Ameriprise 2008 Annual Report Download

Download and view the complete annual report

Please find the complete 2008 Ameriprise annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

Annual Report 2008

Table of contents

-

Page 1

Annual Report 2008 -

Page 2

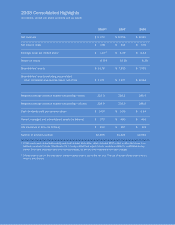

...,824 12,592 2008 results were impacted by equity and credit market dislocation, which included $917 million in after-tax losses from realized investment losses, RiverSource 2a-7 money market fund support costs, expenses related to unafï¬liated money market funds and integration and restructuring... -

Page 3

... us to protect our franchise while focusing on executing our strategy and investing in our long-term opportunity. We were not, however, immune to the environment in 2008. Client assets decreased along with the markets, James M. Cracchiolo Chairman and CEO Ameriprise Financial 2008 Annual Report 1 -

Page 4

... by using new products, services and technology. As the markets deteriorated later in the year, we developed a new online market resource center to help advisors provide current information to their clients. In addition, we broadened market resources and perspectives on our public website. As... -

Page 5

...of individual investors. Approximately 300,000 of our clients had invested their cash-funds many clients used to pay routine expenses-in Reserve money market funds. We promptly stepped up for clients: We advanced affected clients approximately $400 million to help meet their immediate cash needs; we... -

Page 6

..., from cash management and lending to investments, insurance and annuities. In 2008, many of our clients sought the safety of cash or other liquid or ï¬xed-interest-rate products. The resulting shift from wrap accounts, variable annuities and mutual funds to FDIC-insured banking products, certi... -

Page 7

... in annuity account values • Capabilities: variable and fixed annuities Protection • $192 billion in life insurance in force • A leading variable universal life insurance provider in sales • Capabilities: life, health and auto & home insurance Ameriprise Financial 2008 Annual Report 5 -

Page 8

...both in the U.S. and at Threadneedle in the U.K. We intend to reduce pre-acquisition general and administrative expenses by approximately 10 percent in 2009; this is on top of the signiï¬cant reduction we achieved in 2008. As is appropriate in the current 6 Ameriprise Financial 2008 Annual Report -

Page 9

... granted cash bonuses for 2008. In addition to our ï¬nancial and management strengths, our business is underpinned by a deeply talented and dedicated group of senior leaders and employees; together we continue to stress careful decision-making and service to our clients and advisors. Our employees... -

Page 10

We're building on our strong foundation. Clear client focus Diversiï¬ed business model Strong balance sheet fundamentals 8 Ameriprise Financial 2008 Annual Report -

Page 11

... to address cash management, savings, borrowing, investing, protection, retirement income and estate planning. This holistic approach and commitment to ï¬nancial planning creates client-advisor relationships that endure. We are the leader in ï¬nancial planning. It's a long-term process... -

Page 12

We remain committed to our prudent approach. En ter pri se ris km an ag em en t g rin e e gin n e reg n goi n O nagement a m l a it p a c Conservative In cr ea se d tra ns pa re nc y 10 Ameriprise Financial 2008 Annual Report -

Page 13

...at 12/31/08 was $34 billion) Cash and cash equivalents 18% U.S. Gov't & Agency-backed 18% Investment grade 47% Below investment grade 5% Direct loans/non-rated 12% General and Administrative Expenses (In billions) 2005 2006 2007 2008 $2.3 $2.5 $2.6 $2.4 Ameriprise Financial 2008 Annual Report 11 -

Page 14

We derive strength from personal client-advisor relationships. Highly satisï¬ed advisor force Enduring client-advisor relationships Stable client base 12 Ameriprise Financial 2008 Annual Report -

Page 15

...ensure advisors can meet clients' changing needs. As market declines increased investor anxiety, clients sought more conservative products, generating strong sales in certiï¬cates, FDIC-insured banking products and ï¬xed annuities. We also experienced lower sales in wrap products, mutual funds and... -

Page 16

We're in position to capture opportunities. in grow Investing th tribution is d g in d n Expa hnology c e t d n a g tools Enhancin r advisors u o g in in Tra ovation n in g in r e Deliv s d advisor e c n ie r e p ex Recruiting 14 Ameriprise Financial 2008 Annual Report -

Page 17

... in 2008, we strengthened our business-completing three all-cash acquisitions that will increase advisor productivity, enhance our asset management capabilities and expand distribution levels. We acquired H&R Block Financial Advisors and an independent broker-dealer, Brecek & Young Advisors, adding... -

Page 18

We're committed to delivering long-term shareholder value. 16 Ameriprise Financial 2008 Annual Report Tak ing the lon gv iew -

Page 19

...' trust. Financial Targets Net revenue growth (On average, over time) 6-8% 12-15% 12-15% Earnings per share growth Return on equity Annual Dividends (In millions) 2005 2006 2007 2008 $27 $108 $133 $143 In 2008, our employee giving campaign raised a record $4.4 million. "Our corporate giving... -

Page 20

... services for Ameriprise Financial Services, Inc. RiverSource insurance and annuity products are issued by RiverSource Life Insurance Company and in New York, by RiverSource Life Insurance Co. of New York, Albany, NY, and distributed by RiverSource Distributors, Inc. Ameriprise Auto & Home Insurance... -

Page 21

Ameriprise Financial, Inc. 2008 Form 10-K -

Page 22

... EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2008 OR អ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO COMMISSION FILE NUMBER 1-32525 AMERIPRISE FINANCIAL, INC. Delaware (State or other jurisdiction of... -

Page 23

... Independence ...147 Principal Accountant Fees and Services ...147 Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities ...37 Selected Financial Data ...39 Management's Discussion and Analysis of Financial Condition and Results of Operations... -

Page 24

... in financial planning and a client retention percentage rate of 94%. Branded financial plan net cash sales for the year ended December 31, 2008 increased 4% compared to the year-ago period. Our multi-platform network of affiliated financial advisors is the means by which we develop personal... -

