/Servicers" for additional information on our institutional credit risk related to our mortgage seller/servicers. Our financial condition or results of... -

Page 69

... LTV ratios greater than 90% increased during 2012 compared to 2011, in part because most mortgage insurance companies lowered their premiums in 2011 for certain higher-risk loans. For more information, see "MD&A - RISK MANAGEMENT - Credit Risk - Mortgage Credit Risk - Single-Family Mortgage Credit... -

Page 70

... of all claims in the future. See "NOTE 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - Allowance for Loan Losses and Reserve for Guarantee Losses - Single-Family Loans" for more information. The loss of business volume from key mortgage originators could result in a decline in our market share and... -

Page 71

... credit standards or raising guarantee fees, could cause our market share to decrease and the volume of our single-family guarantee business to decline. Historically, we also competed with other financial institutions that retain or securitize mortgages, such as commercial and investment banks... -

Page 72

... business activities and meet our obligations could have an adverse effect on our business, liquidity, financial condition, and results of operations. See "MD&A - LIQUIDITY AND CAPITAL RESOURCES - Liquidity - Other Debt Securities" for a description of our debt issuance programs. Our funding costs... -

Page 73

..., changes in government support for us, future GAAP losses, and additional draws under the Purchase Agreement. Any such downgrades could lead to major disruptions in the mortgage market and to our business due to lower liquidity, higher borrowing costs, lower asset values, and higher credit losses... -

Page 74

...investment activities and credit guarantee activities expose us to interest rate and other market risks. Changes in interest rates, up or down, could adversely affect our net interest yield. Although the yield we earn on our assets and our funding costs tend to move in the same direction in response... -

Page 75

... borrowers to refinance into a fixed-rate loan. Interest rates can fluctuate for a number of reasons, including changes in the fiscal and monetary policies of the federal government and its agencies, such as the Federal Reserve. Federal Reserve policies directly and indirectly influence the yield... -

Page 76

... net interest yields over time on other mortgage-related investments. The ultimate impact of the HARP revisions on our financial results will be driven by the level of borrower participation and the volume of loans with high LTV ratios that we acquire under the program. Over time, relief refinance... -

Page 77

... further write-downs and losses relating to our assets, including our investment securities, net deferred tax assets, REO properties or mortgage loans, that could materially adversely affect our business, results of operations, financial condition, liquidity and net worth. We experienced significant... -

Page 78

... servicers from completing foreclosures within required timelines defined by mortgage insurers. Mortgage insurance companies establish foreclosure timelines that vary by state and range between 60 and 990 days. Delays in the foreclosure process could create fluctuations in our single-family credit... -

Page 79

... of newly established controls; (f) data quality or servicing-related issues; and (g) the uncertain long-term impacts of the recent housing and economic downturn on the results of our models, which are used for financial accounting and reporting purposes. Disruptive levels of employee turnover could... -

Page 80

... risk that we could make poor business decisions in areas where model results are an important factor, including loan purchases, management and guarantee fee pricing, asset and liability management, market risk management, and quality-control sampling strategies for loans in our single-family credit... -

Page 81

...from our current methods of accounting for single-family loans that are 180 days or more delinquent. For more information, see "BUSINESS - Regulation and Supervision - Legislative and Regulatory Developments - FHFA Advisory Bulletin." See "NOTE 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES" for more... -

Page 82

...technology and other projects, and erode our business, modeling, internal audit, risk management, information security, financial reporting, legal, compliance, and other capabilities. Internal reorganizations could have a similar effect. Any such event could add to the risk of operational or control... -

Page 83

...to other non-bank financial companies. New prudential standards could include requirements related to risk-based capital and leverage, liquidity, single-counterparty credit limits, overall risk management and risk committees, stress tests, and debt-to-equity limits, among other requirements. • The... -

Page 84

... Real Estate Transfer Taxes." Pursuant to the Temporary Payroll Tax Cut Continuation Act of 2011, FHFA required Freddie Mac and Fannie Mae to increase guarantee fees by no less than 10 basis points above the average guarantee fees charged in 2011 on single-family mortgage-backed securities to fund... -

Page 85

... legal proceedings. ITEM 4. MINE SAFETY DISCLOSURES Not applicable. PART II ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES Market Information Our common stock, par value $0.00 per share, trades on the OTCQB Marketplace, operated... -

Page 86

... of the Director of FHFA is required for any dividend payment; the Director may approve a capital distribution only if the Director determines that the distribution will enhance the ability of the company to meet required capital levels promptly, will contribute to the long-term financial safety-and... -

