Public Storage 1996 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 1996 Public Storage annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

P

UBLIC

S

TORAGE

, I

NC

. 1996 A

NNUAL

R

EPORT

15

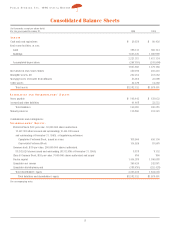

Real estate facilities

Real estate facilities are recorded at cost. Depreciation is computed using the straight-line method over the estimated useful lives of the buildings

and improvements, which are generally between 5 and 25 years.

Allowance for possible losses

The Company has no allowance for possible losses relating to any of its real estate investments, long-lived assets and mortgage notes receivable.

The need for such an allowance is evaluated by management by means of periodic reviews of its investment portfolio.

Intangible assets

Intangible assets consist of property management contracts ($165,000,000) and the cost over the fair value of net tangible and identifiable intan-

gible assets ($67,726,000) acquired in the PSMI Merger. Intangible assets are amortized straight-line over 25 years. At December 31, 1996 and

1995, intangible assets are net of accumulated amortization of $10,473,000 and $1,164,000, respectively. Included in depreciation and amortization

expense is $9,309,000 in 1996 and $1,164,000 in 1995 (for the period from November 16, 1995 through December 31, 1995) related to the

amortization of intangible assets.

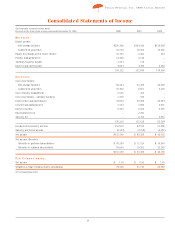

Revenue and expense recognition

Property rents are recognized as earned. Equity in earnings of real estate entities are recognized based on the Company’s ownership interest in the

earnings of each of the unconsolidated real estate entities. Leasing commissions relating to the business park operations are expensed as incurred.

Environmental costs

The Company’s policy is to accrue environmental assessments and/or remediation costs when it is probable that such efforts will be required and

the related costs can be reasonably estimated. The majority of the Company’s real estate facilities were acquired prior to the time that it was

customary to conduct environmental assessments. During 1995, the Company and the Consolidated Partnerships conducted independent environ-

mental investigations of their real estate facilities. As a result of these investigations, the Company recorded an amount which, in management’s

best estimate and based upon independent analysis, was sufficient to satisfy anticipated costs of known remediation requirements. At December 31,

1995, the Company accrued $2,741,000 for estimated environmental remediation costs. Similar to the Company, real estate entities in which the

Company accounts for using the equity method recorded environmental accruals at the end of 1995. The Company’s pro rata share, based on its own-

ership interest, totaled $510,000 and is included in “Equity in earnings of real estate entities” in 1995. Although there can be no assurance, the

Company is not aware of any environmental contamination of any of its facilities which individually or in the aggregate would be material to the

Company’s overall business, financial condition, or results of operations.

Net income per common share

Net income per common share is computed using the weighted average common shares outstanding (adjusted for stock options). The inclusion of

the Class B Common Stock in the determination of earnings per common share has been determined to be anti-dilutive – after giving effect to the

pro forma additional income required to satisfy certain contingencies (Note 11) required for the Class B common stock to convert into common stock –

and, accordingly, the conversion of the Class B common stock into common stock has not been assumed.

The Company’s preferred stocks (Note 11) were determined not to be common stock equivalents. In computing earnings per common share, pre-

ferred stock dividends totaling $68,599,000, $31,124,000 and $16,846,000 for the years ended December 31, 1996, 1995 and 1994, respectively,

reduced income available to common stockholders.

Fully diluted earnings per common share are not presented, as the assumed conversion of the Company’s convertible preferred stock (Note 11)

would be anti-dilutive.

Stock-based compensation

In October 1995, the FASB issued SFAS No. 123 “Accounting for Stock-Based Compensation” (“Statement 123”) which provides companies an alter-

native to accounting for stock-based compensation as prescribed under APB Opinion No. 25 (APB 25). Statement 123 encourages, but does not

require companies to recognize expense for stock-based awards based on their fair value at date of grant. Statement 123 allows companies to con-

tinue to follow existing accounting rules (intrinsic value method under APB 25) provided that pro-forma disclosures are made of what net income

and earnings per share would have been had the new fair value method been used. The Company has elected to adopt the disclosure requirements

of Statement 123 but will continue to account for stock-based compensation under APB 25. Statement 123’s disclosure requirements are applicable

to stock-based awards granted in fiscal years beginning after December 15, 1994.