Sallie Mae 2007 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2007 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

|

|

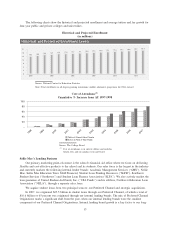

term market penetration. This positions us to control our future volume as well as the costs to originate new

assets. Our internal lending brand loans are our most valuable loans because we do not pay a premium other

than to ED to originate them. The adverse impact of the CCRAA on FFELP loan profitability has further

increased the importance of our internal lending brands as a vehicle for achieving appropriate risk-adjusted

returns.

Preferred Channel Originations growth has been fueled by new business from schools leaving the FDLP

or other FFELP lending relationships, same school sales growth, and growth in the for-profit sector. Since

1999, we have partnered with over 300 schools that have chosen to return to the FFELP from the FDLP. Our

FFELP loan originations at these schools totaled over $2.4 billion in 2007. In addition to working with new

schools, we have also forged broader relationships with many of our existing school clients. Our FFELP and

private originations at for-profit schools have grown faster than at not-for-profit schools due to enrollment

trends as well as our increased market share of lending to these institutions. We expect that in 2008 and in

subsequent years this trend will be reversed. Many of our for-profit school customers have programs for which

we offer non-traditional loans. As we cut back on Private Education Loan programs to this non-traditional

segment of our customer base, we expect to lose FFELP loan volume originated through these schools as well.

Similarly, as we reduce premiums for lender partner and school-as-lender purchases, we expect to lose FFELP

volume. Accordingly, we expect volume in both FFELP loan and Private Education Loan originations to

decline in 2008 relative to 2007.

Consolidation Loans

Between 2003 and 2006, we experienced a surge in consolidation activity as a result of aggressive

marketing and historically low interest rates. This growth has contributed to the changing composition of our

student loan portfolio. FFELP Consolidation Loans earn a lower yield than FFELP Stafford Loans due

primarily to the Consolidation Loan Rebate Fee. The Consolidation Loan margin was 75 basis points lower

than a FFELP Stafford loan in repayment as a result of this fee. This negative impact is somewhat mitigated

by the longer average life of FFELP Consolidation Loans. FFELP Consolidation Loans now represent

67 percent of both our on-balance sheet federally guaranteed student loan portfolio and Managed federally

guaranteed portfolio, respectively.

We expect the percentage of our portfolio consisting of Consolidation Loans will decline steadily over

time. The CCRAA dramatically reduced the margin on new FFELP Consolidation Loans and, as a result these

loans are only marginally profitable for high balance loans and are not profitable for lower loan balances.

Legislation passed in 2006 provided for all FFELP loans to bear a fixed rate to the borrower, thereby

eliminating the potential for the borrower to lock in a more beneficial interest rate on post-July 1, 2006 loans

in a low interest rate environment. This had a significant adverse impact on the Consolidation Loan industry

that developed as a result of the low interest rate environment that existed between 2000 and 2004.

Accordingly, we are no longer buying Wholesale Consolidation Loans or actively marketing Consolidation

Loans to our customer base. Finally, under the HEA, borrowers with loan balances exceeding $30,000 can

extend their repayment term without consolidating their loans. As a result of all of these factors, we believe

that FFELP loans will have a much lower propensity to consolidate in the future. We intend to accommodate

those borrowers who have high loan balances and who wish to consolidate their loans. We will also direct

borrowers wishing to extend their loan’s term to the FFELP extended repayment product, which we believe

will be an attractive alternative to a Consolidation Loan for borrowers seeking a lower monthly payment.

GradPLUS

The Deficit Reduction Act of 2005 expanded the existing Federal PLUS loan program to include graduate

and professional students (“GradPLUS Loans”). Previously, PLUS loans were restricted to parents of

dependent, undergraduate students.

GradPLUS Loans generally have a lower rate of interest than our Private Education Loans and they allow

graduate and professional students to borrow up to the full cost of their education (tuition, room and board),

14