Page 87

...pay dividends on any other series of preferred stock outstanding in 2012. Recent Sales of Unregistered Securities The securities we issue are "exempted securities" under the Securities Act of 1933, as amended. As a result, we do not file registration statements with the SEC with respect to offerings... -

Page 88

...diluted ...Cash dividends per common share ...Weighted average common shares outstanding (in thousands) - basic and diluted(3) ...Balance Sheets Data Mortgage loans held-for-investment, at amortized cost by consolidated trusts (net of allowances for loan losses) ...Total assets ...Debt securities of... -

Page 89

... changes in single-family home prices by state, which are weighted using the property values underlying our single-family credit guarantee portfolio to obtain a national index. The rate for each year presented incorporates property value information on loans purchased by both Freddie Mac and Fannie... -

Page 90

...debt was driven by increasing sales of new and existing single-family homes during this same period. As reported by FHFA in its Conservator's Report on the Enterprises' Financial Condition, dated June 13, 2011, the market share of mortgage-backed securities issued by the GSEs and Ginnie Mae declined... -

Page 91

... interest rates on fixed-rate single-family mortgages. For information on the HARP initiative, see "RISK MANAGEMENT - Credit Risk - Mortgage Credit Risk - Single-Family Mortgage Credit Risk - Single-Family Loan Workouts and the MHA Program." While home prices remained at significantly lower levels... -

Page 92

... net of taxes and reclassification adjustments: Changes in unrealized gains (losses) related to available-for-sale securities ...Changes in unrealized gains (losses) related to cash flow hedge relationships ...Changes in defined benefit plans ...Total other comprehensive income (loss), net of taxes... -

Page 93

... Change (in millions) Interest-earning assets: Cash and cash equivalents ...Federal funds sold and securities purchased under agreements to resell ...Mortgage-related securities: Mortgage-related securities (3) ...Extinguishment of PCs held by Freddie Mac ...Total mortgage-related securities, net... -

Page 94

...by 15% each year until the portfolio reaches $250 billion. This decline in asset balances will cause a reduction in our interest income over time. For more information on the various restrictions and limitations on our investment activity and our mortgage-related investments portfolio, see "BUSINESS... -

Page 95

... life of the loan regardless of the payment status. See "RISK MANAGEMENT - Credit Risk - Mortgage Credit Risk" for further information on our single-family credit guarantee portfolio, including credit performance, serious delinquency rates, charge-offs, our loan loss reserves balance, and our non... -

Page 96

...funding our assets. When we repurchase or call outstanding debt securities, or holders put outstanding debt securities to us, we recognize a gain or loss to the extent the amount paid to redeem the debt security differs from its carrying value. See "NOTE 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES... -

Page 97

... adjust the interest-rate characteristics of our debt in response to changes in the expected lives of our investments in mortgage-related assets. Purchased call and put swaptions, where we make premium payments, are options for us to enter into receive- and pay-fixed swaps, respectively. Conversely... -

Page 98

...these securities. For information concerning the estimated impact this enhancement would have had on our net income, as of the beginning of the fourth quarter of 2012, see "NOTE 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - Change in Estimate - Other-Than-Temporary Impairments of Single-Family Non... -

Page 99

... on loans impaired upon purchase declined in both 2012 and 2011, compared to the prior year, due to a lower volume of foreclosure transfers and payoffs associated with loans impaired upon purchase. Commencing January 1, 2010, we no longer recognize losses on loans purchased from PC pools related to... -

Page 100

...(a) income recognized in 2011 related to proceeds received from an agreement with Bank of America with respect to repurchase obligations; and (b) income recognized in 2011 related to a settlement with Taylor, Bean & Whitaker (TBW), one of our former seller/servicers. The decline in 2011, compared to... -

Page 101

... REO activity to remain at elevated levels, as we have a large inventory of seriously delinquent loans in our single-family credit guarantee portfolio. See "RISK MANAGEMENT - Credit Risk - Mortgage Credit Risk - Non-Performing Assets" for additional information about our REO activity. Other Expenses... -

Page 102

..., we purchase single-family mortgage loans originated by our seller/servicers in the primary mortgage market. In most instances, we use the mortgage securitization process to package the purchased mortgage loans into guaranteed mortgage-related securities. We guarantee the payment of principal and... -

Page 103

...by: (a) reclassifying certain investment-related activities and credit guarantee-related activities between various line items on our GAAP consolidated statements of comprehensive income; and (b) allocating certain revenues and expenses, including certain returns on assets and funding costs, and all... -

Page 104

... the Investments segment's mortgage investments portfolio. (3) The balances of the mortgage-related securities in the Single-family Guarantee managed loan portfolio are based on the UPB of the security, whereas the balances of our single-family credit guarantee portfolio presented in this report are... -