Page 25

... through our branded advisors (e.g., investment advisory accounts, retail brokerage services and banking products) and products and services that we market directly to consumers (e.g., personal auto and home insurance). We use our RiverSource brand for our U.S. asset management, annuity, and the... -

Page 26

... Fund Distributors, Inc. RiverSource Distributors, Inc. RiverSource Life Insurance Company RiverSource Service Corporation IDS Property Casualty Insurance Company Ameriprise Certificate Company Ameriprise Trust Company Ameriprise Bank, FSB RiverSource Life Insurance Co. of New York... -

Page 27

...companies.'' • RiverSource Service Corporation is a transfer agent that processes client transactions for our RiverSource mutual funds and Ameriprise face-amount certificates. Its results of operations are included in our Asset Management segment. • IDS Property Casualty Insurance Company (''IDS... -

Page 28

... transfer products and services, as well as a selection of products from other companies, as more fully described below. Brokerage and Investment Advisory Services Individual and Family Financial Services Our branded advisors deliver financial solutions to our advisory clients by building long-term... -

Page 29

... the products that we sell to them. These commissions, sales loads and other revenues are separate from and in addition to the financial planning fees we and our affiliated financial advisors may receive. We earned branded financial planning net cash sales in 2008 of $211 million, a 4% increase over... -

Page 30

... in investment-secured loan and line of credit balances and $99 million in unsecured balances (including credit card balances), net of premiums and discounts, and capitalized lender paid origination fees. Ameriprise Bank's strategy and operations are focused on serving branded advisor clients. We... -

Page 31

...), savings and loan associations, credit unions, mutual funds, insurance companies and similar financial institutions, which may be viewed by potential customers as offering a comparable or superior combination of safety and return on investment. In times of weak performance in the equity markets... -

Page 32

... of Financial Condition and Results of Operations'' included in Part II, Item 7 of this Annual Report on Form 10-K. Investment Management Capabilities and Development Our investment management teams manage the majority of assets in our RiverSource, Threadneedle and Seligman families of mutual funds... -

Page 33

... is a long/short strategy, and two new property unit trusts, all of which launched in 2008. We also provide seed money to certain of our investment management teams to develop new products for our institutional clients. Asset Management Offerings Mutual Fund Families-RiverSource, Threadneedle and... -

Page 34

...property fund of funds. During the third quarter of 2008, Threadneedle began managing 2 new mutual funds in the U.S. Separately Managed Accounts We provide investment management services to pension, profit-sharing, employee savings and endowment funds, accounts of large- and medium-sized businesses... -

Page 35

... with the Securities and Exchange Commission (''SEC'') and offered primarily through banks and other financial institutions to institutional clients such as retirement, pension and profit-sharing plans. We currently serve as investment manager to 51 Ameriprise Trust Company collective funds covering... -

Page 36

... in connection with a restructuring of the portfolio and a move to more market-aligned rates and terms. Our Segments-Annuities Our Annuities segment provides RiverSource Life variable and fixed annuity products to retail clients primarily distributed through our affiliated financial advisors and... -

Page 37

... marketing support payments from the affiliates of other companies' funds included as investment options in our RiverSource variable annuity products. Fixed Annuities RiverSource fixed annuity products provide a contractholder with cash value that increases by a fixed or indexed interest rate... -

Page 38

...insurance products in force offer a fixed account investment option with guaranteed minimum interest crediting rates ranging from 3.0% to 4.5% at December 31, 2008. For the nine months ended September 30, 2008, RiverSource Life ranked fifth in sales of variable universal life based on total premiums... -

Page 39

...risks associated with variable universal life insurance. RiverSource fixed universal life insurance products provide life insurance coverage and cash value that increases by a fixed interest rate. The rate is periodically reset at the discretion of the issuing company subject to certain policy terms... -

Page 40

... new policy sales of our Property Casualty companies in 2008. Through other alliances, we market our property casualty products to certain consumers who have a relationship with Delta Air Lines and offer personal auto, home and liability insurance products to customers of Ford Motor Credit Company... -

Page 41

..., brand recognition, investor confidence, type and quality of services, fee structures, distribution, and type and quality of service. Our brokerage subsidiaries compete with securities broker-dealers, independent broker-dealers, financial planning firms, registered investment advisors, insurance... -

Page 42

... that manage individual brokerage, mutual fund, insurance and banking client accounts. Over the years we have updated our platform to include new product lines such as brokerage, deposit, credit and products of other companies, wrap accounts and e-commerce capabilities for our financial advisors and... -

Page 43

...by the SEC and the UK Financial Services Authority (''FSA''). Our European fund distribution activities are also subject to local country regulations. Our Australian CDO management business is regulated by the Australian Securities and Investment Commission (''ASIC''). Our trust company is primarily... -

Page 44

... accounts. The Minnesota Department of Commerce (Insurance Division), the Wisconsin Office of the Commissioner of Insurance and the New York State Insurance Department (the ''Domiciliary Regulators'') regulate certain of the RiverSource Life companies, IDS Property Casualty, and Ameriprise Insurance... -

Page 45

... supervisory regulator under the EU Financial Conglomerates Directive. SECURITIES EXCHANGE ACT REPORTS AND ADDITIONAL INFORMATION We maintain an Investor Relations website at ir.ameriprise.com and we make available free of charge our annual, quarterly and current reports and any amendments to those... -

Page 46

...new purchasers of our products to refrain from purchasing products, such as mutual funds, variable annuities and variable universal life insurance, which have returns linked to the performance of the equity markets. If we are unable to offer appropriate product alternatives which encourage customers... -

Page 47

... effect on the revenues and returns from our asset management services, wrap accounts and variable annuity contracts. Because the profitability of these products and services depends on fees related primarily to the value of assets under management, declines in the equity markets will reduce our... -

