Xcel Energy 2000 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2000 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40

|

|

62

XCEL ENERGY INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Plant Decommissioning

Decommissioning of NSP-Minnesota’s nuclear facilities is planned for the years 2010–2022, using the prompt dismantlement method. We are currently

following industry practice by ratably accruing the costs for decommissioning over the approved cost recovery period and including the accruals in Utility

Plant – Accumulated Depreciation. Consequently, the total decommissioning cost obligation and corresponding assets currently are not recorded in Xcel

Energy’s financial statements.

The FASB has proposed new accounting standards that, if approved, would require the full accrual of nuclear plant decommissioning and other site exit

obligations no sooner than 2002. Using Dec. 31, 2000, estimates, adoption of the proposed accounting would result in the recording of the total discounted

decommissioning obligation of $838 million as a liability, with the corresponding costs capitalized as plant and other assets and depreciated over the

operating life of the plant. We have not yet determined the potential impact of the FASB’s proposed changes in the accounting for site exit obligations,

such as costs of removal, other than nuclear decommissioning. However, the ultimate decommissioning and site exit costs to be accrued are expected to

be similar to the current methodology. The effects of regulation are expected to minimize or eliminate any impact on operating expenses and results of

operations from this future accounting change.

Consistent with cost recovery in utility customer rates, we record annual decommissioning accruals based on periodic site-specific cost studies and a

presumed level of dedicated funding. Cost studies quantify decommissioning costs in current dollars. Funding presumes that current costs will escalate in

the future at a rate of 4.5 percent per year. The total estimated decommissioning costs that will ultimately be paid, net of income earned by external trust

funds, is currently being accrued using an annuity approach over the approved plant recovery period. This annuity approach uses an assumed rate of

return on funding, which is currently 5.5 percent, net of tax, for external funding and approximately 8 percent, net of tax, for internal funding.

The MPUC last approved NSP-Minnesota’s nuclear decommissioning study and related nuclear plant depreciation capital recovery request in April 2000,

using 1999 cost data. Although we expect to operate Prairie Island through the end of each unit’s licensed life, the approved capital recovery would allow for

the plant to be fully depreciated, including the accrual and recovery of decommissioning costs, in 2007. This is about seven years earlier than each unit’s

licensed life. The approved recovery period for Prairie Island has been reduced because of the uncertainty regarding used fuel storage. We believe future

decommissioning cost accruals will continue to be recovered in customer rates.

The total obligation for decommissioning currently is expected to be funded 100 percent by external funds, as approved by the MPUC. Contributions to the

external fund started in 1990 and are expected to continue until plant decommissioning begins. The assets held in trusts as of Dec. 31, 2000, primarily

consisted of investments in fixed-income securities, such as tax-exempt municipal bonds and U.S. government securities that mature in 1 to 20 years, and

common stock of public companies. We plan to reinvest matured securities until decommissioning begins.

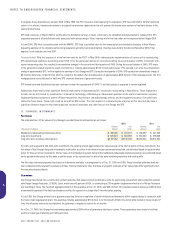

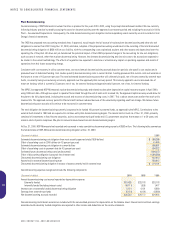

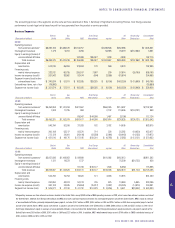

At Dec. 31, 2000, NSP-Minnesota had recorded and recovered in rates cumulative decommissioning accruals of $583 million. The following table summarizes

the funded status of NSP-Minnesota’s decommissioning obligation at Dec. 31, 2000:

(Thousands of dollars) 2000

Estimated decommissioning cost obligation from most recently approved study (1999 dollars) $ 958,266

Effect of escalating costs to 2000 dollars (at 4.5 percent per year) 41,685

Estimated decommissioning cost obligation in current dollars 999,951

Effect of escalating costs to payment date (at 4.5 percent per year) 894,322

Estimated future decommissioning costs (undiscounted) 1,894,273

Effect of discounting obligation (using risk-free interest rate) (1,056,360)

Discounted decommissioning cost obligation 837,913

Assets held in external decommissioning trust 563,812

Discounted decommissioning obligation in excess of assets currently held in external trust $ 274,101

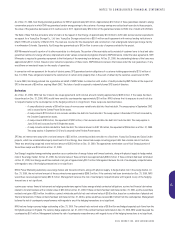

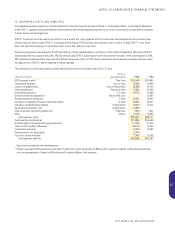

Decommissioning expenses recognized include the following components:

(Thousands of dollars) 2000 1999 1998

Annual decommissioning cost accrual reported as depreciation expense:

Externally funded $51,433 $33,178 $33,178

Internally funded (including interest costs) (16,111) 1,595 1,477

Interest cost on externally funded decommissioning obligation 5,151 4,191 6,960

Earnings from external trust funds (5,151) (4,191) (6,960)

Net decommissioning accruals recorded $35,322 $34,773 $34,655

Decommissioning and interest accruals are included with the accumulated provision for depreciation on the balance sheet. Interest costs and trust earnings

associated with externally funded obligations are reported in other income and deductions on the income statement.