Aetna 2009 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2009 Aetna annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

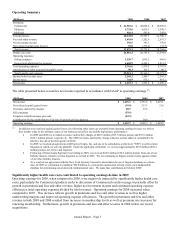

Interest expense on our debt was $243 million, $236 million and $181 million for 2009, 2008 and 2007, respectively.

The increase in interest expense in 2009 and 2008 was due to higher overall average long-term debt levels as a result

of our issuance of senior notes in September 2008 and December 2007.

Refer to Note 14 of Notes to Consolidated Financial Statements on page 75 for additional information on our short-

term and long-term debt.

Restrictions on Certain Payments

In addition to general state law restrictions on payments of dividends and other distributions to shareholders applicable

to all corporations, HMOs and insurance companies are subject to further regulations that, among other things, may

require those companies to maintain certain levels of equity (referred to as surplus) and restrict the amount of

dividends and other distributions that may be paid to their equity holders. These regulations are not directly applicable

to Aetna as a holding company, since Aetna is not an HMO or an insurance company. The additional regulations

applicable to our HMO and insurance company subsidiaries are not expected to affect our ability to service our debt,

meet our other financing obligations or pay dividends, or the ability of any of our subsidiaries to service other

financing obligations, if any. Under regulatory requirements, at December 31, 2009, the amount of dividends that our

insurance and HMO subsidiaries could pay to Aetna without prior approval by regulatory authorities was

approximately $1.2 billion in the aggregate.

We maintain capital levels in our operating subsidiaries at or above targeted and/or required capital levels and dividend

amounts in excess of these levels to meet our liquidity requirements, including the payment of interest on debt and

shareholder dividends. In addition, at our discretion, we use these funds for other purposes such as funding share

repurchase programs, investments in new businesses and other purposes we consider necessary.

Off-Balance Sheet Arrangements

We do not have guarantees or other off-balance sheet arrangements that we believe, based on historical experience and

current business plans, are reasonably likely to have a material impact on our current or future results of operations,

financial condition or cash flows. Refer to Notes 8 and 18 of Notes to Consolidated Financial Statements beginning on

page 58 and 77, respectively, for additional detail of our variable interest entities and guarantee arrangements,

respectively, at December 31, 2009.

Ratings

As of February 25, 2010, the credit ratings of Aetna and Aetna Life Insurance Company (“ALIC”) from the

respective nationally recognized statistical rating organizations (“Rating Agencies”) were as follows:

Moody's Investors Standard

A.M. Best Fitch Service & Poor's

Aetna (senior debt)

(1)

bbb+ A- A3 A-

Aetna (commercial paper) AMB-2 F1 P-2 A-2

ALIC (financial strength)

(1)

A AA- Aa3 A+

(1) Aetna’ s senior debt and ALIC’ s financial strength have a stable outlook from A.M. Best and a negative outlook from Fitch and

Standard & Poor’ s. Moody’ s Investors Service has placed Aetna’ s senior debt and ALIC’ s financial strength ratings under review for

possible downgrade.

Solvency Regulation

The National Association of Insurance Commissioners (the “NAIC”) utilizes risk-based capital (“RBC”) standards for

insurance companies that are designed to identify weakly-capitalized companies by comparing each company’ s

adjusted surplus to its required surplus (“RBC Ratio”). The RBC Ratio is designed to reflect the risk profile of

insurance companies. Within certain ratio ranges, regulators have increasing authority to take action as the RBC Ratio

decreases. There are four levels of regulatory action, ranging from requiring insurers to submit a com-prehensive plan

to the state insurance commissioner to requiring the state insurance commissioner to place the insurer under regulatory

control. At December 31, 2009, the RBC Ratio of each of our primary insurance sub-sidiaries was above the level that

would require regulatory action. The RBC framework described above for insurers has been extended by the NAIC to

health organizations, including HMOs. Although not all states had adopted these rules at December 31, 2009, at that

date, each of our active HMOs had a surplus that exceeded either the applicable state net worth requirements or, where

adopted, the levels that would require regulatory action under the NAIC’ s RBC rules. External rating agencies use

their own RBC standards when they determine a company’ s rating.

Annual Report – Page 15