Page 48

... by the requirement to pay assessments to the guaranty fund associations. Third-party defaults, bankruptcy filings, legal actions and other events may limit the value of or restrict our access and our clients' access to cash and investments. The extreme capital and credit market volatility that we... -

Page 49

..., economic downturns and corporate malfeasance can increase the number of companies, including those with investment-grade ratings, that default on their debt obligations. Default-related declines in the value of our fixed maturity securities portfolio or consumer credit products could cause our net... -

Page 50

...investment performance, product features, price, perceived financial strength, and claims-paying and credit ratings. Our competitors include broker-dealers, banks, asset managers, insurers and other financial institutions. Many of our businesses face competitors that have greater market share, offer... -

Page 51

... to increase profitability. Sales of our own mutual funds by our affiliated financial advisor network comprise a significant percentage of our total mutual fund sales. We attribute this success to performance, new products and marketing efforts. A decline in the level of investment performance as... -

Page 52

...us marketing, sales and account maintenance support. For example, conflicts may arise between our position as a provider of financial planning services and as a manufacturer and/or distributor or broker of asset accumulation, income or insurance products that one of our affiliated financial advisors... -

Page 53

...: • reducing new sales of insurance products, annuities and investment products; • adversely affecting our relationships with our affiliated financial advisors and third-party distributors of our products; • materially increasing the number or amount of policy surrenders and withdrawals by... -

Page 54

...make greater payments under our life insurance policies and annuity contracts with guaranteed minimum death benefits than we have projected. The risk that our claims experience may differ significantly from our pricing assumptions is particularly significant for our long term care insurance products... -

Page 55

...life and disability income insurance and, to a lesser extent, marketing and promotional expenses for personal auto and home insurance, and distribution expense for certain mutual fund products. For annuity and universal life products, DAC are amortized based on projections of estimated gross profits... -

Page 56

...financial condition and results of operations. Insurance, banking and securities laws and regulations regulate the ability of many of our subsidiaries (such as our insurance, banking and brokerage subsidiaries and our face-amount certificate company) to pay dividends or make other permitted payments... -

Page 57

... in general have experienced volatility that has often been unrelated to the operating performance of a particular company. These broad market fluctuations may adversely affect the trading price of our common stock. Provisions in our certificate of incorporation and bylaws and of Delaware law may... -

Page 58

... to, the company's mutual funds, annuities, insurance products, brokerage services, financial plans and other advice offerings; supervision of the company's financial advisors; supervisory practices in connection with financial advisors' outside business activities; sales practices and supervision... -

Page 59

... date, approximately $0.85 per dollar NAV has been paid to investors by the Reserve Primary Fund. For several years, the company has been cooperating with the SEC in connection with an inquiry into the company's sales of, and revenue sharing relating to, other companies' real estate investment trust... -

Page 60

... Ameriprise Financial, Inc. or any ''affiliated purchaser'' (as defined in Rule 10b-18(a)(3) under the Securities Exchange Act of 1934), of our common stock during the fourth quarter of 2008: (a) Total Number of Shares Purchased (b) (c) Total Number of Shares Purchased as Part of Publicly Announced... -

Page 61

... exercise price, they have been excluded from the weighted average exercise price in column B. Includes 6 million shares of common stock issuable under the terms of the Ameriprise Financial 2008 Employment Incentive Equity Award Plan. As of December 31, 2008, there were no awards granted under this... -

Page 62

...for the five-year period ended December 31, 2008. Certain prior year amounts have been reclassified to conform to the current year's presentation. For the periods preceding our separation from American Express Company (''American Express''), we prepared our Consolidated Financial Statements as if we... -

Page 63

...the Ameriprise Financial brand, separating and reestablishing our technology platforms and advisor and employee retention programs. Effective January 1, 2004, we adopted American Institute of Certified Public Accountants Statement of Position 03-1, ''Accounting and Reporting by Insurance Enterprises... -

Page 64

... to equity risk and interest rate risk, see ''Quantitative and Qualitative Disclosures About Market Risk.'' It is management's priority to increase shareholder value over a multi-year horizon by achieving our on-average, over-time financial targets. Our financial targets are: • Net revenue growth... -

Page 65

... planning and our strong corporate foundation. Our franchisee advisor and client retention remain strong at 92% and 94%, respectively, as of December 31, 2008. Branded financial plan net cash sales for the year ended December 31, 2008 increased 4% compared to the year-ago period. Our owned, managed... -

Page 66

...and Deferred Sales Inducement Costs For our annuity and life, disability income and long term care insurance products, our DAC and DSIC balances at any reporting date are supported by projections that show management expects there to be adequate premiums or estimated gross profits after that date to... -

Page 67

... the new contract. For details regarding the balances of and changes in DAC for the years ended December 31, 2008, 2007 and 2006 see Note 8 to our Consolidated Financial Statements. Liabilities for Future Policy Benefits and Policy Claims and Other Policyholders' Funds Fixed Annuities and Variable... -

Page 68

... and Long Term Care Insurance Future policy benefits and policy claims and other policyholders' funds related to life, disability income and long term care insurance include liabilities for fixed account values on fixed and variable universal life policies, liabilities for unpaid amounts on reported... -

Page 69

... fair value of derivatives hedging variable annuity living benefits, equity indexed annuities and stock market certificates are included within benefits, claims, losses and settlement expenses, interest credited to fixed accounts and banking and deposit interest expense, respectively. The changes in... -

Page 70

... of operations or financial condition, see Note 3 to our Consolidated Financial Statements. Sources of Revenues and Expenses Management and Financial Advice Fees Management and financial advice fees relate primarily to fees earned from managing mutual funds, separate account and wrap account assets... -

Page 71

... life insurance products, variable annuity guaranteed benefit rider charges and administration charges against contractholder accounts or balances. Premiums paid by fixed and variable universal life policyholders and annuity contractholders are considered deposits and are not included in revenue... -

