Suzuki 2001 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2001 Suzuki annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

|

|

SUZUKI MOTOR CORPORATION● 29

Millions of

yen

6.Reserve for retirment allowance

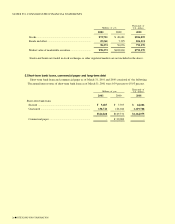

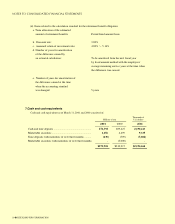

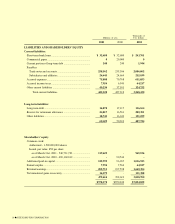

(a). Outline of an adopted retirement benefit system

In the case of the Company, as a defined benefit plan, Employee Pension Fund, Approved Retirement

Annuity System and Termination Allowance Plan are established.

(b). Items related to a retirement benefit obligation (as of March 31, 2001)

Remarks:1). The part of employees' pension plan is included in the figures written down above. In

connection with the amendment of the Welfare Pension Insurance Law in 2000, the raising of

the age for the start of payment is studied concerning the partial part carried out for the

employees' pension fund and therefore decrease takes place of the liability for the service in

the past by 8,792 million yen from next fiscal year.

2). The premium retirement allowance paid on a temporary basis is not included.

3). Some of subsidiaries adopt simplified methods for the calculation of retirement benefits.

(c). Items related to retirement benefit cost (as of March 31, 2001)

Remarks:1). The amount of employees' contribution to employees' pension fund is deducted.

2). The retirement benefit cost of subsidiaries where simplified methods are adopted is accounted

for "a. Service cost".

a. Service cost ¥ 7,872 $ 63,538

b. Interest cost 4,854 39,182

c. Assumed return on investment (4,975) (40,161)

d. The amount of difference to be amortized, which was 10,779 87,000

caused at the time when the accounting standard was

changed

e. Retirement benefit cost (a+b+c+d) ¥18,530 $149,560

Thousands of

U.S. dollars

Millions of

yen

a. Retirement benefit obligation ¥(227,411) $(1,835,443)

b. Pension assets 130,294 1,051,613

c. Unrecognized retirement benefit obligation (a + b) ¥ (97,116) $ (783,830)

d. Non-amortized amount of difference caused at the 43,117 348,000

time of alteration of an accounting standard

e. Unrecognized difference by an actuarial calculation 17,028 137,436

f. Reserve for retirement allowance (c+d+e) ¥ (36,970) $ (298,392)

Thousands of

U.S. dollars

*ANNUAL REPORT2001/14のコピー 2