Page 105

... balances of interest-earning cash and cash equivalents, non-mortgage-related securities, and federal funds sold and securities purchased under agreements to resell. (7) Excludes unsecuritized seriously delinquent single-family mortgage loans. 2012 vs. 2011 Segment Earnings for our Investments... -

Page 106

...these securities. The decline in the UPB of single-family unsecuritized mortgage loans is primarily related to our securitization of mortgage loans that we had purchased for cash. See "CONSOLIDATED BALANCE SHEETS ANALYSIS - Investments in Securities" and "- Mortgage Loans" for additional information... -

Page 107

... to 2010. For a discussion of items that have affected our Investments segment net interest income over time, and will likely continue to do so, see "BUSINESS - Conservatorship and Related Matters - Limits on Investment Activity and Our Mortgage-Related Investments Portfolio." 102 Freddie Mac -

Page 108

... balance of our single-family HFA initiative guarantees. (9) Source: Federal Reserve Flow of Funds Accounts of the United States of America dated December 6, 2012. The outstanding amount for December 31, 2012 reflects the balance as of September 30, 2012. (10) Based on Freddie Mac's Primary Mortgage... -

Page 109

... unemployment rates, future declines in home prices, or negative impacts of HARP loans (which may not perform as well as other refinance mortgages, due in part to the high LTV ratios of the loans), could require us to incur expenses on these loans beyond our current expectations. 104 Freddie Mac -

Page 110

... 82% of our single-family mortgage purchase volume in 2012, compared to 78% in 2011, based on UPB. We purchased significant volumes of relief refinance mortgages and HARP loans (i.e., relief refinance loans with LTV ratios above 80%) in both 2012 and 2011. Over time, HARP loans may not perform as... -

Page 111

... UPB over 80%. Approximately 20% and 12% of our single-family purchase volume in 2012 and 2011, respectively, were HARP loans. For more information about HARP loans and our relief refinance mortgage initiative, see "RISK MANAGEMENT - Credit Risk - Mortgage Credit Risk - Single-Family Mortgage Credit... -

Page 112

... the amount of recoveries on loans impaired upon purchase since the volume of foreclosure transfers and payoffs associated with loans impaired upon purchase also declined in 2011. Other non-interest expense for the Single-family Guarantee segment was $0.4 billion in 2012, compared to $0.3 billion in... -

Page 113

...Rate: Net interest yield - Segment Earnings basis ...Average Management and guarantee fee rate, in bps(4) ...Credit: Delinquency rate: Credit-enhanced loans, at period end ...Non-credit-enhanced loans, at period end ...Total delinquency rate, at period end(5) ...Allowance for loan losses and reserve... -

Page 114

...loans on our consolidated balance sheets during both 2012 and 2011 resulted in higher total gains in those years compared to the respective prior year. Segment Earnings gains (losses) on mortgage loans recorded at fair value are presented net of changes in fair value due to changes in interest rates... -

Page 115

... help manage recurring cash flows and meet our other cash management needs. We consider federal funds sold to be overnight unsecured trades executed with commercial banks that are members of the Federal Reserve System. Securities purchased under agreements to resell principally consist of short-term... -

Page 116

... 31, 2012 Available-for-sale mortgage-related securities: Freddie Mac ...Fannie Mae ...Ginnie Mae ...CMBS ...Subprime ...Option ARM ...Alt-A and other ...Obligations of states and political subdivisions ...Manufactured housing ...Total investments in available-for-sale mortgage-related securities... -

Page 117

... Trading mortgage-related securities: Freddie Mac ...Fannie Mae ...Ginnie Mae ...Other ...Total trading mortgage-related securities ...Trading non-mortgage-related securities: Asset-backed securities ...Treasury bills ...Treasury notes ...FDIC-guaranteed corporate medium-term notes ...Total trading... -

Page 118

...-related securities: Single-family:(4) Subprime ...Option ARM ...Alt-A and other ...CMBS ...Obligations of states and political subdivisions(5) ...Manufactured housing ...Total non-agency mortgage-related securities(6) ...Total UPB of mortgage-related securities ...Premiums, discounts, deferred fees... -

Page 119

... Structured Securities. See "GLOSSARY" for more information on these securities. (6) Includes fair values of $3 million and $2 million of interest-only securities at December 31, 2012 and 2011, respectively. The total UPB of our investments in mortgage-related securities on our consolidated balance... -

Page 120

... and Market Risks - A significant decline in the price performance of or demand for our PCs could have an adverse effect on the volume and/or profitability of our new single-family guarantee business." Unrealized Losses on Available-For-Sale Mortgage-Related Securities At December 31, 2012, our... -