Page 72

... the general account and RiverSource Variable Product funds held in the separate accounts of our life insurance subsidiaries. Administered assets include assets for which we provide administrative services such as client assets invested in other companies' products that we offer outside of our wrap... -

Page 73

...of operations for the years ended December 31, 2008 and 2007. Years Ended December 31, 2008 2007 Change (in millions, except percentages) Revenues Management and financial advice fees Distribution fees Net investment income Premiums Other revenues Total revenues Banking and deposit interest expense... -

Page 74

... fair value of derivatives hedging variable annuity living benefits, equity indexed annuities and stock market certificates were reclassified to benefits, claims, losses and settlement expenses, interest credited to fixed accounts and banking and deposit interest expense, respectively. Prior period... -

Page 75

... total pretax impacts on our revenues and expenses for the year ended December 31, 2007 attributable to the review of valuation assumptions for products of RiverSource Life companies and the impact of markets on DAC and DSIC amortization and variable annuity living benefit riders, net of hedges were... -

Page 76

... was a $42 million expense related to the market's impact on DSIC, a $70 million expense related to the equity market's impact on variable annuity minimum death and income benefits and increases in life, long term care and auto and home insurance benefits. Benefits, claims, losses and settlement... -

Page 77

... Financial Statements for the years ended December 31, 2008 and 2007: Years Ended December 31, Percent Share of Total 2007 (in millions, except percentages) 2008 Percent Share of Total Total net revenues Advice & Wealth Management Asset Management Annuities Protection Corporate & Other... -

Page 78

... Our affiliated advisors utilize a diversified selection of both proprietary and non-proprietary products to help clients meet their financial needs. The following table presents the results of operations of our Advice & Wealth Management segment for the years ended December 31, 2008 and 2007: Years... -

Page 79

... years ended December 31, 2008 and 2007: Years Ended December 31, 2008 2007 Change (in millions, except percentages) Revenues Management and financial advice fees Distribution fees Net investment income Other revenues Total revenues Banking and deposit interest expense Total net revenues Expenses... -

Page 80

...million related to decreased mutual fund sales volume. Annuities Our Annuities segment provides variable and fixed annuity products of RiverSource Life companies to our retail clients primarily through our Advice & Wealth Management segment and to the retail clients of unaffiliated advisors through... -

Page 81

... benefit rider fees on variable annuities driven by volume increases in 2008. Expenses Total expenses increased $122 million, or 7%, to $1.9 billion in 2008, primarily due to an increase in amortization of DAC partially offset by decreases in interest credited to fixed accounts, benefits, claims... -

Page 82

... fees Net investment income Premiums Other revenues Total revenues Banking and deposit interest expense Total net revenues Expenses Distribution expenses Interest credited to fixed accounts Benefits, claims, losses and settlement expenses Amortization of deferred acquisition costs General... -

Page 83

... general and administrative expense was driven by a $77 million expense related to changes in fair value of Lehman Brothers securities that we purchased from various 2a-7 money market mutual funds managed by RiverSource Investments, expense of $36 million for the cost of guaranteeing specific client... -

Page 84

... adjustment on derivatives hedging variable annuity living benefits, equity indexed annuities and stock market certificates were reclassified to benefits, claims, losses and settlement expenses, interest credited to fixed accounts and banking and deposit interest expense, respectively. Prior period... -

Page 85

...variable product fund fee revenue and $8 million from model changes related to variable life second to die insurance. Distribution expenses increased $329 million, or 19%. The increase primarily reflected higher commissions paid driven by overall business growth and increases in advisor productivity... -

Page 86

...fees representing increased spending on investment initiatives, expenses related to Ameriprise Bank, increased hedge fund performance compensation and an increase in technology related costs, partially offset by a decrease in expense in 2007 related to our defined contribution recordkeeping business... -

Page 87

... our financial advisors. Our affiliated advisors utilize a diversified selection of both proprietary and non-proprietary products to help clients meet their financial needs. The following table presents the results of operations of our Advice & Wealth Management segment for the years ended December... -

Page 88

... as an increase in Threadneedle hedge fund performance fees. Management and financial advice fees in 2006 included $27 million related to revenues from our defined contribution recordkeeping business that we sold in the second quarter of 2006. The expenses from the sale of our defined contribution... -

Page 89

... fees Net investment income Premiums Other revenues Total revenues Banking and deposit interest expense Total net revenues Expenses Distribution expenses Interest credited to fixed accounts Benefits, claims, losses and settlement expenses Amortization of deferred acquisition costs General... -

Page 90

... fees Net investment income Premiums Other revenues Total revenues Banking and deposit interest expense Total net revenues Expenses Distribution expenses Interest credited to fixed accounts Benefits, claims, losses and settlement expenses Amortization of deferred acquisition costs General... -

Page 91

...: Years Ended December 31, 2007 2006 Change (in millions, except percentages) Revenues Management and financial advice fees Net investment income Other revenues Total revenues Banking and deposit interest expense Total net revenues Expenses Distribution expenses Interest and debt expense Separation... -

Page 92

... make to reflect an exit price. As a result, we adjust the valuation of variable annuity riders by updating certain contractholder assumptions, adding explicit margins to provide for profit, risk and expenses, and adjusting the rates used to discount expected cash flows to reflect a current market... -

Page 93

...American Enterprise Investment Services, Inc. (''AEIS''), our auto and home insurance subsidiary, IDS Property Casualty Insurance Company (''IDS Property Casualty''), doing business as Ameriprise Auto & Home Insurance, Threadneedle, RiverSource Service Corporation and our investment advisory company... -

Page 94

...2007 2008 2007 (in millions) RiverSource Life(1)(2) RiverSource Life of NY(1)(2) IDS Property Casualty(1)(3) Ameriprise Insurance Company(1)(3) ACC(4)(5) Threadneedle(6) Ameriprise Bank, FSB(7) AFSI(3)(4) Ameriprise Captive Insurance Company Ameriprise Trust Company(3) AEIS(3)(4) Securities America... -

