Carphone Warehouse 2003 Annual Report Download - page 6

Download and view the complete annual report

Please find page 6 of the 2003 Carphone Warehouse annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

The Group achieved a strong result for the year despite a

handset market that recorded a second consecutive year of

declines. Revenues, profits and earnings per share all grew

significantly and the Group generated encouraging levels of

free cash flow. The quality of earnings also improved, with

nearly half of Group contribution being derived from our

recurring revenue businesses.

Group turnover for the period was £1,841.5m compared

with £1,152.7m for the prior year. We achieved growth in

turnover across all our businesses. Excluding our Wholesale

business, which grew turnover from £343.0m to £806.6m,

and the acquisition of Opal Telecom, underlying growth in

turnover was 18.4%.

The principal acquisition during the year was the purchase

of Opal Telecom plc, a provider of value-added fixed line

telecoms services to business customers, for an initial

consideration of £67.6m, with up to a further £18.0m

payable over two years subject to performance. Opal has

generated a contribution of £8.3m on turnover of £75.9m

since acquisition.

Pre-tax profits for the Group, before exceptional items and

goodwill amortisation, were £57.0m, an increase of 21.8%

on the year to March 2002. Earnings per share on the same

basis grew by 19.0% to 5.25p.

Free cash flow, before the acquistion of Opal, the sale

of our London offices and investment in new stores, was

£50.8m (2002: £0.5m).

Two exceptional items arose during the year. We generated

an exceptional profit of £13.2m on the sale for cash of the

freehold on our London offices for £36.6m. We also incurred

a further non-cash writedown of £15.1m to the carrying

value of the investments in our wireless investment portfolio.

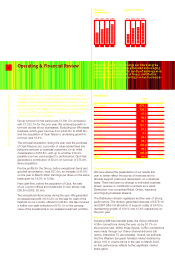

Operating & Financial Review Revenues, profits and earnings per share all grew

significantly and the Group generated encouraging

levels of free cash flow. The quality of earnings also

improved, with nearly half of Group contribution

being derived from our recurring revenue businesses.

Distribution

2003 2002

£m £m

Turnover 876.1 742.4

Retail 738.3 623.2

Online 41.9 36.7

Insurance 66.8 60.5

Ongoing 29.1 22.0

Contribution 121.7 109.1

Retail 67.2 60.2

Online 3.4 5.1

Insurance 22.0 21.8

Ongoing 29.1 22.0

Support costs (52.4) (47.7)

EBITDA 69.3 61.4

Depreciation (25.3) (22.4)

EBIT 44.0 39.0

Before amortisation of goodwill and exceptional items.

Divisional performance

We have altered the presentation of our results this

year to better reflect the source of revenues and to

allocate support costs and depreciation on a divisional

basis. There has been no change to individual business

stream revenue or contribution numbers as a result.

Distribution now comprises Retail, Online, Insurance

and Ongoing business streams.

The Distribution division registered another year of strong

performance. The division generated revenues of £876.1m

and EBIT (after full allocation of support costs) of £44.0m,

representing growth of 18.0% and 12.8% respectively on

the prior year.

Retail and Online

Including SIM-free handset sales, the Group achieved

4.36m connections during the year, up by 20.7% on

the previous year. Within these figures, 0.26m connections

were made through our Online channel (inbound call

centre, interactive TV and website). Overall, we estimate

that the Western European handset market declined by

about 10% in volume terms in the year to March 2003,

so this performance reflects further significant market

share gains.

4

The Carphone Warehouse Group PLC Annual Report 2003

568 763 810 1,035

02 030100

Revenue

(ex wholesale)

(£m)

41.4 66.0 72.8 90.0

02 030100

Headline EBITDA

(£m)