Page 121

... more information on single-family loans with certain higher-risk characteristics underlying our issued securities, see "RISK MANAGEMENT - Credit Risk - Mortgage Credit Risk." Non-Agency Mortgage-Related Securities Backed by Subprime, Option ARM, and Alt-A Loans We categorize our investments in non... -

Page 122

... fourth quarter of 2012, of a third-party model, which enhanced our approach to estimating other-than-temporary impairments of our singlefamily non-agency mortgage-related securities. For more information regarding our implementation of this model, see "NOTE 7: INVESTMENTS IN SECURITIES - Impairment... -

Page 123

...on bond insurance coverage, see "RISK MANAGEMENT - Credit Risk - Institutional Credit Risk - Bond Insurers." The table below provides principal repayment and cash shortfall information for our investments in non-agency mortgage-related securities backed by subprime, option ARM, Alt-A and other loans... -

Page 124

..., option ARM, and Alt-A and other loans. Economic factors negatively impacting the performance of our investments in non-agency mortgage-related securities since 2007 include high unemployment, a large inventory of seriously delinquent mortgage loans and unsold homes, tight credit conditions, and... -

Page 125

... changes in interest rates may also affect our losses due to the structural credit enhancements on our investments in non-agency mortgage-related securities. The lengthening of the foreclosure timelines that has occurred in recent years can also affect our losses. For example, while defaulted loans... -

Page 126

... Mortgage-Related Securities Backed by Subprime, Option ARM, Alt-A and Other Loans, and CMBS Credit Ratings as of December 31, 2012 UPB Gross Percentage Amortized Unrealized of UPB Cost Losses (dollars in millions) Bond Insurance Coverage (1) Subprime loans: AAA-rated ...Other investment grade... -

Page 127

... total mortgage portfolio, excluding non-Freddie Mac securities, were 1.7% and 2.1%, respectively, and as a percentage of the UPB associated with our nonperforming loans were 23.5% and 32.0%, respectively. Our loan loss reserves declined during 2012 primarily due to continued high levels of charge... -

Page 128

... with mortgage loans. See endnote (5) for further information. (2) Includes amortizing ARMs with 1-, 3-, 5-, 7-, and 10-year initial fixed-rate periods. We did not purchase any option ARM loans during the years ended December 31, 2012, 2011, or 2010. (3) Represents loans where the borrower pays... -

Page 129

... Credit Exposure" for information about non-cash collateral held or posted. (4) Represents the notional weighted average rate for the fixed leg of the swaps. (5) Represents interest-rate swap agreements that are scheduled to begin on future dates ranging from less than one year to thirteen years... -

Page 130

... remain at elevated levels, as we have a large inventory of seriously delinquent loans in our single-family credit guarantee portfolio. See "RISK MANAGEMENT - Credit Risk - Mortgage Credit Risk - Non-Performing Assets" for additional information about our REO activity. Deferred Tax Assets, Net After... -

Page 131

... of the Par Value and UPB to Total Debt, Net December 31, 2012 2011 (in millions) Total debt: Other debt: ...Par value ...Unamortized balance of discounts and premiums(1) ...Hedging-related and other basis adjustments(2) ...Subtotal ...Debt securities of consolidated trusts held by third... -

Page 132

... Average (3) Balance, Net Effective Rate(4) (dollars in millions) Maximum Balance, Net Outstanding at Any Month End Reference Bills® securities and discount notes ...Medium-term notes ...Federal funds purchased and securities sold under agreements to repurchase ...Other short-term debt ... $161... -

Page 133

... Single-family ...Multifamily ...Total HFA bonds ...Total Other Guarantee Transactions ...REMICs and Other Structured Securities backed by Ginnie Mae certificates (6) ...Total Freddie Mac Mortgage-Related Securities ...Less: Repurchased Freddie Mac Mortgage-Related Securities(7) ...Total UPB of debt... -

Page 134

...of Debt Securities of Consolidated Trusts," extinguishments, net for 2012 include $4.4 billion related to the consolidation of these REMIC trusts related to the correction of the error. See "NOTE 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - Basis of Presentation" for more information. 129 Freddie... -

Page 135

...-for-sale securities ...Changes in unrealized gains (losses) related to cash flow hedge relationships ...Changes in defined benefit plans ...Comprehensive income ...Capital draw funded by Treasury ...Senior preferred stock dividends declared ...Other ...Total equity (deficit)/Net worth ...Aggregate... -

Page 136

... to debt payments), documentation level, the number of borrowers, the features of the mortgage itself, the purpose of the mortgage, occupancy type, property type and value, the LTV ratio, and local and regional economic conditions, including home prices and unemployment rates. We use a process of... -

