Freddie Mac 2014 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2014 Freddie Mac annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

|

|

8Freddie Mac

certain “high-cost” areas (currently, up to $625,500 for a one-family residence). Higher limits also apply to two- to four-family

residences and to mortgages secured by properties in Alaska, Guam, Hawaii, and the U.S. Virgin Islands.

Our charter permits us to purchase first-lien single-family mortgages with LTV ratios at the time of our purchase of less

than or equal to 80%. Our charter also permits us to purchase first-lien single-family mortgages that do not meet this criterion if

we have one of the following credit protections:

• mortgage insurance on the portion of the UPB of the mortgage that exceeds 80%;

• a seller’s agreement to repurchase or replace any mortgage that has defaulted; or

• retention by the seller of at least a 10% participation interest in the mortgage.

This charter requirement does not apply to multifamily mortgages or to mortgages that have the benefit of any guarantee,

insurance or other obligation by the U.S. or any of its agencies or instrumentalities (e.g., the FHA, the VA or the USDA Rural

Development). Additionally, as part of HARP, we purchase single-family mortgages that refinance mortgages we currently own

or guarantee without obtaining additional credit enhancement in excess of that already in place for any such loan, even when

the LTV ratio of the new loan is above 80%.

Overview of the Mortgage Securitization and Guarantee Process

Mortgage securitization is an integral part of our business activities. Mortgage securitization is a process where we

purchase mortgage loans that lenders originate, and then pool these loans into mortgage-related securities that can be sold in

global capital markets. Our primary single-family mortgage securitization and guarantee process involves the issuance of

single-class PCs and our primary multifamily mortgage securitization and guarantee process involves the issuance of K

Certificates. We also resecuritize mortgage-related securities that are issued by us, other GSEs, HFAs, or private (non-agency)

entities, and issue other single-class and multiclass mortgage-related securities to third-party investors.

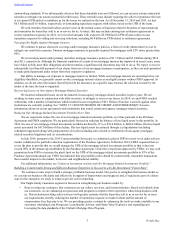

The following diagram illustrates how we support mortgage market liquidity when we create PCs through mortgage

securitizations. PCs can be sold to investors or held by us or our lender customers.

Mortgage Securitizations

For single-family loans, our securitization and guarantee process generally works as follows: (a) a lender originates a

mortgage loan to a borrower purchasing a home or refinancing an existing mortgage loan; (b) we purchase the loan from the

lender and place it with other mortgages into a security (this process is referred to as “pooling”); (c) we provide a credit

guarantee (for a fee) to those who invest in the security; (d) the borrower’s monthly payment of mortgage principal and interest

(net of a servicing fee and our management and guarantee fee) is passed through to the investors; and (e) if the borrower stops

making monthly payments, we make the applicable payments to the investors pursuant to our guarantee.

The terms of single-family mortgage loans that we purchase allow borrowers to prepay them, thereby allowing borrowers

to refinance their loans. Because of the nature of long-term, fixed-rate mortgage loans, borrowers with these loans are protected

against rising interest rates, but are able to take advantage of declining rates through refinancing. When a borrower prepays a

mortgage loan that we have securitized, the outstanding balance of the security owned by investors is reduced by the amount of

the prepayment.

We issue mortgage-related securities in the form of PCs, REMICs and Other Structured Securities, and Other Guarantee

Transactions. Each of these types of mortgage-related securities is discussed below.

Table of Contents