Page 95

... Years Ended December 31, 2007 (in millions) 2006 Cash dividends paid/(contributions made), net RiverSource Life Ameriprise Bank AEIS ACC RiverSource Investments RiverSource Service Corporation Threadneedle Ameriprise Trust Company Securities America Financial Corporation AFSI IDS Property Casualty... -

Page 96

... relate to our Available-for-Sale investment portfolio. Further, this activity is significantly affected by the net outflows of our investment certificate, fixed annuity and universal life products reflected in financing activities. Net cash provided by investing activities for the year ended... -

Page 97

... activities of $4.3 billion for the year ended December 31, 2007, an increase in cash of $4.7 billion. Cash proceeds from additions of investment certificates and banking time deposits increased $1.9 billion, primarily due to an increase in sales of investment certificates as a result of the market... -

Page 98

... and extent of legal claims threatened or initiated by clients, other persons and regulators, and developments in regulation and legislation; • investment management performance and consumer acceptance of the Company's products; • effects of competition in the financial services industry and... -

Page 99

... DSIC assets associated with variable annuity and variable UL products, the values of liabilities for guaranteed benefits associated with our variable annuities and the values of derivatives held to hedge these benefits. Changes in both the equity and fixed income markets during 2008 have affected... -

Page 100

... curve. The selection of a 100 basis point interest rate increase as well as 10% and 20% equity market declines should not be construed as a prediction of future market events. Asset-Based Management and Distribution Fees We earn asset-based management fees on our owned separate account assets and... -

Page 101

... portion of annuity and insurance products of RiverSource Life companies and their investment portfolios. We guarantee an interest rate to the holders of these products. Premiums and deposits collected from clients are primarily invested in fixed rate securities to fund the client credited rate with... -

Page 102

...related to our fixed rate certificate products and $1.4 billion in reserves related to our banking products. Equity Indexed Annuities Our equity indexed annuity product is a single premium annuity issued with an initial term of seven years. The annuity guarantees the contractholder a minimum return... -

Page 103

... whether such variability might reasonably be expected to create exposure to a counterparty in excess of established limits. Additionally, we reinsure a portion of the insurance risks associated with our life, disability income, long term care and auto and home insurance products through reinsurance... -

Page 104

... Financial Statements: Ameriprise Financial, Inc. Report of Independent Registered Public Accounting Firm ...Consolidated Statements of Operations-Years ended December 31, 2008, 2007 and 2006 . . Consolidated Balance Sheets-December 31, 2008 and 2007 ...Consolidated Statements of Cash Flows-Years... -

Page 105

... consolidated balance sheets of Ameriprise Financial, Inc. (the Company) as of December 31, 2008 and 2007, and the related consolidated statements of operations, shareholders' equity, and cash flows for each of the three years in the period ended December 31, 2008. These financial statements are... -

Page 106

... Statements of Operations Ameriprise Financial, Inc. Years Ended December 31, 2008 2007 2006 (in millions, except per share amounts) Revenues Management and financial advice fees Distribution fees Net investment income Premiums Other revenues Total revenues Banking and deposit interest expense... -

Page 107

...cash Other assets Total assets Liabilities and Shareholders' Equity Liabilities: Future policy benefits and claims Separate account liabilities Customer deposits Debt Accounts payable and accrued expenses Other liabilities Total liabilities Shareholders' Equity: Common shares ($.01 par value; shares... -

Page 108

... Premiums and discount amortization Changes in operating assets and liabilities: Segregated cash Trading securities and equity method investments, net Future policy benefits and claims, net Receivables Brokerage deposits Accounts payable and accrued expenses Other, net Net cash provided by operating... -

Page 109

... Statements of Cash Flows (continued) Ameriprise Financial, Inc. Years Ended December 31, 2008 2007 2006 (in millions) Cash Flows from Financing Activities Investment certificates and banking time deposits: Proceeds from additions Maturities, withdrawals and cash surrenders Change in other banking... -

Page 110

... Share-based compensation plans Balances at December 31, 2006 Change in accounting principles, net of tax Comprehensive income: Net income Other comprehensive income (loss), net of tax: Change in net unrealized securities losses Change in net unrealized derivatives losses Change in defined benefit... -

Page 111

... to benefits, claims, losses and settlement expenses, interest credited to fixed accounts and banking and deposit interest expense, respectively. The following table shows the impact of the reclassification made to the Company's previously reported Consolidated Statements of Operations: Year Ended... -

Page 112

...related hedge and tax effects, are included in accumulated other comprehensive income (loss). Revenues and expenses are translated at average exchange rates during the year. Amounts Based on Estimates and Assumptions Accounting estimates are an integral part of the Consolidated Financial Statements... -

Page 113

...Liabilities Separate account assets and liabilities are primarily funds held for the exclusive benefit of variable annuity contractholders and variable life insurance policyholders. The Company receives investment management fees, mortality and expense risk fees, guarantee fees and cost of insurance... -

Page 114

...fair value of derivatives hedging variable annuity living benefits, equity indexed annuities and stock market certificates are included within benefits, claims, losses and settlement expenses, interest credited to fixed accounts and banking and deposit interest expense, respectively. Changes in fair... -

Page 115

... value of stock market investment certificate embedded derivatives is included in customer deposits. The changes in fair value of the equity indexed annuity and investment certificate embedded derivatives are reflected in interest credited to fixed accounts and banking and deposit interest expense... -

Page 116

... make assumptions to project maintenance expenses associated with servicing the Company's annuity and insurance businesses during the DAC amortization period. The client asset value growth rates are the rates at which variable annuity and variable universal life insurance contract values invested... -

Page 117

... year of issue, with an average rate of approximately 5.8%. Life and Health Insurance Future policy benefits and claims related to life and health insurance include liabilities for fixed account values on fixed and variable universal life policies, liabilities for unpaid amounts on reported claims... -

