Abercrombie & Fitch 1999 Annual Report Download - page 10

Download and view the complete annual report

Please find page 10 of the 1999 Abercrombie & Fitch annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21

|

|

most merchandise categories. In addition, buying and occu-

pancy costs, expressed as a percentage of net sales, declined

slightly due to leverage achieved from comparable store sales

increases. The Company also improved the gross income rate

through reduced freight costs and enhanced store inventory

control procedures which reduced shrink cost.

In 1998, the gross income rate increased to 42.2% from 38.5%

in 1997. The improvement was the result of higher merchan-

dise margins, expressed as a percentage of net sales due to

higher IMU across most major merchandise categories and a

lower markdown rate. In addition, buying and occupancy

costs, expressed as a percentage of net sales, declined due to

leverage achieved from comparable store sales increases.

GENERAL, ADMINISTRATIVE AND STORE OPERATING

EXPENSES General, administrative and store operating

expenses, expressed as a percentage of net sales, were 17.9% in

the fourth quarter of 1999 and 16.9% in the comparable period

in 1998. The increase in the rate was primarily due to a change

in the accounting for gift certificates. Excluding the impact of

the accounting change, the rate would have improved com-

pared to last year primarily due to lower compensation expenses

related to management bonuses and restricted stock grants

awarded to key executives of the Company. Additionally, the

Company did not incur expenses related to service agreements

with The Limited, Inc. that expired prior to the fourth quarter

of 1999 and emphasized tighter expense control in travel, relo-

cation and legal expenses.

General, administrative and store operating expenses for

the year, expressed as a percentage of net sales, were 21.4%,

21.7% and 22.4% in 1999, 1998 and 1997. The improvement

during the three-year period resulted from management’s

continued emphasis on expense control and favorable lever-

aging of expenses due to higher sales volume. The 1998

improvement was offset by compensation expense associated

with restricted stock grants of approximately $11.5 million.

OPERATING INCOME Operating income, expressed as a per-

centage of net sales, was 34.1%, 32.4% and 27.9% for the fourth

quarter of 1999, 1998 and 1997 and 23.2%, 20.5% and 16.1% for

fiscal years 1999, 1998 and 1997. The improvement was the

result of higher gross income coupled with lower general, admin-

increase in comparable store sales and sales attributable to new

and remodeled stores. Comparable store sales increases were strong

in both the men’s and women’s businesses and across all geographic

regions of the country. The A&F Quarterly accounted for 2.0% of

net sales in the fourth quarter of 1998 as compared to 1.7% in 1997.

Net sales for 1999 increased 28% to $1.04 billion from $815.8

million a year ago. Sales growth resulted from a comparable

store sales increase of 10% and the addition of 54 new stores.

Comparable store sales increases were driven by both men’s and

women’s knits and pants. Net retail sales per gross square foot for

the Company increased 6%, principally from an increase in the

number of transactions per store. The Company’s catalogue, the

A&F Quarterly and the Company’s website represented 2.6% of

1999 net sales compared to 1.8% last year.

Net sales for 1998 increased 56% to $815.8 million over the same

period in 1997. The sales increase was attributable to the net

addition of 40 stores and a 35% comparable store sales increase.

Comparable store sales increases were equally strong in both

men’s and women’s businesses and their performance strength was

broadly based across all major merchandise categories. Net retail

sales per gross square foot for the Company increased 28%, driven

principally by an increase in the number of transactions per store.

GROSS INCOME Gross income, expressed as a percentage of

net sales, increased to 51.9% for the fourth quarter of 1999 from

49.3% for the same period in 1998. The increase was attributable

to higher merchandise margins (representing gross income before

the deduction of buying and occupancy costs), resulting from

higher initial markups (IMU), and improved control of store

inventory shrinkage and merchandise freight costs. The Company

also achieved some leverage in buying and occupancy costs,

expressed as a percentage of net sales.

For the fourth quarter of 1998, gross income, expressed as a

percentage of net sales, increased to 49.3% from 45.4% for the

same period in 1997. The increase was attributable to significant

leverage in buying and occupancy costs, expressed as a percent-

age of net sales associated with increased comparable store sales.

Merchandise margins improved primarily due to a lower mark-

down rate as the Company efficiently managed inventories.