Page 137

... "BUSINESS - Our Business Segments - Single-Family Guarantee Segment - Underwriting Requirements and Quality Control Standards." We were significantly adversely affected by deteriorating conditions in the single-family housing and mortgage markets during 2008 and 2009. During 2005 to 2007, financial... -

Page 138

...the rate at which this replacement is occurring continues to be negatively affected by low demand for new purchase mortgage originations and a lengthy foreclosure process in many states. For the years ended December 31, 2012 and 2011, loans originated in 2005 through 2008 in our single-family credit... -

Page 139

... data provided was not sufficient for us to determine whether the mortgage was a cash-out or a no cash-out refinance transaction. (5) Includes manufactured housing and homes within planned unit development communities. The UPB of manufactured housing mortgage loans purchased during 2012, 2011... -

Page 140

...of the property at origination based on changes in the market value of homes in the same geographical area since origination. (5) Relief refinance mortgages of all LTV ratios comprised approximately 18%, 11%, and 7% of our single-family credit guarantee portfolio by UPB as of December 31, 2012, 2011... -

Page 141

... levels during 2012, as low interest rates contributed to high refinance activity in 2012 and 2011. Cash-out refinancings generally have had a higher risk of default than mortgages originated in no cash-out, or rate and term, refinance transactions. Property Type Townhomes and detached single-family... -

Page 142

... jumbo loans in our single-family credit guarantee portfolio. Interest-only and option ARM loans have experienced significantly higher serious delinquency rates than fixed-rate amortizing mortgage products. Interest-Only Loans Interest-only loans have an initial period during which the borrower pays... -

Page 143

...presents information for single-family mortgage loans in our single-family credit guarantee portfolio, excluding Other Guarantee Transactions, at December 31, 2012 that contain interest-only payment terms. The reported balances in the table below are aggregated by interest-only loan product type and... -

Page 144

... Investments in Securities." Adjustable-Rate Mortgage Loans The table below presents information for single-family mortgage loans in our single-family credit guarantee portfolio, excluding Other Guarantee Transactions, at December 31, 2012 that contain adjustable payment terms. The reported balances... -

Page 145

...worth and fair value of net assets" for additional information. Since a substantial portion of ARM loans were originated in 2005 through 2008 and are located in geographical areas that have been most impacted by declines in home prices since 2006, we believe that the serious delinquency rate for ARM... -

Page 146

...-agency mortgage-related securities see "CONSOLIDATED BALANCE SHEETS ANALYSIS - Investments in Securities." Higher-Risk Loans in the Single-Family Credit Guarantee Portfolio The table below presents information about certain categories of single-family mortgage loans within our single-family credit... -

Page 147

... and foreclosure transfers. While the balance of our non-HARP mortgages with original LTV ratios greater than 90% declined during 2012 because of liquidations, our purchases of these loans increased because: (a) most mortgage insurance companies lowered their premiums in 2011 for certain higher-risk... -

Page 148

... troubled assets and lowering credit losses. Our loan workouts consist of: (a) forbearance agreements; (b) repayment plans; (c) loan modifications; and (d) foreclosure alternatives (e.g., short sales or deed in lieu of foreclosure transactions). Our single-family loss mitigation strategy emphasizes... -

Page 149

... and Market Risks - Seller/servicers may fail to perform their obligations to service loans in our single-family and multifamily mortgage portfolios or that their servicing performance could decline." Home Affordable Modification Program HAMP commits U.S. government, Freddie Mac and Fannie Mae funds... -

Page 150

...or fixed-rate terms. HARP is targeted at borrowers with current LTV ratios above 80%; however, our relief refinance initiative also allows borrowers with LTV ratios of 80% and below to participate. In October 2011, FHFA, Freddie Mac, and Fannie Mae announced a series of FHFA-directed changes to HARP... -

Page 151

.... Relief refinance mortgages of all LTV ratios comprised approximately 18% and 11% of the UPB in our total single-family credit guarantee portfolio at December 31, 2012 and 2011, respectively. Home Affordable Foreclosure Alternatives Program HAFA is designed to permit borrowers who meet basic... -

Page 152

...term extension and principal forbearance ...Total loan modifications(3) ...Repayment plans(4) ...Forbearance agreements(5) ...Total home retention actions ...Foreclosure alternatives: Short sale ...Deed in lieu of foreclosure transactions ...Total foreclosure alternatives ...Total single-family loan... -

Page 153

... at the time of the modification. As a result, the risk of redefault may increase for these borrowers due to the increase in monthly payments resulting from these scheduled increases in the contractual interest rate of the modified loan. A significant number of HAMP loan modifications were completed... -

