TomTom 2010 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2010 TomTom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

p 66 / TomTom Annual Report and Accounts 2010

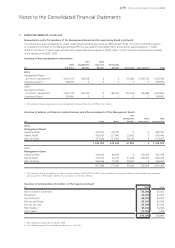

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

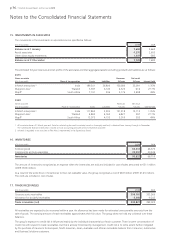

Share premium

The share premium represents the amount by which the fair value of the consideration received exceeds the nominal value of shares

issued. Incremental costs directly attributable to the issue of new shares or options are shown in equity as a deduction, net of tax, from

the proceeds.

Provisions

Provisions are recognised when the group has a present obligation as a result of a past event and it is probable that the group will be

required to settle that obligation. Provisions are measured at management’s best estimate of the expenditure required to settle the

obligation at the balance sheet date, and are discounted to present value where the effect is material.

Provisions for warranty costs are recognised at the date of sale of the relevant products, at management’s best estimate of the expenditure

required to settle the group’s obligation. Warranty costs are recorded within cost of sales.

Other provisions are recorded for probable liabilities that can be reasonably estimated. The provisions include legal claims and tax risks

for which it is probable that an outflow of resources will be required to settle the obligation.

Borrowings

Borrowings are recognised initially at fair value, net of transaction costs incurred. Subsequently, amounts are stated at amortised cost with

the difference being recognised in the income statement over the period of the borrowings using the effective interest rate method.

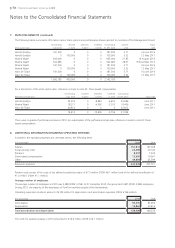

3. FINANCIAL RISK MANAGEMENT

The business risk report included in this annual report, contains auditable parts comprising ‘Credit’, ‘Liquidity’, ‘Loan covenants’, ‘Foreign

currencies’ and ‘Interest rates’. Management policies have been established to identify, analyse and monitor these risks, and to set

appropriate risk limits and controls. Financial risk management is carried out in accordance with the Treasury policy which has been

approved by the Supervisory Board. The written principles and policies are reviewed periodically to reflect changes in market conditions

and the activities of the business.

Capital risk management

The group’s financing policy aims to maintain a capital structure which enables the group to achieve its strategic objectives and daily

operational needs, and to safeguard the group’s ability to continue as a going concern.

In order to maintain or adjust the capital structure, the group may issue new shares, adjust its dividend policy, return capital to

shareholders or sell assets to reduce debt.

With respect to debt financing, the group focuses on interest cover and leverage. Net debt is calculated as total borrowings less cash

and cash equivalents plus our financial lease commitments.

Further quantitative disclosures are included throughout these Consolidated Financial Statements and/or in the business risk report.

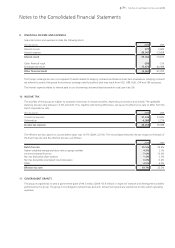

4. CRITICAL ACCOUNTING ESTIMATES AND JUDGEMENTS

The group makes estimates and assumptions concerning the future. The resulting accounting estimates will, by definition, seldom equal

the related actual results. The estimates and assumptions that have a significant risk of causing a material adjustment to the carrying

amounts of assets and liabilities within the next financial year are discussed below.

a) Revenue recognition

When returns are probable, an estimate is made of the expected financial impact of these returns. The estimate is based upon

historical data on the return rates and information on the inventory levels in the distribution channel. The estimated probable returns

are recorded as a direct deduction from revenue and cost of sales.

The group reduces revenue for estimates of sales incentives. We offer sales incentives, including channel rebates and end-user rebates

for our products. The estimate is based on our historical experience taking into account future expectations on rebate payments.

If there is excess stock at retailers when a price reduction becomes effective, the group will compensate its customers on the price

difference for their existing stock. Customers are eligible for compensation if certain criteria are met. To reflect the costs related to

known price reductions in the income statement, an accrual is created against revenue.

Multiple Deliverable Arrangements (MDA) require TomTom to deliver hardware and/or a number of services under one agreement

and/or a number of services under one agreement which is commercially linked. Revenue recognition must be determined separately

for each of the deliverables identified, and for that purpose TomTom must attribute a reliable fair value to each deliverable. IFRS

permits the use of a combination of estimation and allocation methods if that combination best reflects a transaction’s substance.

The absence of a reliable fair value for any of the deliverables indicates that the goods and services do not operate independently.

In this situation, the whole revenue is allocated over the subscription period.

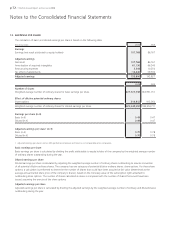

Notes to the Consolidated Financial Statements