Page 118

...products. Principal sources of revenue include management and financial advice fees, distribution fees, net investment income and premiums. Management and Financial Advice Fees Management and financial advice fees relate primarily to fees earned from managing mutual funds, separate account and wrap... -

Page 119

...Distribution fees also include amounts received under marketing support arrangements for sales of mutual funds and other companies' products, such as through the Company's wrap accounts, as well as surrender charges on fixed and variable universal life insurance and annuities. Net Investment Income... -

Page 120

.... The Company is currently evaluating the impact of SFAS 160 on its consolidated results of operations and financial condition. In September 2006, the FASB issued SFAS No. 158, ''Employers' Accounting for Defined Benefit Pension and Other Postretirement Plans-an Amendment of FASB Statements No... -

Page 121

... and liabilities for future policy benefits by $9 million. The after-tax decrease to retained earnings for these changes was $134 million. 4. Separation and Distribution from American Express Ameriprise Financial was formerly a wholly owned subsidiary of American Express Company (''American Express... -

Page 122

...Express. Ameriprise Bank acquired $493 million of customer loans and $963 million of customer deposits and received net cash of $470 million. The assets acquired and liabilities assumed were recorded at fair value. Separately, in 2006, the Company purchased $33 million of secured loans from American... -

Page 123

...The following is a summary of investments: December 31, 2008 2007 (in millions) Available-for-Sale securities, at fair value Commercial mortgage loans, net Trading securities Policy loans Other investments Total Available-for-Sale Securities Available-for-Sale securities distributed by type were as... -

Page 124

..., 2008 and 2007, approximately 45% and 39%, respectively, of the securities rated AAA were GNMA, FNMA and FHLMC mortgage backed securities. No holdings of any other issuer were greater than 10% of shareholders' equity. The following tables provide information about Available-for-Sale securities with... -

Page 125

... in interest rates and credit spreads across sectors. The primary driver of increased unrealized losses during 2008 was the widening of credit spreads across sectors. A majority of the unrealized losses for the year ended December 31, 2008 related to corporate debt securities and mortgage backed... -

Page 126

...$ 73 (24) (5) $ 66 (14) (2) The $762 million of other-than-temporary impairments in 2008 primarily related to credit-related losses on non-agency residential mortgage backed securities, corporate debt securities primarily in the financial services and gaming industries and asset backed and other... -

Page 127

... first mortgages on real estate. The Company holds the mortgage documents, which gives it the right to take possession of the property if the borrower fails to perform according to the terms of the agreements. The balances of and changes in the allowance for loan losses were as follows: December 31... -

Page 128

... 5 - - $ 96 (15) (12) $ 92 (2) (1) $ 106 (30) 25 The total pretax impacts on the Company's revenues and expenses attributable to the review of valuation assumptions for products of RiverSource Life companies and the valuation system conversion for the year ended December 31, 2008 and the 105 -

Page 129

review of the valuation assumptions for products of RiverSource Life companies for the year ended December 31, 2007 and 2006 were as follows: Benefits, Claims, Losses, and Settlement Amortization Expenses of DAC (in millions) Pretax Benefit (Charge) Premiums Other Revenues Distribution Expenses... -

Page 130

... amortization expense for definite-lived intangible assets during the years ended December 31, 2008, 2007 and 2006 was $25 million, $27 million and $20 million, respectively. In 2008 and 2007, the Company had impairment charges of $8 million and $1 million, respectively, related to Asset Management... -

Page 131

... the death benefit liability related to individual fixed and variable universal life and term life insurance products. As a result, the Company typically retains and is at risk for, at most, 10% of each policy's death benefit from the first dollar of coverage for new sales of these policies, subject... -

Page 132

...annuity GMAB Other variable annuity guarantees Total annuities Variable universal life (''VUL'')/universal life (''UL'') insurance Other life, disability income and long term care insurance Auto, home and other insurance Policy claims and other policyholders' funds Total Separate account liabilities... -

Page 133

... exclusive benefit of those policyholders. The Company also offers term and whole life insurance as well as disability products. The Company no longer offers long term care products but has in force policies from prior years. Insurance liabilities include accumulation values, unpaid reported claims... -

Page 134

... the end of the 10 year period, a lump sum will be added to the contract value to make the contract value equal to the guarantee value. Certain universal life contracts offered by the Company provide secondary guarantee benefits. The secondary guarantee ensures that, subject to specified conditions... -

Page 135

...risks. Certain investment certificate products have returns tied to the performance of equity markets. The Company guarantees the principal for purchasers who hold the certificate for the full 52-week term and purchasers may participate in increases in the stock market based on the S&P 500 Index, up... -

Page 136

... structured entity supported by a $10 million portfolio of municipal bonds. The floating rate revolving credit borrowings at December 31, 2008 are non-recourse debt related to certain consolidated property funds. The debt is due in 2013 and will be extinguished with the cash flows from the sale... -

Page 137

... Ameriprise Financial 2008 Employment Incentive Equity Award Plan (the ''2008 Plan''), and the Amended Deferred Equity Program for Independent Financial Advisors (''P2 Deferral Plan''). In accordance with the Employee Benefits Agreement (''EBA'') entered into between the Company and American Express... -

Page 138

... are made in cash for which the Company has recorded a liability, or shares of the Company's common stock for the portion of the deferral invested in the Ameriprise Financial Stock Fund and the related Company match, for which the Company has recorded in equity. Compensation expense related to the... -

Page 139

... for Ameriprise Financial common stock upon the director's termination of service. The employee awards generally vest ratably over three to four years. Compensation expense for deferred share units and restricted stock units is based on the market price of Ameriprise Financial stock on the date of... -

Page 140

... market value of Ameriprise Financial common stock on the deferral date as defined by the plan. As independent financial advisors are not employees of the Company, the awards are expensed based on the stock price of the Company's common stock up to the vesting date. The share-based awards generally... -