For the year, the gross income rate increased to 44.7% in 1999

from 42.2% in 1998. Merchandise margins, expressed as a per-

centage of net sales, increased due to slightly higher IMU across

RESULTS OF OPERATIONS Net sales for the fourth quarter

were $367.9 million, an increase of 21% from $304.6 million

for the fourth quarter a year ago. Operating income was $125.3

million, up 27% compared to $98.7 million last year. Net income

per diluted share was $.73, up 30% from $.56 last year.

Net sales for the fiscal year ended January 29, 2000, increased

28% to $1.04 billion from $815.8 million last year. Operating

income for the year increased 45% to $242.1 million from $167.0

million in 1998. Net income per diluted share was $1.39 com-

pared to $.96 a year ago, an increase of 45%.

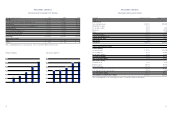

FINANCIAL SUMMARY The following summarized financial

data compares the 1999 fiscal year to the comparable periods

for 1998 and 1997:

% Change

1999- 1998-

1999 1998 1997 1998 1997

Net sales (millions) $1,042.1 $815.8 $521.6 28% 56%

Increase in comparable store sales 10% 35% 21%

Retail sales increase attributable

to new and remodeled stores,

magazine, catalogue and website 18% 21% 34%

Retail sales per average

gross square foot $0,512 $0,483 $0,376 6% 28%

Retail sales per average store

(thousands) $4,550 $4,551 $3,653 – 25%

Average store size at year-end

(gross square feet) 8,695 9,140 9,755 (5%) (6%)

Gross square feet at year-end

(thousands) 2,174 1,791 1,522 21% 18%

Number of stores

Beginning of year 196 156 127

Opened 54 41 30

Closed (–)(1) (1)

End of year 250 196 156

NET SALES Net sales for the fourth quarter of 1999 increased

21% to $367.9 million from $304.6 million in 1998. The increase

was primarily due to the addition of new stores and a comparable

store sales increase of 3%. Comparable store increases were driven

by men’s pants and knits while the women’s knit business was very

strong. The Company’s catalogue, the A&F Quarterly, a cata-

logue/magazine, and the Company’s website accounted for 3.4% of

net sales in the fourth quarter of 1999 as compared to 2.0 % last year.

Fourth quarter 1998 net sales as compared to net sales for the

fourth quarter 1997 increased 44% to $304.6 million, due to a 26%

15

Abercrombie &Fitch Co.

14

MANAGEMENT’S DISCUSSION AND ANALYSIS

Abercrombie &Fitch Co.

istrative and store operating expenses, expressed as a percentage

of net sales. Sales volume and gross income have increased at a

faster rate than general, administrative and store operating

expenses as the Company continues to emphasize cost controls.

INTEREST INCOME/EXPENSE Net interest income was $2.5

million in the fourth quarter of 1999 and $7.3 million for all of

1999 compared with net interest income of $1.6 million and $3.1

million for the corresponding periods last year. Net interest

income in 1999 and 1998 was primarily from short-term invest-

ments. Net interest expense in 1997 included $975 thousand per

quarter associated with $50 million of long-term debt that was

repaid during the first quarter of 1998, offset by interest income

on short-term investments.

FINANCIAL CONDITION The Company’s continuing growth

in operating income provides evidence of financial strength

and flexibility. A more detailed discussion of liquidity, capital

resources and capital requirements follows.

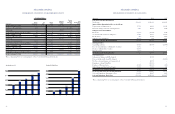

LIQUIDITY AND CAPITAL RESOURCES Cash provided by

operating activities provides the resources to support operations,

including seasonal requirements and capital expenditures. A

summary of the Company’s working capital position and cap-

italization follows (thousands):

1999 1998 1997

Working capital $162,351 $095,890 $ 42,000

Capitalization:

Long-term debt – – $ 50,000

Shareholders’ equity $311,094 $186,105 58,775

Total capitalization $311,094 $186,105 $108,775

The Company considers the following to be measures of

liquidity and capital resources:

1999 1998 1997

Current ratio (current assets divided

by current liabilities) 2.18 1.78 1.63

Debt-to-capitalization ratio (long-term debt

divided by total capitalization) n/a n/a 46%

Cash flow to capital investment

(net cash provided by operating

activities divided by capital expenditures) 183% 413% 340%

n/a=not applicable