Mercury Insurance 2015 Annual Report Download - page 3

Download and view the complete annual report

Please find page 3 of the 2015 Mercury Insurance annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

|

|

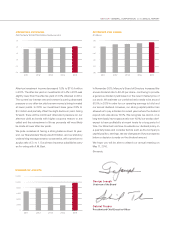

Our 2014 operating results and ratios were distorted by an

unexpected $27.6 million fine imposed by the California Insurance

Commissioner. Accordingly, all Companywide and California

Personal Auto comparisons to 2014 are exclusive of the fine.

During 2015, the insurance industry experienced an increase in both

the frequency and severity of auto claims. Mercury was not immune

from this trend as our loss costs also increased. Although we took

and are continuing to take action to offset increases in loss costs,

our operating results nevertheless fell short of expectations in 2015.

Our 2015 operating earnings were $2.34 per share compared

to $2.78 per share in 2014, a 15.8% decline. The deterioration

in operating earnings was primarily due to an increase in the

combined ratio from 97.8% in 2014 to 99.2% in 2015. Although

our California Private Passenger Automobile combined ratio did

not change as compared to 2014, our Commercial Automobile,

California Homeowners and Private Passenger Automobile results

outside of California deteriorated and offset our consistent California

Private Passenger Automobile results. In addition, $13 million of

adverse reserve development and $19 million of Catastrophe

losses also negatively impacted our 2015 operating results.

Despite the increase in frequency and severity, our California Private

Passenger Automobile combined ratio was 97.0% in both 2015

and 2014. Higher average premiums from rate increases taken

in the latter part of 2014 and in 2015 offset the year over year

increase in frequency and severity. However, we still fell short of

our 95% combined ratio target. To achieve our targeted profitability

levels and to keep up with loss trends, a 5% rate increase was

implemented in March 2016 for Mercury Insurance Company

and a 6.9% rate increase is pending approval from the California

Department of Insurance for California Automobile Insurance

Company. Mercury Insurance Company represents about half of

our Companywide premiums written and California Automobile

Insurance Company represents about 15% of our Companywide

premiums written.

We’ve made significant progress over the past few years in our

operations outside of California as we’ve driven down our accident

year Private Passenger Automobile combined ratio every year since

2009 to a low of 100% in 2014. However, in 2015 we took a step

backward. Our results outside of California were disappointing

as we posted an accident year Private Passenger Automobile

combined ratio of 108% in 2015. The deterioration in the combined

ratio outside of California was primarily driven by our two largest

states, Florida and Texas. In Florida and Texas, we posted calendar

year Private Passenger Automobile combined ratios of 102.7%

and 113.8%, respectively, in 2015 compared to 96.6% and 96.1%,

respectively, in 2014. We experienced significant growth in many

states in 2015 and that growth came at a price. New business

sales increased 14.3% in Florida and 46.1% in Texas and premiums

written grew 15% and 29.5%, respectively. The increase in loss

costs trends coupled with our new business growth penalty were

the main reasons for our poor results outside of California. To

address our profitability we are increasing rates in many states

and are tightening our underwriting.

Part of our long-term strategy is to continue to grow our

Homeowners and Commercial lines of business. In August 2014,

we launched a new Homeowners product in California with

refined pricing and new technology. The new product was very

well received as new business applications increased over 17.5%

in 2015. Companywide, our Homeowners line grew 7% in 2015

to $395 million in premiums written.

MERCURY GENERAL CORPORATION 2015 ANNUAL REPORT

LETTER TO SHAREHOLDERS

COMBINED RATIO VS. INDUSTRY

(In percent)

105

103

97

95

93

99

101

20152011 2012 2013 2014

Mercury General

U.S. Industry

Source for Industry Data: A.M. Best Company