Circuit City 2001 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2001 Circuit City annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

|

|

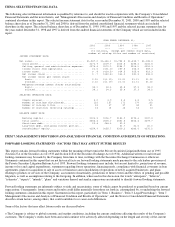

The Company's cash balance increased $22.0 million to $36.5 million during the year ended December 31, 2001. The Company's working

capital was $103 million at December 31, 2001, down from $107 million at the end of 2000. This was due principally to a $47 million decrease

in accounts receivable and a $35 million decrease in inventories, offset by a $22 million increase in cash, a $46 million decrease in notes

payable to banks and a $39 million decrease in accrued expenses and other current liabilities.

The Company maintains its cash and cash equivalents primarily in money market funds or their equivalent. The Company does not have any

derivative financial instruments. As of December 31, 2001, all of the Company's investments mature in less than three months. Accordingly,

the Company does not believe that its investments have significant exposure to interest rate risk.

Cash was provided by operating activities in each of the three years presented, $95.6 million in 2001, $8.5 million in 2000 and $20.5 million in

1999. Cash flow was provided in 2001 through additional inventory reductions, decreases in accounts receivable and receipt of a tax refund

resulting from the loss recorded in 2000, offset by a decrease in accounts payable. The significant loss incurred by the Company in 2000 was

the primary reason for the decrease in operating cash flow compared to 1999. However, cash flow was provided by operations in 2000 as a

result of reductions in inventories and a decrease in accounts receivable.

In 2001 the Company used cash in investing activities of $23.8 million, primarily for property, plant and equipment additions. These included

$9.5 million for software and systems development and $5.5 million toward the construction of a new facility for the Company's United

Kingdom operations. In 2000 the Company used net cash in investing activities of $40.7 million for property, plant and equipment additions.

Capital additions in 2000 included $13.6 million for the purchase and outfitting of a new distribution facility in Georgia, $2 million for

upgrading the Company's information systems infrastructure and $7.9 million in connection with software development programs. In 1999 the

Company used net cash of $36.1 million for investing activities. Expenditures for property, plant and equipment totaled $22.0 million and

included expenditures related to expansion of the Company's PC assembly facility and improvements to information systems. Expenditures for

business acquisitions, including the payment of contingent consideration, totaled $19.2 million. Short-term investments decreased by $5.1

million to partially fund these activities.

Capital expenditures in 2002 are expected to be $10 million and includes the completion of the construction of a new UK facility. The

Company plans to fund these expenditures out of cash from operations and borrowings.

In 2001, $45.8 million of cash was used in financing activities, all of which went to pay down short-term borrowings. In 2000, $27.5 million

was provided by financing activities and in 1999 $3.8 million of cash was used in financing activities. In 2000, the Company purchased 1.1

million treasury shares for $9.8 million and used $2.2 million to repay a long-term loan in Europe. The Company borrowed $39.6 million to

finance these expenditures as well as the fixed asset additions. In 1999, $10.1 million was used to repurchase 890,000 shares of the Company's

common stock and $2.8 million was used to repay a mortgage loan. This was partially funded by $9.0 million in short-term bank borrowings.

As a result of the net loss incurred in the United States in the year ended December 31, 2001, the Company intends to apply for a refund of

approximately $9 million from the Internal Revenue Service. The Company applied for and received a refund of approximately $25 million

from the Internal Revenue Service for the net loss incurred in 2000.

In June 2001, the Company entered into a $70,000,000 revolving credit agreement with a group of financial institutions to provide for

borrowings in the United States. The borrowings are secured by all of the domestic accounts receivable and inventories of the Company and the

Company's shares of stock and membership interests in its domestic subsidiaries. The credit facility expires and outstanding borrowings

thereunder are due on June 15, 2004. The borrowings under the agreement are subject to borrowing base limitations of up to 75% of eligible

accounts receivable and up to 25% of qualified inventories. The interest on outstanding advances is payable monthly, at the Company's option,

at the agent bank's base rate (4.75 at December 31, 2001) plus 0.25% to 0.75% or the bank's daily LIBOR rate (3.62% at December 31, 2001)

plus 2.25% to 3%. The facility also calls for a commitment fee payable quarterly in arrears of 0.5% of the average daily unused portion of the

facility. The undrawn availability under the agreement may not be less than $20,000,000 prior to June 30, 2002. As of December 31, 2001,

availability under the agreement was $45,291,000, against which there were no outstanding advances and there were outstanding letters of

credit of $4,000,000. The revolving credit agreement contains certain financial and other covenants, including restrictions on capital

expenditures and payments of dividends.

The Company also has a (pound)15,000,000 ($21,828,000 at the December 31, 2001 exchange rate) multi-currency credit facility with a

financial institution in the United Kingdom, which is available to its United Kingdom subsidiaries. Drawings under the facility may be made by

overdraft, trade acceptance or loan. The facility is secured by assets of certain of the Company's United Kingdom subsidiaries and a guaranty

from Systemax. At December 31, 2001 there were

(pound)1,944,000 ($2,829,000) of borrowings outstanding under this line.

The Company has accepted a proposal from a financial institution and signed a commitment letter for an $8.4 million, ten-year mortgage on its

Suwanee, Georgia distribution facility. The loan will bear interest at 7.04%. Closing is subject to due diligence and negotiation of a definitive

agreement.

The Company is obligated under operating leases for the rental of certain facilities and equipment which expire at various dates through 2013.

The Company currently leases its two New York facilities from entities owned by Richard Leeds, Robert Leeds and Bruce Leeds, the

Company's three principal stockholders and senior executive officers. The annual rentals total $1.2 million and both leases expire in 2007.

The Company believes it has access to adequate funds for continued operations and growth through its available cash balances and funds