Air New Zealand 2009 Annual Report Download - page 10

Download and view the complete annual report

Please find page 10 of the 2009 Air New Zealand annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

Investment revenue

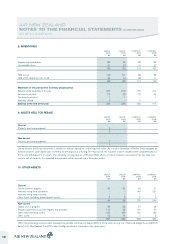

Dividend revenue is recognised when the right to receive payment is established.

Interest revenue from investments and fixed deposits is recognised as it accrues, using the effective interest method where appropriate.

CASH FLOWS

Cash flows are included in the Statement of Cash Flows net of Goods and Services Tax.

BORROWING COSTS

Borrowing costs directly attributable to the acquisition of qualifying assets, such as aircraft, are added to the cost of those assets until such time as the

assets are substantially ready for their intended use or sale. Qualifying assets are assets which necessarily take a substantial period of time to get ready

for their intended use. All other borrowing costs are recognised in the Statement of Financial Performance in the period in which they are incurred.

LEASE PAYMENTS

Operating leases

Leases under which a significant proportion of the risks and rewards of ownership are retained by the lessor are classified as operating leases. Payments

made under operating leases (net of any incentives received) are recognised as an expense in the Statement of Financial Performance on a straight-line

basis over the term of the lease.

Finance leases

Payments made under finance leases are apportioned between the finance expense and the reduction of the outstanding liability. The finance expense is

allocated to each period during the lease term so as to produce a constant periodic rate of interest on the remaining balance of the liability.

MAINTENANCE COSTS

The cost of major airframe inspections and engine overhauls for aircraft owned by the Group is capitalised and depreciated over the period to the next

expected inspection or overhaul.

Where there is a commitment to maintain aircraft held under operating lease arrangements, a provision is made during the lease term for the lease return

obligations specified within those lease agreements. The provision is based upon historical experience, manufacturers’ advice and, where appropriate,

contractual obligations in determining the present value of the estimated future costs of major airframe inspections and engine overhauls by making

appropriate charges to the Statement of Financial Performance, calculated by reference to the number of hours or cycles operated during the year.

All other maintenance costs are expensed as incurred.

FINANCIAL INSTRUMENTS

Non-derivative financial instruments

Non-derivative financial instruments include cash and cash equivalents, other interest-bearing assets, trade and other receivables, interest-bearing

liabilities and trade and other payables. These are recognised initially at fair value plus any attributable transaction costs. Subsequent to initial recognition,

non-derivative financial instruments are recognised as described below.

Loans and receivables:

Cash and cash equivalents

Cash and cash equivalents include cash on hand, demand deposits, current accounts in banks net of overdrafts and other short-term highly liquid

investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value.

Trade and other receivables

Trade and other receivables are recognised at cost less any provision for impairment. A provision for impairment is established when collection is

considered to be doubtful. When a trade receivable is considered uncollectible, it is written-off against the provision.

Financial liabilities at amortised cost:

Borrowings

Borrowings are initially recognised at fair value, net of transaction costs incurred. Borrowings are subsequently stated at amortised cost using the

effective interest rate method, where appropriate. Borrowings are classified as current liabilities unless the Group has an unconditional right to defer

settlement of the liability for more than 12 months after the balance sheet date.

Finance leases

Finance lease obligations are initially stated at fair value, net of transaction costs incurred. The obligations are subsequently stated at amortised cost.

AIR NEW ZEALAND

STATEMENT OF ACCOUNTING POLICIES (CONTINUED)

FOR THE YEAR TO 30 JUNE 2009

8