Page 154

... single-family serious delinquency rate information based on the number of loans that are three monthly payments or more past due or in the process of foreclosure, as reported by our servicers. Mortgage loans that have been modified are not counted as seriously delinquent as long as the borrower... -

Page 155

... rates on single-family loans originated between 2005 and 2008. We purchased significant amounts of loans with higher-risk characteristics in those years and those borrowers have been more susceptible to the declines in home prices and weak economic conditions since 2006. 150 Freddie Mac -

Page 156

...-A Non Alt-A Current LTV Percentage UPB UPB Total UPB Ratio(1) Modified(2) (dollars in billions) Serious Delinquency Rate Geographical distribution: Arizona, California, Florida, and Nevada(3) ...All other states ...Year of origination: 2012 ...2011 ...2010 ...2009 ...2008 ...2007 ...2006 ...2005... -

Page 157

...(2) Rate Current LTV Ratio All Loans(1) Percentage of Portfolio(2) Percentage Modified(3) Serious Delinquency Rate By Product Type FICO scores < 620: 20 and 30- year or more amortizing fixed-rate ...15- year amortizing fixed-rate ...ARMs/adjustable rate(4) ...Interest-only(5) ...Other(6) ...Total... -

Page 158

...Current LTV Ratio All Loans(1) Percentage of Portfolio(2) Percentage Modified(3) Serious Delinquency Rate By Product Type FICO scores < 620: 20 and 30- year or more amortizing fixedrate ...15- year amortizing fixed-rate ...ARMs/adjustable rate(4) ...Interest only(5) ...Other(6) ...Total FICO scores... -

Page 159

...and Alt-A mortgage products in these years; and (c) an environment of persistently high unemployment, decreasing home sales, and broadly declining home prices in the period following the loans' origination. Multifamily Mortgage Credit Risk To manage our multifamily mortgage portfolio credit risk, we... -

Page 160

... for more information about our multifamily delinquency rates. (2) Original LTV ratios are calculated as the UPB of the mortgage, divided by the lesser of the appraised value of the property at the time of mortgage origination or, except for refinance loans, the mortgage borrower's purchase price... -

Page 161

...except financial guarantees that are backed by HFA bonds due to the credit enhancement provided by the U.S. government. We report multifamily delinquency rates based on UPB of mortgage loans that are two monthly payments or more past due or in the process of foreclosure, as reported by our servicers... -

Page 162

... with an improvement in borrower payment performance within our single-family credit guarantee portfolio, which led to a decline in the level of our loan loss reserves in 2012. The amount of non-performing assets increased to $135.7 billion as of December 31, 2012, from $129.2 157 Freddie Mac -

Page 163

... quarter of 2012, the balance of our non-performing loans would have declined in 2012 due to a combination of improved borrower payment performance and the continued high levels of foreclosure transfers, short sales, and REO dispositions during 2012. TDRs include HAMP and non-HAMP loan modifications... -

Page 164

... of foreclosures associated with loans in our single-family credit guarantee portfolio, excluding Other Guarantee Transactions, ranged from 390 days in Michigan to 1,026 days in Florida. As of December 31, 2012, our serious delinquency rate for the aggregate of those states that require a judicial... -

Page 165

... delinquent, or in foreclosure, result in credit losses. The table below provides detail on our credit loss performance associated with mortgage loans and REO assets on our consolidated balance sheets and underlying our non-consolidated mortgage-related financial guarantees. 160 Freddie Mac -

Page 166

... recoveries of loss from credit enhancement and seller/servicer repurchases. We primarily record charge-offs at the time we take ownership of a property through foreclosure and at the time of settlement of foreclosure alternatives (e.g., short sales). Single-family charge-offs, gross, for 2012 and... -

Page 167

...offs primarily result from foreclosure alternatives and REO acquisitions on loans where a share of default risk has been assumed by mortgage insurers, servicers, or other third parties through credit enhancements. As shown in the table above, our charge-offs improved during 2012 compared to 2011 in... -

Page 168

...loans purchased on our consolidated statements of comprehensive income. (4) Recoveries of charge-offs primarily result from foreclosure alternatives and REO acquisitions on loans where: (a) a share of default risk has been assumed by mortgage insurers, servicers or other third parties through credit... -

Page 169

... in UPB of loans discharged in Chapter 7 bankruptcy as TDRs in the third quarter of 2012. The majority of these loans were not seriously delinquent at the time of reclassification. (2) Consists of foreclosure transfers or foreclosure alternatives, such as a deed in lieu of foreclosure or short sale... -

