Cogeco 2009 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2009 Cogeco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

|

|

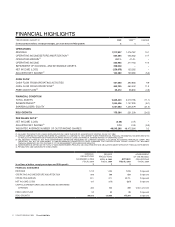

14 COGECO CABLE INC. 2009 Management’s discussion and analysis

The adoption of these standards did not have any impact on the classification and measurements of the Corporation’s financial

instruments. The new disclosures pursuant to these new Sections are included in note 19 of the Corporation’s consolidated financial

statements.

GENERAL STANDARDS OF FINANCIAL STATEMENT PRESENTATION

The CICA amended Section 1400 of the CICA Handbook, General Standards of Financial Statement Presentation, to include a

requirement for management to make an assessment of the entity’s ability to continue as a going concern when preparing financial

statements. These changes, including the related disclosure requirements, were adopted by the Corporation on September 1, 2008

and had no impact on the consolidated financial statements.

CREDIT RISK AND FAIR VALUE OF FINANCIAL ASSETS AND FINANCIAL LIABILITIES

On January 20, 2009, the Emerging Issues Committee (“EIC”) of the Canadian Accounting Standards Board issued EIC Abstract

173, Credit Risk and Fair Value of Financial Assets and Financial Liabilities, which establishes guidance requiring an entity to

consider its own credit risk as well as the credit risk of the counterparty in determining the fair value of financial assets and financial

liabilities, including derivative instruments. EIC 173 is applicable to all financial assets and liabilities measured at fair value in interim

and annual financial statements for periods ending on or after January 20, 2009 and is applicable to the Corporation for its second

quarter of fiscal 2009 with retrospective application, without restatement of prior periods, to the beginning of its current fiscal year.

The adoption of this new abstract during the second quarter had no significant impact on the consolidated balance sheet at

September 1, 2008.

ADOPTED DURING FISCAL 2008

FINANCIAL INSTRUMENTS

Effective September 1, 2007, the Corporation adopted the CICA Handbook Section 1530, Comprehensive Income, Section 3855,

Financial Instruments – Recognition and Measurement, Section 3861, Financial Instruments – Disclosure and Presentation, Section

3865, Hedges and Section 3251, Equity.

Statements of comprehensive income

A new statement, entitled consolidated statements of comprehensive income, was added to the Corporation’s consolidated financial

statements and includes net income as well as other comprehensive income. Other comprehensive income represents changes in

shareholders’ equity arising from transactions and events from non-owner sources, such as changes in foreign currency translation

adjustments of a net investment in self-sustaining foreign subsidiaries, long-term debt designated as a hedge of a net investment in

self-sustaining foreign subsidiaries, and changes in the fair value of effective cash flow hedging instruments.

Recognition and measurement of financial instruments

Under these new standards, all financial assets, including derivatives, must be classified as available-for-sale, held-for-trading, held-

to-maturity, or loans and receivables. All financial liabilities, including derivatives, must be classified as held-for-trading or other

liabilities. All financial instruments classified as available-for-sale or held-for-trading are recognized at fair value on the consolidated

balance sheet while financial instruments classified as loans and receivables or other liabilities will continue to be measured at

amortized cost using the effective interest rate method. The standards allow the Corporation the option to designate certain financial

instruments, on initial recognition, as held-for-trading.

All of the Corporation's financial assets are classified as held-for-trading or loans and receivables. The Corporation has classified its

cash and cash equivalents as held-for-trading. Accounts receivable have been classified as loans and receivables. All of the

Corporation’s financial liabilities were classified as other liabilities, except for the cross-currency swap agreements, which were

classified as held-for-trading. Held-for-trading assets and liabilities are carried at fair value on the consolidated balance sheet, with

changes in fair value recorded in the consolidated statements of income, except for the changes in fair value of the cross-currency

swap agreements, which are designated as cash flow hedges of the Senior Secured Notes Series A and are recorded in other

comprehensive income. Loans and receivables and all financial liabilities are carried at amortized cost using the effective interest

rate method. Upon adoption, the Corporation determined that none of its financial assets are classified as available-for-sale or held-

to-maturity. Except for the treatment of transaction costs and derivative financial instruments mentioned below, the provisions of the

new accounting standards had no impact on the consolidated financial statements on September 1, 2007.

Transaction costs

Effective September 1, 2007, transaction costs are capitalized on initial recognition and presented as a reduction of the related

financing, except for transaction costs on the revolving loan and the swingline facility, which are presented as deferred charges.

These costs are amortized over the term of the related financing using the effective interest rate method, except for transaction

costs on the revolving loan and the swingline facility, which are amortized over the term of the related financing on a straight-line