TomTom 2010 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2010 TomTom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

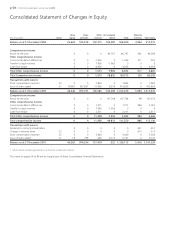

p 64 / TomTom Annual Report and Accounts 2010

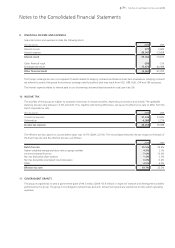

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Intangible assets other than goodwill (continued)

Internally generated intangible assets (continued)

The group is required to use estimates, assumptions and judgements to determine the expected useful lives and future economic benefits

of these costs. Such estimates are made on a regular basis, or as appropriate throughout the year, as they can be significantly affected by

changes in technology and other factors.

All expenditures on research activities are expensed in the income statement as incurred. Internal software costs relating to development

of non-core software with an estimated average useful life of less than one year and engineering cost relating to the detailed

manufacturing design of new products are expensed in the period in which they are incurred.

Acquired intangible assets

Definite-lived intangible assets acquired separately or through a business combination are initially recognised at cost. The cost of assets

acquired separately includes the purchase price and directly attributable costs to bring the asset to its intended use. Intangible assets

acquired in a business combination are identified and recognised separately from goodwill where they satisfy the definition of an

intangible asset and their fair values can be measured reliably. The cost of such intangible assets is their fair value at the acquisition date.

Subsequent to initial recognition, these intangible assets are carried at cost less accumulated amortisation and accumulated impairment

losses.

The estimated useful lives of the intangible assets are as follows:

Databases and tools 10-20 years

Customer relationships 20-27 years

Computer software 2-5 years

Acquired technology 4-5 years

Customer relationships include customers for Tele Atlas maps; there is a high cost to change map providers and historically there is high

customer retention.

Property, plant and equipment

Property, plant and equipment are stated at historical cost less accumulated depreciation and impairment charges. Depreciation is recorded

on a straight-line basis over the estimated useful lives of the assets as follows:

Furniture and fixtures 4-10 years

Computer equipment and hardware 2-4 years

Vehicles 4 years

Tools and moulds 1-2 years

The costs of tools and moulds used to manufacture the group’s products are capitalised within property, plant and equipment, and

depreciated over their estimated useful lives.

The estimated useful lives, residual values and depreciation methods are reviewed at each year-end, with the effect that any changes in

estimate are accounted for on a prospective basis.

The gain or loss arising on disposal or retirement of an item of property, plant and equipment is determined as the difference between

the sales proceeds and the carrying amount of the asset and is recognised in profit or loss.

Impairment of tangible and intangible assets

Assets, such as goodwill, that have an indefinite useful life are not subject to amortisation and are tested annually for impairment. Assets

that are subject to amortisation are reviewed for impairment whenever events or changes in circumstances indicate that the carrying

amount may not be recoverable. An impairment loss is recognised for the amount by which the asset’s carrying amount exceeds its

recoverable amount.

The recoverable amount is the higher of an asset’s fair value, less costs to sell and value in use. In estimating the fair value less costs to

sell, the estimated future cash flows are discounted to their present value, using a post-tax discount rate that reflects current market

assessments of the time-value of money and the risks specific to the asset for which the estimates of future cash flows have not been adjusted.

For the purposes of assessing impairment, assets are grouped at the lowest levels for which there are separately identifiable cash flows

(cash-generating units).

An impairment loss is recognised immediately in the income statement, unless the relevant asset is carried at a revalued amount, in which

case the impairment loss is treated as a revaluation decrease.

Non-financial assets, other than goodwill that suffered an impairment, are reviewed for possible reversal of the impairment at each

reporting date.

Notes to the Consolidated Financial Statements