Vonage 2011 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2011 Vonage annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

|

|

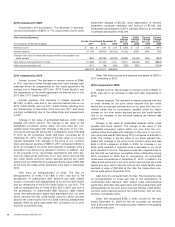

Trends in Our Industry and Key Operating Data A num-

ber of trends in our industry have a significant effect on our

results of operations and are important to an understanding of

our financial statements.

Competitive landscape. We face intense competition from

traditional telephone companies, wireless companies, cable

companies, and alternative voice communication providers. Most

traditional wireline and wireless telephone service providers and

cable companies are substantially larger and better capitalized

than we are and have the advantage of a large existing customer

base. In addition, because our competitors provide other serv-

ices, they often choose to offer VoIP services or other voice serv-

ices as part of a bundle that includes other products, such as

video, high speed Internet access, and wireless telephone serv-

ice, which we do not offer. Further, as wireless providers offer

more minutes at lower prices, better coverage, and companion

landline alternative services, their services have become more

attractive to households as a replacement for wireline service.

We also compete against alternative voice communication pro-

viders, such as magicJack, Skype, and Google Voice. Some of

these service providers have chosen to sacrifice telephony rev-

enue in order to gain market share and have offered their serv-

ices at low prices or for free. As we continue to introduce

applications that integrate different forms of voice and messaging

services over multiple devices, we are facing competition from

emerging competitors focused on similar integration, as well as

from alternative voice communication providers. In addition, our

competitors have partnered and may in the future partner with

other competitors to offer products and services, leveraging their

collective competitive positions. We also are subject to the risk of

future disruptive technologies. In connection with our increasing

emphasis on the international long distance market, we face

competition from low-cost international calling cards and VoIP

providers in addition to traditional telephone companies, cable

companies, and wireless companies.

Broadband adoption. The number of United States house-

holds with broadband Internet access has grown significantly. On

March 16, 2010, the Federal Communications Commission

(“FCC”) released its National Broadband Plan, which seeks,

through supporting broadband deployment and programs, to

encourage broadband adoption for the approximately 100 million

United States residents who do not have broadband at home.

We expect the trend of greater broadband adoption to continue.

We benefit from this trend because our service requires a broad-

band Internet connection and our potential addressable market

increases as broadband adoption increases.

Regulation. Our business has developed in a relatively lightly

regulated environment. The United States and other countries,

however, are examining how VoIP services should be regulated.

The November 2010 order by the FCC in response to a request

by Kansas and Nebraska that permits states to impose state

universal service fund obligations on VoIP service, discussed in

Note 10 to our financial statements, is an example of efforts by

regulators to determine how VoIP service fits into the tele-

communications regulatory landscape. In addition to regulatory

matters that directly address VoIP, a number of other regulatory

initiatives could impact our business. One such regulatory ini-

tiative is net neutrality. In December 2010, the FCC adopted a

revised set of net neutrality rules for broadband Internet service

providers. These rules make it more difficult for broadband Inter-

net service providers to block or discriminate against Vonage

service. Several broadband Internet service providers have filed

appeals of the FCC’s new rules at the D.C. Circuit Court of

Appeals alleging that the FCC lacks authority to apply its rules to

broadband Internet service providers. In addition, on February 9,

2011, the FCC released a Notice of Proposed Rulemaking on

reforming universal service and the intercarrier compensation

(“ICC”) system that governs payments between tele-

communications carriers primarily for terminating traffic. The

FCC's adoption of an ICC proposal will impact Vonage's costs

for telecommunications services. On October 27, 2011, the FCC

adopted an order reforming universal service and ICC. The FCC

order provides that VoIP originated calls will be subject to inter-

state access charges for long distance calls and reciprocal

compensation for local calls that terminate to the public switched

telephone network (“PSTN”). The termination charges for all traf-

fic, including VoIP originated traffic, will transition over several

years to a bill and keep arrangement (i.e., no termination

charges). We believe that the order would positively impact our

costs over time. See also the discussion under “Regulation” in

Note 10 to our financial statements for a discussion of certain

other regulatory issues that impact us.

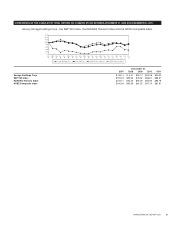

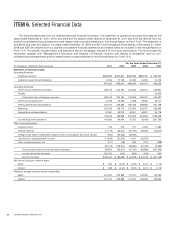

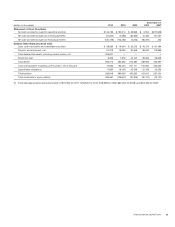

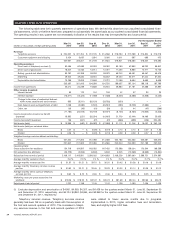

The table below includes key operating data that our management uses to measure the growth and operating performance of our

business:

For the Years Ended December 31,

2011 2010 2009

Gross subscriber line additions 672,274 640,205 748,681

Change in net subscriber lines (29,996) (30,013) (155,458)

Subscriber lines (at period end) 2,374,887 2,404,883 2,434,896

Average monthly customer churn 2.6% 2.4% 3.1%

Average monthly revenue per line $ 30.35 $ 30.48 $ 29.49

Average monthly telephony services revenue per line $ 30.22 $ 30.06 $ 28.68

Average monthly direct cost of telephony services per line $ 8.23 $ 8.40 $ 7.08

Marketing costs per gross subscriber line addition $ 303.84 $ 309.54 $ 304.52

Employees (excluding temporary help) (at period end) 1,008 1,140 1,225

Gross subscriber line additions. Gross subscriber line addi-

tions for a particular period are calculated by taking the net

subscriber line additions during that particular period and add-

ing to that the number of subscriber lines that terminated during

that period. This number does not include subscriber lines both

added and terminated during the period, where termination

occurred within the first 30 days after activation. The number

does include, however, subscriber lines added during the period

that are terminated within 30 days of activation but after the end

of the period.

Net subscriber line additions. Net subscriber line additions

for a particular period reflect the number of subscriber lines at

the end of the period, less the number of subscriber lines at the

beginning of the period.

Subscriber lines. Our subscriber lines include, as of a

particular date, all paid subscriber lines from which a customer

can make an outbound telephone call on that date. Our sub-

scriber lines include fax lines and soft phones but do not include

our virtual phone numbers or toll free numbers, which only allow

inbound telephone calls to customers. Subscriber lines

decreased by 29,996 from 2,404,883 as of December 31, 2010

to 2,374,887 as of December 31, 2011.

VONAGE ANNUAL REPORT 2011 25