Page 170

...." For information about institutional credit risk associated with our investments in non-mortgage-related securities, see "NOTE 7: INVESTMENTS IN SECURITIES - Table 7.9 - Trading Securities" as well as "Cash and Other Investments Counterparties" below. Single-family Mortgage Seller/Servicers We... -

Page 171

... warranties on the original mortgage being refinanced. For more information on HARP, see "Mortgage Credit Risk - Single-Family Mortgage Credit Risk - Single-Family Loan Workouts and the MHA Program - Relief Refinance Mortgage Initiative and the Home Affordable Refinance Program." We launched a new... -

Page 172

... to mortgage insurance rescission or mortgage insurance claim denial. During 2010 and 2009, we entered into agreements with certain of our seller/servicers to release specified loans from certain repurchase obligations in exchange for one-time cash payments. As of December 31, 2012, loans totaling... -

Page 173

... business or no longer approved as our seller/servicers, at December 31, 2012. Table 64 - Loans Released from Repurchase Obligations(1) As of December 31, 2012 Percentage of Single-family Credit Guarantee UPB Portfolio (in billions) Year of origination: Negotiated agreements: 2008 ...2007 ...2006... -

Page 174

... credit risk relating to the potential insolvency of, or non-performance by, mortgage insurers that insure single-family mortgages we purchase or guarantee. As a guarantor, we remain responsible for the payment of principal and interest if a mortgage insurer fails to meet its obligations... -

Page 175

... mortgage insurers, net of associated reserves, of $0.8 billion and $1.0 billion as of December 31, 2012 and 2011, respectively. The UPB of single-family loans covered by pool insurance declined approximately 73% during 2012, primarily due to a settlement with MGIC concerning our current and future... -

Page 176

...bond insurers' ability to meet their obligations in making our impairment determinations on our non-agency mortgage-related securities at December 31, 2012 and 2011. See "NOTE 7: INVESTMENTS IN SECURITIES - Other-Than-Temporary Impairments on Available-For-Sale Securities" for additional information... -

Page 177

... cash and securities purchased under agreements to resell invested with institutional counterparties; or (b) cash deposited with the Federal Reserve Bank. See "NOTE 15: CONCENTRATION OF CREDIT AND OTHER RISKS" for further information on counterparty credit ratings and concentrations within our cash... -

Page 178

... agreements we have with derivative counterparties, the amount of collateral that we are required to post is based on the credit rating of our long-term senior unsecured debt securities from S&P or Moody's. The lowering or withdrawal of our credit rating by S&P or Moody's may increase our obligation... -

Page 179

... regularly review the market values of the securities pledged to us to minimize our exposure to loss. When non-cash collateral is posted to us, we require collateral in excess of our exposure to satisfy the net obligation to us in accordance with the counterparty agreement. Includes amounts related... -

Page 180

... than 60 days, and we monitor the credit fundamentals of the counterparties to these commitments on an ongoing basis in an effort to ensure that they continue to meet our internal risk-management standards. Selected European Sovereign and Non-Sovereign Exposures The sovereign debt of Spain, Italy... -

Page 181

... - Legislative and Regulatory Developments - Developments Concerning Single-Family Servicing Practices" for more information. Our business decision-making, risk management, and financial reporting are highly dependent on our use of models. In recent periods, external market factors have continued to... -

Page 182

... our ability to: (a) serve our mission and meet our objectives; (b) manage credit and other risks related to our mortgage portfolio; (c) reduce the need to draw funds from Treasury; and (d) issue timely financial statements. Our ability to attract and retain executives and other employees is also... -

Page 183

... net payments on derivative instruments; pay dividends on our senior preferred stock; purchase mortgage-related securities and other investments; purchase mortgage loans; and remove modified or seriously delinquent loans from PC trusts. We fund our cash requirements primarily by issuing short-term... -

Page 184

...-related investments be comprised of short-maturity U.S. Treasury or government guaranteed securities, overnight and term repurchase agreements, unsecured Federal Funds, bank certificates of deposit, and cash. Throughout 2012, we complied with all requirements under our liquidity management policies... -

Page 185

... preferred stock is limited and we will not be able to do so for the foreseeable future, if at all. For more information on the Purchase Agreement, see "BUSINESS - Treasury Agreements." Other Debt Securities We fund our business activities primarily through the issuance of short- and long-term debt... -

Page 186

... of the market for our debt securities and to manage our mix of liabilities funding our assets. To fund our business activities, we depend on the continuing willingness of investors to purchase our debt securities. The required reduction in our mortgage-related investments portfolio has... -

Page 187

... repurchase activities also help us manage the funding mismatch, or duration gap, created by changes in interest rates. For example, when interest rates decline, the expected lives of our investments in mortgage-related securities decrease which reduces the need for long-term debt. We use a number... -