Page 141

... capital of Ameriprise Bank, per Federal Deposit Insurance Corporation policy, should be sufficient to provide a Tier 1 capital to assets leverage ratio of not less than 8% throughout its first three years of operation. For purposes of completing the bank's regulatory reporting, the Office of Thrift... -

Page 142

...to market risk related to certain variable annuity riders are classified as Level 3. Consolidated Property Funds The Company records the fair value of the properties held by its consolidated property funds within other assets. The fair value of these assets is determined using discounted cash flows... -

Page 143

... 31, 2008 Level 2 Level 3 (in millions) Level 1 Total Assets Cash equivalents Available-for-Sale securities Trading securities Separate account assets Other assets Total assets at fair value Liabilities Future policy benefits and claims Customer deposits Other liabilities Total liabilities at... -

Page 144

...mortgage loans, net Policy loans Receivables Restricted and segregated cash Other investments and assets Financial Liabilities Future policy benefits and claims Investment certificate reserves Banking and brokerage customer deposits Separate account liabilities Debt and other liabilities Investments... -

Page 145

.... Variable annuity fixed sub-accounts classified as investment contracts and equity indexed annuities fair value is determined by discounting cash flows adjusted for policyholder and contractholder behavior and the Company's non-performance risk specific to these liabilities. Customer deposits The... -

Page 146

... employees receive payments at the time of retirement or termination under applicable labor laws or agreements. The components of the net periodic pension cost for all pension plans were as follows: Years Ended December 31, 2007 2006 (in millions) 2008 Service cost Interest cost Expected return... -

Page 147

... date as the Company's fiscal year-end balance sheet. 2008 (in millions) 2007 Benefit obligation, beginning of period Effect of eliminating early measurement date Service cost Interest cost Plan amendments Benefits paid Actuarial gain Curtailments Settlements Foreign currency rate changes Benefit... -

Page 148

...determined by each plan's investment committee. The asset classes typically include domestic and foreign equities, emerging market equities, domestic and foreign investment grade and high-yield bonds and domestic real estate. The Company's retirement plans expect to make benefit payments to retirees... -

Page 149

... include the Ameriprise Financial Stock Fund. The Company matches 100% of the first 3% of base salary an employee contributes on a pre-tax basis each pay period. The Company may also make annual discretionary variable match contributions, which replaced the discretionary profit sharing contributions... -

Page 150

... income related to investment management services and investment portfolio income excluding gains and losses on asset disposals, certain reorganization expenses, equity participation plan expenses and other non-recurring expenses. Compensation expense related to the employee profit sharing plan was... -

Page 151

.... Cash Flow Hedges The Company uses interest rate derivative products, primarily swaps and swaptions, to manage funding costs related to the Company's debt and fixed annuity business. The interest rate swaps are used to hedge the exposure to interest rates on the forecasted interest payments... -

Page 152

... rate risk related to various products and transactions of the Company. Certain annuity and investment certificate products have returns tied to the performance of equity markets. As a result of fluctuations in equity markets, the amount of expenses incurred by the Company related to equity indexed... -

Page 153

...effective tax rate for 2008 included $79 million in tax benefits related to changes in the status of current audits and closed audits, tax planning initiatives, and the finalization of prior year tax returns. The Company's effective tax rate for 2007 included a $16 million tax benefit related to the... -

Page 154

... tax assets: Liabilities for future policy benefits and claims Investment impairments and write-downs Deferred compensation Unearned revenues Net unrealized losses on Available-for-Sale securities Accrued liabilities Investment related Net operating loss and tax credit carryforwards Other Gross... -

Page 155

... of the Separation from American Express, the Company's life insurance subsidiaries will not be able to file a consolidated U.S. federal income tax return with the other members of the Company's affiliated group until 2010. The Company's tax allocation agreement with American Express (the ''Tax... -

Page 156

... to, the Company's mutual funds, annuities, insurance products, brokerage services, financial plans and other advice offerings; supervision of the Company's financial advisors; supervisory practices in connection with financial advisors' outside business activities; sales practices and supervision... -

Page 157

... date, approximately $0.85 per dollar NAV has been paid to investors by the Reserve Primary Fund. For several years, the Company has been cooperating with the SEC in connection with an inquiry into the Company's sales of, and revenue sharing relating to, other companies' real estate investment trust... -

Page 158

... prices for specific services provided. The Company reviews the transfer pricing rates periodically and makes appropriate adjustments to ensure the transfer pricing rates that approximate arm's length market prices remain at current market levels. Costs related to shared services are allocated to... -

Page 159

... expenses for services provided by the Advice & Wealth Management, Annuities and Protection segments. The Annuities segment provides variable and fixed annuity products of RiverSource Life companies to retail clients primarily distributed through the Company's affiliated financial advisors... -

Page 160

... income. The Company allocates certain non-recurring items, such as costs related to supporting RiverSource 2a-7 money market funds, expenses related to unaffiliated money market funds and restructuring charges for 2008, as well as separation costs for 2007 and 2006, to the Corporate segment. The... -

Page 161

...in the fourth quarter of 2008 primarily through selective reductions in employee headcount largely in areas other than in the Company's client service operations. The following table summarizes the Company's restructuring activity for 2008: (in millions) Liability balance at January 1 Restructuring... -

Page 162

..., except per share data) Net revenues Separation costs(2) Pretax income (loss) Net income (loss) Earnings (loss) per basic common share Earnings (loss) per diluted common share Weighted average common shares outstanding: Basic Diluted Cash dividends paid per common share Common share price: High Low... -

Page 163

...marketing affiliates such as Costco Wholesale Corporation, Delta Loyalty Management Services, Inc. and Ford Motor Credit Company. We sell these products through our auto and home subsidiary, IDS Property Casualty Insurance Company (doing business as Ameriprise Auto & Home Insurance). Cash Sales-Cash... -

Page 164

... their financial advisor. Investors in our wrap accounts generally pay an asset-based fee based on the assets held in their wrap accounts. These investors also pay any related fees or costs included in the underlying securities held in that account, such as underlying mutual fund operating expenses... -