Page 188

...fund our business operations. For additional information on these assets, see "CONSOLIDATED BALANCE SHEETS ANALYSIS - Cash and Cash Equivalents, Federal Funds Sold and Securities Purchased Under Agreements to Resell" and "- Investments in Securities - Non-Mortgage-Related Securities." Mortgage Loans... -

Page 189

... net worth results as of December 31, 2012 and 2011. In addition, notwithstanding our failure to maintain required capital levels, FHFA directed us to continue to make interest and principal payments on our subordinated debt. For more information, see "BUSINESS - Regulation and Supervision - Federal... -

Page 190

... information on the effect of the Purchase Agreement on our business and capital management activities, and the potential impact of making additional draws, see "BUSINESS - Conservatorship and Government Support for Our Business." FAIR VALUE MEASUREMENTS AND ANALYSIS Fair Value Measurements We use... -

Page 191

... processes, help ensure that the prices used to develop our financial statements are in accordance with the accounting guidance for fair value measurements and disclosures. See "NOTE 16: FAIR VALUE DISCLOSURES - Changes in Fair Value Levels" for a discussion of changes in our Level 3 assets... -

Page 192

... fair value balance sheets, we use a number of financial models. See "QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK - InterestRate Risk and Other Market Risks," and "RISK FACTORS" and "RISK MANAGEMENT - Operational Risks" for information concerning the risks associated with these... -

Page 193

... and market conditions. This estimate considers both contractual management and guarantee fees collected over the life of the credit guarantees and credit-related delivery fees collected up front when pools are formed, and associated costs and obligations, which include default costs. Change in... -

Page 194

...the HFA initiative, we, together with Fannie Mae, provide liquidity guarantees for certain variable-rate single-family and multifamily housing revenue bonds, under which Freddie Mac generally is obligated to purchase 50% of any tendered bonds that cannot be remarketed within five business days. 189... -

Page 195

... for mortgage loans and mortgage-related securities. Some of these commitments are accounted for as derivatives. Their fair values are reported as either derivative assets, net or derivative liabilities, net on our consolidated balance sheets. For more information, see "RISK MANAGEMENT - Credit Risk... -

Page 196

... changes to the quarterly commitment fee and dividends on the senior preferred stock beginning in 2013; • future cash settlements on derivative agreements not yet accrued, because the amount and timing of such payments are dependent upon changes in the underlying financial instruments in response... -

Page 197

... Risks - We face risks and uncertainties associated with the models that we use for financial accounting and reporting purposes, to make business decisions, and to manage risks. Market conditions have raised these risks and uncertainties." Individually impaired single-family loans include loans... -

Page 198

..., and available economic data related to multifamily real estate, including apartment vacancy and rental rates. Multifamily loans evaluated collectively for impairment are aggregated into book year vintages and measured by benchmarking published historical commercial mortgage data to those vintages... -

Page 199

... of time our available-for-sale securities have been in an unrealized loss position. Also see "NOTE 7: INVESTMENTS IN SECURITIES - Table 7.3 - Significant Modeled Attributes for Certain Non-Agency Mortgage-Related Securities" for the modeled default rates and severities that were used to determine... -

Page 200

... as to when borrowers will pay the outstanding principal balance of mortgage loans and mortgage-related securities, known as prepayment risk, and the resulting potential mismatch between the timing of: (a) our receipt of cash flows related to our assets; and (b) payment of cash flows related to the... -

Page 201

...the long-term value of our guarantee business because these changes do not take into account the potential for new future guarantee business activity. • Other assets with minimal interest-rate sensitivity. We do not include other assets, primarily non-financial instruments such as fixed assets and... -

Page 202

..., to make business decisions and to manage risks. Market conditions have raised these risks and uncertainties" for a discussion of the risks associated with our use of models. Given the importance of models to our investment management practices, model changes undergo a rigorous review process. As... -

Page 203

..."NOTE 16: FAIR VALUE DISCLOSURES - Valuation Processes and Controls over Fair Value Measurement." Annually, the Business and Risk Committee of our Board of Directors establishes certain Board limits for interest-rate risk measures, and if we exceed these limits we are required to notify the Business... -

Page 204

... in recent years to measure and manage the interest-rate risk related to mortgage assets as risk for prepayment model error remains high due to the low interest rate environment and uncertainty regarding default rates, unemployment rates, the effect of widespread loan modification programs, and the... -

Page 205

... the third and fourth quarters of 2012, we made assumption changes related to our prepayment model for non-HARP eligible loans underlying our securities. In addition, we enhanced our process used to estimate duration and convexity of our unsecuritized single-family loans by incorporating additional... -