Page 165

... Commission in Internal Control-Integrated Framework. Based on management's assessment and those criteria, we believe that, as of December 31, 2008, the Company's internal control over financial reporting is effective. Ernst & Young LLP , the Company's independent registered public accounting... -

Page 166

..., in accordance with the standards of the Public Company Accounting Oversight Board (United States), the 2008 consolidated financial statements of Ameriprise Financial, Inc., and our report dated March 2, 2009, expressed an unqualified opinion thereon. Minneapolis, Minnesota March 2, 2009 143 -

Page 167

...Managed Products of AEFC since April 2002. Prior thereto, he served as Senior Vice President and Head, Business Transformation, Global Financial Services of American Express from March 2001 until April 2002. William F. Truscott-President-U.S. Asset Management, Annuities and Chief Investment Officer... -

Page 168

... as Vice President-Business Planning and Communications for the Group President, Global Financial Services at American Express. Ms. Davey has more than 15 years of experience in marketing, business planning and corporate communications. John R. Woerner-President-Insurance and Chief Strategy Officer... -

Page 169

... Financial Officer and Controller, but also to all other employees of our company) and the Code of Business Conduct for the Members of the Board of Directors may be found by clicking the ''Corporate Governance'' link found on our Investor Relations website at ir.ameriprise.com. You may also access... -

Page 170

.... Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters. Information concerning the market for our common shares and our shareholders, and certain information concerning equity compensation plans, can be found in Part II, Item 5 of this Annual Report on Form... -

Page 171

...has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized. AMERIPRISE FINANCIAL, INC. (Registrant) Date: March 2, 2009 By /s/ WALTER S. BERMAN Walter S. Berman Executive Vice President and Chief Financial Officer POWER OF ATTORNEY KNOW ALL PERSONS BY THESE... -

Page 172

... 2, 2009 By /s/ RICHARD F. POWERS III Richard F. Powers III Director Date: March 2, 2009 By /s/ H. JAY SARLES H. Jay Sarles Director Date: March 2, 2009 By /s/ ROBERT F. SHARPE, JR. Robert F. Sharpe, Jr. Director Date: March 2, 2009 By /s/ WILLIAM H. TURNER William H. Turner Director 149 -

Page 173

Report of Independent Registered Public Accounting Firm The Board of Directors and Shareholders of Ameriprise Financial, Inc. We have audited the consolidated financial statements of Ameriprise Financial, Inc. as of December 31, 2008 and 2007, and for each of the three years in the period ended ... -

Page 174

AMERIPRISE FINANCIAL, INC. SCHEDULE I-CONDENSED FINANCIAL INFORMATION OF REGISTRANT (Parent Company Only) Table of Contents Condensed Statements of Operations Condensed Balance Sheets Condensed Statements of Cash Flows Notes to Condensed Financial Information of Registrant F-3 F-4 F-5 F-6 F-2 -

Page 175

... CONDENSED STATEMENTS OF OPERATIONS (Parent Company Only) Years Ended December 31, 2007 2006 (in millions) 2008 Revenues Management and financial advice fees Distribution fees Net investment income Other revenues Total revenues Banking and deposit interest expense Total net revenues Expenses... -

Page 176

...amounts applicable to equity investments in subsidiaries: Net unrealized securities losses Net unrealized derivatives losses Foreign currency translation adjustments Defined benefit plans Total accumulated other comprehensive loss Total shareholders' equity Total liabilities and shareholders' equity... -

Page 177

AMERIPRISE FINANCIAL, INC. SCHEDULE I-CONDENSED FINANCIAL INFORMATION OF REGISTRANT CONDENSED STATEMENTS OF CASH FLOWS (Parent Company Only) Years Ended December 31, 2008 2007 2006 (in millions) Cash Flows from Operating Activities Net income (loss) Adjustments to reconcile net income to net cash ... -

Page 178

... of a consolidated structured entity. 3. Commitments and Contingencies The Parent Company is the guarantor for an operating lease of IDS Property Casualty Insurance Company. All consolidated legal, regulatory and arbitration proceedings, including class actions of Ameriprise Financial, Inc. and... -

Page 179

.... Exhibits numbered 10.2 through 10.17 are management contracts or compensatory plans or arrangements. Exhibit Description 3.1 3.2 Amended and Restated Certificate of Incorporation of Ameriprise Financial, Inc. (incorporated by reference to Exhibit 3.1 to the Current Report on Form 8-K, File No... -

Page 180

...General Counsel and Principal Accounting Officer and any other officers designated by the Chief Executive Officer (incorporated by reference to Exhibit 10.29 of the Annual Report on Form 10-K, File No. 1-32525, filed on March 8, 2006). Ameriprise Financial 2008 Employment Incentive Equity Award Plan... -

Page 181

... reinvestment of dividends. Fiscal year ending December 31. The stock price performance included in this graph is not necessarily indicative of future price performance. Copyright ©2009 S&P, a division of The McGraw-Hill Companies Inc. All rights reserved. Ameriprise Financial 2008 Annual Report -

Page 182

...: Investor Relations 243 Ameriprise Financial Center Minneapolis, MN 55474. Stock Exchange Listing New York Stock Exchange Symbol: AMP Independent Registered Public Accounting Firm Ernst & Young LLP 220 South 6th Street, Suite 1400 Minneapolis, MN 55402 Transfer Agent Computershare Trust Company... -

Page 183

...cer Joseph E. Sweeney President Financial Planning, Products and Services William F. Truscott President U.S. Asset Management, Annuities and Chief Investment Ofï¬cer John R. Woerner President Insurance and Chief Strategy Ofï¬cer *Mr. Henderson is not an executive ofï¬cer of Ameriprise Financial... -

Page 184

ameriprise.com © 2009 Ameriprise Financial, Inc. All rights reserved. 400425 DE2/08) 400425 E (2/09)